Capital budgeting is a fundamental area within financial management. It is also referred to by several other terms, including capital expenditure decision, capital expenditure management, long-term investment decision, and management of fixed assets. At its core, capital budgeting is the process of making investment decisions in capital expenditure. It involves the planning and control of capital expenditure. Essentially, it is the process of deciding whether or not to commit resources to particular long-term projects whose benefits are to be realized over a period of time. Long-term investment decisions are popularly known as capital budgeting decisions.

Definition and Nature

Various definitions highlight the key aspects of capital budgeting:

- Charles T. Horngren defined capital budgeting as ‘long-term planning for making and financing proposed capital outlay’.

- According to Keller and Ferrara, ‘capital Budgeting represents the plans for the appropriation and expenditure for fixed asset during the budget period’.

- Robert N. Anthony defined it as ‘capital budget is essentially a list of what management believes to be worthwhile projects for the acquisition of new capital assets together with the estimated cost of each product’.

- It can also be defined as the firm’s decision to invest its current funds most efficiently in long-term activities in anticipation of an expected flow of future benefits over a series of years.

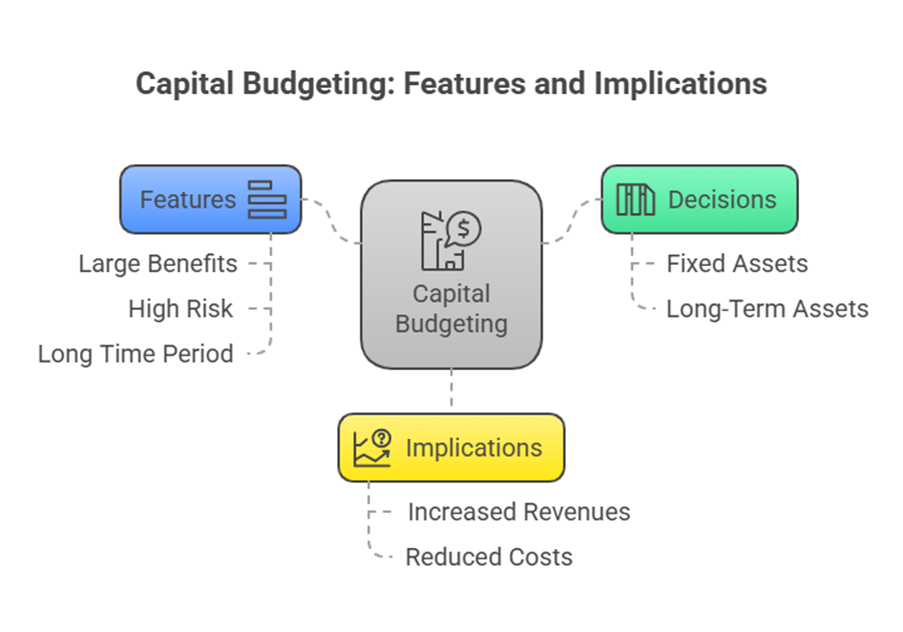

The decisions taken in capital budgeting affect the operations of the firm for many years. They are related to fixed assets or long-term assets that are in operation and yield a return over a period of time, usually exceeding one year. These decisions involve a current outlay or a series of outlays of cash resources in return for an anticipated flow of future benefits. These benefits may be either in the form of increased revenues or reduced costs. Capital expenditure management includes the addition, disposition, modification, and replacement of fixed assets. While the investment proposal is common for both fixed and current assets, capital budgeting decisions primarily involve fixed assets.

Based on these descriptions, the basic features of capital budgeting can be deduced:

- Potentially large anticipated benefits: The expected returns from these long-term investments can be significant.

- A relatively high degree of risk: Long-term projects inherently carry more uncertainty and risk.

- A relatively long time period: There is a significant time lag between the initial investment outlay and the realization of anticipated returns.

Importance and Purpose

Capital budgeting decisions are considered important, crucial, and critical business decisions for several reasons:

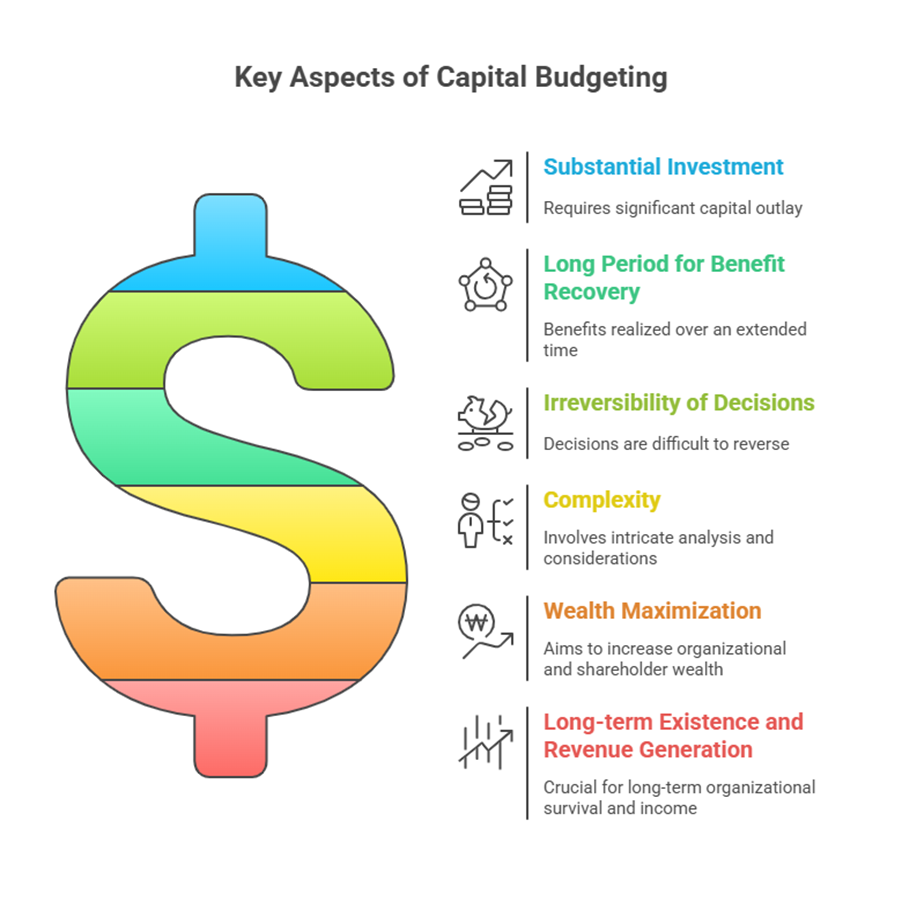

- Substantial Investment: Investment decisions often require substantial capital investment.

- Long Period for Benefit Recovery: Benefits from capital projects are realized over a prolonged period.

- Irreversibility of Decisions: Capital investment decisions are often irreversible or can only be reversed at a heavy loss.

- Complexity: Capital investment decisions involve complex analysis and considerations.

- Wealth Maximization: Capital budgeting is central to maximizing the wealth of the organization and its shareholders by ensuring the optimum utilization of funds.

- Long-term Existence and Revenue Generation: These decisions are crucial for an organization’s long-term existence and its ability to generate revenue. Even non-profit entities need to make investment decisions to fulfill their mission.

The need for capital budgeting decisions generally arises for selecting the most profitable project of capital investment.

Scope and Types of Capital Investment Decisions

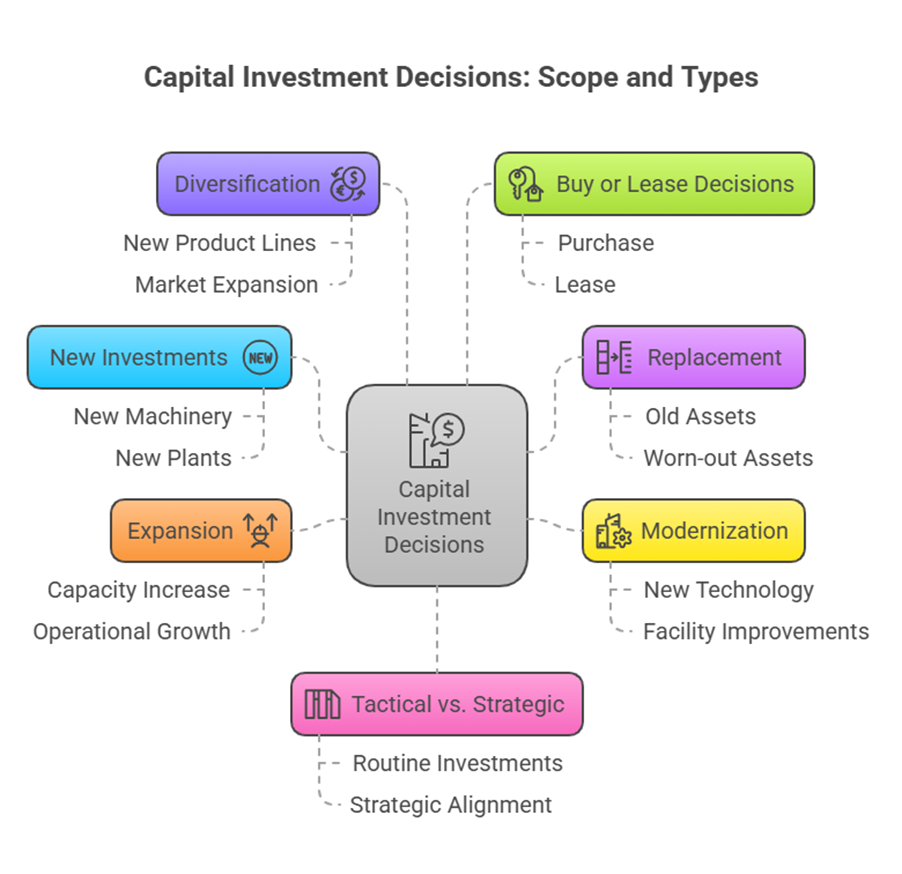

The scope of capital budgeting is broad and encompasses various types of long-term investment decisions:

- New Investments: Decisions related to purchasing new machinery, setting up new plants, or undertaking new projects.

- Replacement: Deciding whether to replace old, worn-out assets.

- Modernization: Investing in new technology to improve existing facilities.

- Expansion: Increasing the capacity of existing operations.

- Diversification: Investing in new product lines or markets, which typically requires large long-term funds.

- Buy or Lease Decisions: Determining whether to purchase an asset or acquire it through a lease arrangement, comparing the costs and benefits of a large initial outlay versus a series of rental payments.

- Tactical vs. Strategic: Decisions can range from routine tactical investments to strategic ones aligned with overall business objectives.

Types of capital investment decisions can also be classified based on the firm’s existence and the situations they address.

The Capital Budgeting Process

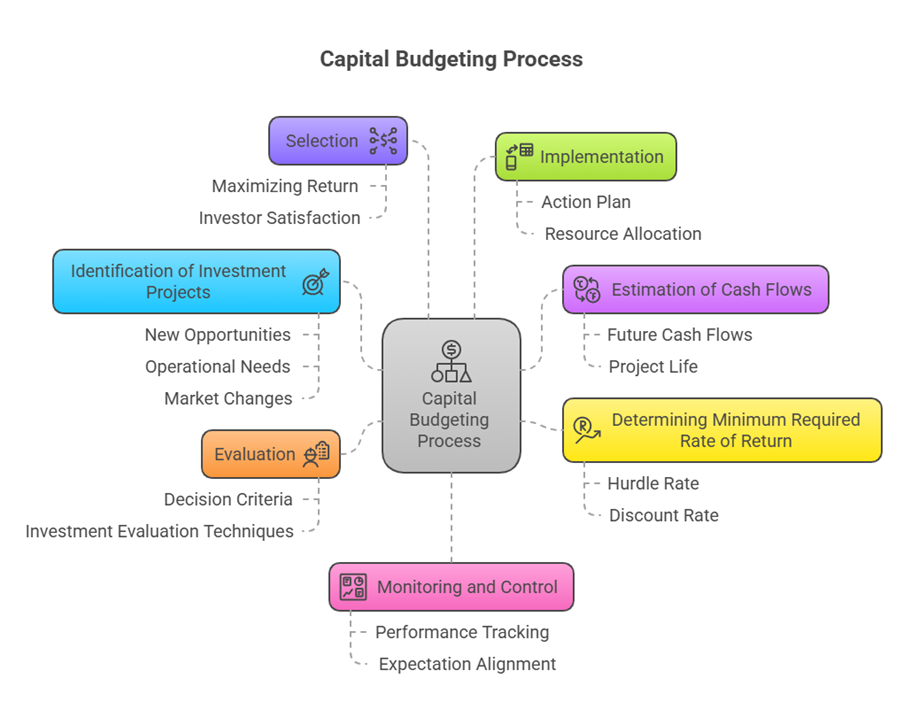

The process of capital budgeting involves several steps:

- Identification of investment projects: Identifying projects that are strategic to the business’ overall objectives. This could involve exploring new opportunities, addressing operational needs, or responding to market changes.

- Estimation of Cash flows: Estimating future cash flows over the entire life for each project under consideration. This is one of the most important tasks.

- Determining the minimum required rate of return (i.e., WACC): Establishing the hurdle rate or discount rate to be used in the evaluation. The cost of capital is the minimum required rate of return.

- Evaluation: Evaluating each alternative project using different decision criteria or investment evaluation techniques.

- Selection: Selecting the investment proposal that maximizes the return to the investors.

- Implementation: Putting the selected project into action.

- Monitoring and Control: Tracking the project’s performance against expectations.

Key Concepts in Capital Budgeting

Several key concepts underpin the capital budgeting process:

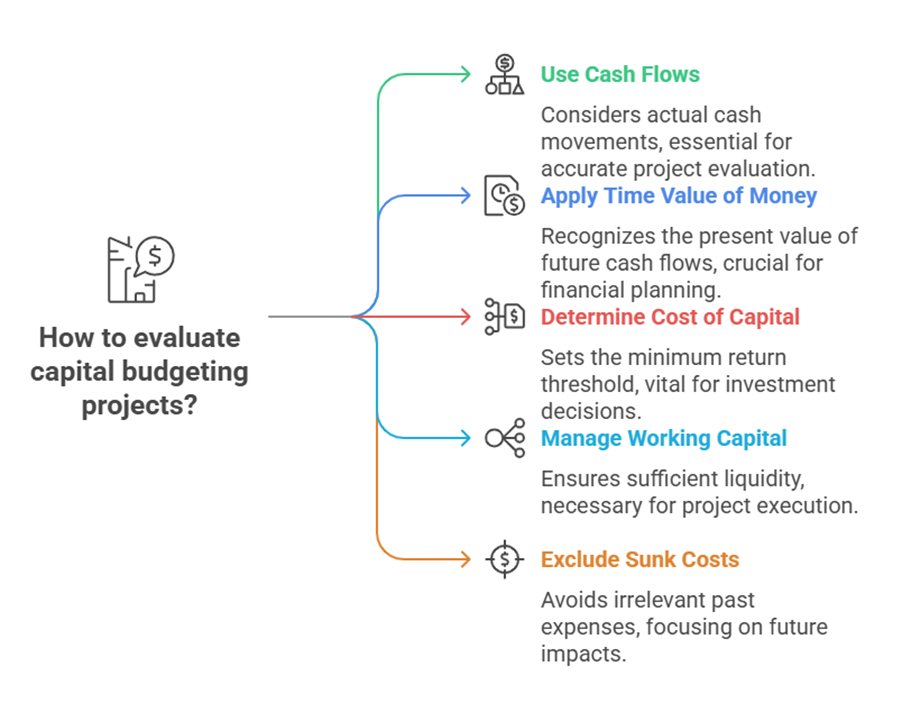

- Cash Flows vs. Accounting Profit: Capital budgeting analysis considers only incremental cash flows from an investment likely to result from accepting a project. Estimating these future cash flows is critical. A key principle is the use of post-tax incremental cash flows. Accounting profit is generally not used because it has limitations; for example, the timing of cash flow may not match the period of profit, and non-cash items like depreciation do not have immediate cash outflow. Accounting data is generally avoided in favor of cash flows for project evaluation. Savings in respect of a cost are treated as an inflow in capital budgeting.

- Time Value of Money: This is a fundamental concept in financial management, relevant to capital budgeting decisions. It recognizes that a rupee received today is worth more than a rupee received in the future. Modern capital budgeting techniques explicitly incorporate this concept.

- Cost of Capital: Each rupee of capital raised by an entity bears some cost, commonly known as the cost of capital. The cost of capital is also called the cut-off rate, target rate, hurdle rate, and required rate of return. It is closely associated with the value and earning capacity of the firm. The finance manager must carefully decide on the cost of capital, especially when using different sources of finance. The cost of capital is used as a decision criterion to evaluate capital budgeting decisions – whether to accept or reject a project. It is the minimum required rate of return. Calculating the cost of various sources of finance is necessary for selecting a capital structure where the expectation of investors is minimum, maximizing shareholders’ wealth. The weighted average cost of capital (WACC) is the combined or weighted average cost of various sources of capital. The marginal cost refers to the average cost of new or additional funds, and it is the marginal cost that should be considered in investment decisions.

- Working Capital: Working capital requirements are estimated by forecasting the amount needed for each item of current assets and current liabilities. Working capital is the difference between current assets and current liabilities. Adequate working capital is important. In an NPV analysis for capital budgeting, adjustments for working capital are made. Net increase in working capital is considered in the cash flows for the project. Working capital management is also a distinct area of financial management.

- Sunk Costs: In capital budgeting, sunk costs are excluded from the analysis because they are not incremental to the decision being made.

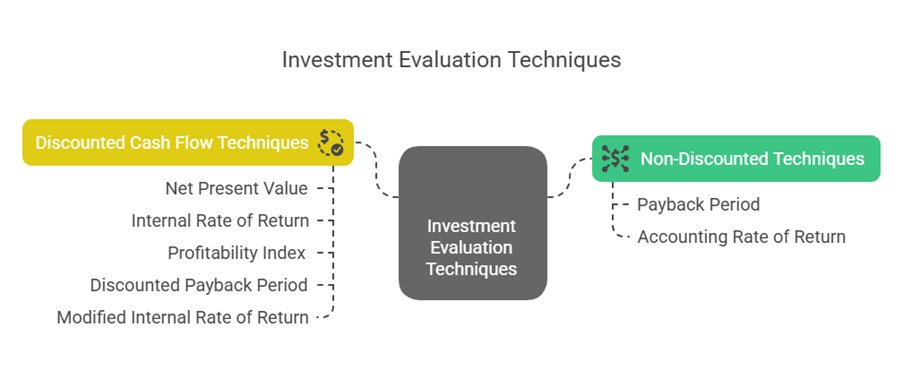

Investment Evaluation Techniques

Various techniques are used to evaluate investment proposals:

Non-Discounted (Traditional) Techniques: These methods rely on accounting information and determine desirability based on useful life and expected returns. A major limitation is that they do not account for the time value of money.

- Payback Period: This technique calculates the time required to recover the initial investment from the project’s cash inflows. It ignores the time value of money.

- Accounting Rate of Return (ARR): This method evaluates profitability based on accounting profit. As mentioned, accounting profit has limitations for capital budgeting.

Discounted Cash Flow (Modern) Techniques: These methods incorporate the time value of money by discounting future cash flows to their present value.

- Net Present Value (NPV): This is a widely used technique. It calculates the present value of all expected future cash flows (inflows minus outflows), discounted at the required rate of return (cost of capital), and subtracts the initial investment. The acceptance rule for independent projects is to accept projects with a positive NPV.

- Internal Rate of Return (IRR): This is the discount rate that makes the Net Present Value (NPV) of all cash flows from a project equal to zero. It is the discount rate that equates the present value of cash inflows to the initial investment. While it offers benefits, the IRR method has limitations, including the possibility of multiple IRRs and potential conflicts with NPV when ranking mutually exclusive projects or projects of different scales.

- Profitability Index (PI) or Benefit-Cost (B/C) Ratio: This is the ratio of the present value of cash inflows to the initial cash outflow, discounted at the required rate of return. Advantages and disadvantages exist for this technique.

- Discounted Payback Period: Similar to the payback period, but uses discounted cash flows to calculate the time required to recover the initial investment.

- Modified Internal Rate of Return (MIRR): A variation of IRR designed to overcome some of its limitations. It has its own definition, calculation process, and strengths.

For independent projects, the decision criteria for these techniques (accept/reject rules) are summarized in the sources. For mutually exclusive projects, there can be conflicts in ranking between methods like NPV and IRR.

Special Cases and Advanced Topics

Capital budgeting also involves addressing special situations and more advanced concepts:

- Capital Rationing: This occurs when a firm has profitable investment proposals but faces financial constraints limiting the total amount of capital expenditure. The objective is to select the combination of projects that maximizes the total NPV within the budget constraint. This may involve ranking projects. Capital rationing can be soft (internal budget ceiling) or hard (inability to obtain external funds). It can apply to divisible or non-divisible projects.

- Dealing with Risk and Uncertainty: While initial capital budgeting discussions might assume known cash flows with certainty, in practice, investment projects are exposed to various risks and factors. Analyzing risk and uncertainty is an important element of capital budgeting decisions. Advanced capital budgeting specifically covers dealing with risk in investment decisions. Methods for incorporating risk include the Certainty Equivalent Approach, Risk Adjusted Discount Rate, Expected NPV and Standard Deviation, Decision Tree Analysis, and Real Options. Sensitivity analysis and Scenario analysis are also techniques to deal with uncertainty. The Capital Asset Pricing Model (CAPM) provides a conceptual framework for evaluating investment decisions by comparing risk and return to securities.

- Inflation: The impact of inflation on capital budgeting decisions is a relevant consideration. This involves techniques for inflation-adjusted cash flow forecasting.

- Projects with Unequal Lives: Specific techniques exist for comparing projects with different useful lives.

- Abandonment Value: The concept of the value of abandoning a project is also considered.

- International Capital Budgeting: Capital budgeting decisions for projects in foreign countries are addressed within International Financial Management.

In summary, Capital Budgeting is a critical function of financial management focused on evaluating and selecting long-term investments to maximize shareholder wealth. It involves a structured process of identifying projects, estimating future cash flows (specifically, post-tax incremental cash flows), determining the appropriate discount rate (cost of capital), evaluating alternatives using various techniques (both traditional and discounted cash flow methods like NPV and IRR), and selecting the most beneficial projects, while also considering factors like capital constraints (capital rationing) and risk. The accuracy of cash flow estimates is paramount for the final decision.