Capital investment decisions, also known as capital budgeting decisions or long-term investment decisions, are a crucial aspect of financial management. These decisions involve the selection of assets in which a firm will invest funds, typically relating to fixed assets or long-term assets expected to yield a return over a period usually exceeding one year. The successful operation of any business depends on investing resources in a way that brings benefits or the best possible returns.

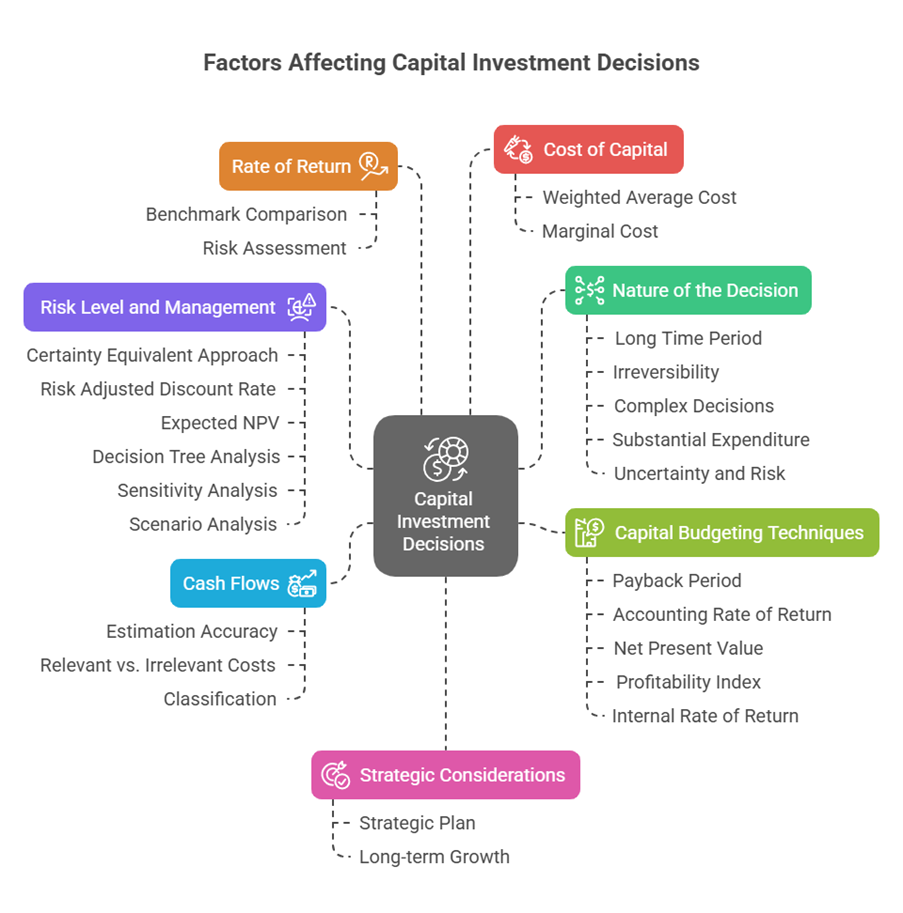

Several factors affect these significant decisions:

- Nature of the Decision: Capital budgeting decisions possess several inherent characteristics that make them complex and impactful.

- Long Time Period / Long-run Effect: The effects of these decisions extend over a considerable period, often several years beyond the current accounting period. They not only influence the firm’s future benefits and costs but also shape its rate and direction of growth. The future growth and profitability of a firm depend on the investment decisions made today. Investing over a long period increases risk.

- Irreversibility: Many investment decisions are irreversible; once implemented, reversing them is very difficult and often not economically feasible without substantial losses. Reasons for this can include upfront payments, contractual obligations, or technological limitations. Once funds are committed to a project, they generally must continue until the end, regardless of loss or profit.

- Complex Decisions: These decisions are complex because they involve assessing future events, which are difficult to predict. Quantifying all benefits and costs related to a particular investment can also be challenging.

- Substantial Expenditure / Large Amount of Funds: Capital investment decisions often require significant financial outlay. Arranging these substantial funds requires determined effort to ensure their timely availability.

- Uncertainty and Risk: Since future benefits are not known with certainty, investment decisions necessarily involve risk. An unwise decision can be disastrous. The uncertainty of the future contributes to the difficulty of taking long-term investment decisions.

- Cash Flows: Cash flows are the most critical factor in a capital investment decision. Investment decisions involve large amounts of cash and are based on the expectation of creating cash flows over time.

- Estimation Accuracy: Estimating future cash flows is a most important task in capital budgeting, and the quality of the final decision depends on the accuracy of these estimates.

- Relevant vs. Irrelevant Costs: Only incremental cash flows (changes in cash flows resulting from the investment) are considered relevant. Sunk costs (already incurred and cannot be reversed) are irrelevant and should be excluded. Opportunity costs (benefits foregone by choosing an alternative) and imputed, out-of-pocket, avoidable, and differential costs are considered relevant.

- Classification: Cash flows are typically classified into initial cash flow (outlay for acquiring the asset, including installation and incidental costs), subsequent cash flows (receipts and payments over the life of the investment), and terminal cash flow (at the end of the project’s life). For example, the release of working capital at the end of a project’s life should be considered a cash inflow. Depreciation, being a non-cash expenditure, is added back when calculating cash flow after tax. Tax shields, such as those from depreciation, are also considered.

- Rate of Return: The rate of return expected from the project is a highly significant standard for appraisal. It needs to be compared against a benchmark, typically the cost of capital. A project with a higher expected rate of return may be selected, assuming similar risk levels.

- Risk Level and Management: Investment projects are exposed to varying degrees of risk. Risk increases when investment is stretched over a long period. Higher risk leads to a higher expected return. Various methods are employed to incorporate risk into capital budgeting decisions, including the Certainty Equivalent Approach, Risk Adjusted Discount Rate, Expected NPV, Standard Deviation of NPV, Decision Tree Analysis, Sensitivity Analysis, and Scenario Analysis.

- Certainty Equivalent Approach: This involves adjusting future cash flows using Certainty Equivalent (CE) factors, which vary inversely with risk (higher risk means lower CE factor). These adjusted cash flows are then discounted at a risk-free rate to find the NPV. CE factors range between 0 and 1.

- Risk Adjusted Discount Rate (RADR): This method adjusts the discount rate based on the project’s risk level. Higher risk projects use a higher discount rate.

- Expected Net Present Value (NPV): In situations with uncertainty, probabilities are assigned to different cash flow outcomes, and the expected NPV is calculated.

- Decision Tree Analysis: This technique breaks down a project into stages, listing possible outcomes, probabilities, and cash flows at each stage. It helps evaluate sequential decisions under uncertainty.

- Sensitivity Analysis: This studies the impact of changes in one variable (like cash inflow, cost of capital, or initial cost) on the project outcome (e.g., NPV or IRR), keeping other variables constant. It helps identify variables that are most critical or sensitive to changes.

- Scenario Analysis: This is a “what-if” analysis calculating the project outcome for several scenarios (e.g., best-case, base case, worst-case).

- Cost of Capital: This is the minimum rate of return a firm must earn on its investments to maintain the market value of its shares. It’s also the opportunity cost of an investment. The decision to invest depends on the firm’s cost of capital or cutoff rate. To maximize wealth, a firm must earn a rate of return higher than its cost of capital. The cost of capital is the weighted average cost of its various sources of finance, such as debt, preference shares, retained earnings, and equity shares. A higher risk involved in the firm leads to a higher cost of capital. The marginal cost of capital (average cost of new funds) should be considered in investment decisions. The cost of capital is used as the discount rate to determine the present value of estimated future cash flows.

- Capital Budgeting Techniques / Investment Criteria: Various techniques are used to appraise investment proposals.

- Common methods include Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), Profitability Index (PI), Internal Rate of Return (IRR), Discounted Payback Period, and Modified Internal Rate of Return (MIRR).

- Decision rules guide acceptance or rejection. For independent projects, accept if NPV is positive, PI is greater than or equal to 1, or IRR is greater than or equal to the cost of capital (K).

- For mutually exclusive projects (where accepting one means rejecting others), select the project with the highest positive NPV. While IRR ranks projects by rate, NPV ranks by wealth creation, and conflicts can arise, often favouring NPV. If NPV is the same, the project with the highest PI might be selected.

- Strategic Considerations: Capital budgeting decisions should align with the business’s overall strategic objectives. A strategic plan identifies future activities, goals, and resource needs over a longer duration (e.g., 3-5 years or more). Long-term investment decisions affect the firm’s future growth and direction.

- Types of Investment Decisions: The specific nature or purpose of the investment also drives the decision. These can include decisions related to new investments, replacement of assets, modernization, expansion, or diversification into new product lines or markets. Deciding whether to buy or lease an asset is another important area of financial management that involves evaluating costs and benefits over time.

- Evaluations Beyond Finance: At the planning stage, a detailed evaluation of aspects beyond financial viability is required.

- Market Analysis: Focuses on demand for proposed products/services and expected market share.

- Technical Analysis: Considers technical feasibility, inputs, and production layout.

- Economic (Social Cost Benefit) Analysis: Focuses on the potential impact of the investment proposal from a societal viewpoint.

- Ecological Analysis (Environmental Analysis): Considers the impact on the environment, including the cost of controlling or restoring damages.

- Internal and External Environmental Factors: Various factors, internal and external to the company, affect capital budgeting decisions.

- External Factors: These include broad economic or policy changes. Examples are inflation, which raises revenues and costs and requires adjustment in appraisal; change in technology, which can affect costs and efficiencies; and change in Government Policies, such as tax rates or fiscal policy, which may require revising estimates of future cash flows. Interest rate risk, influenced by factors like monetary policy and economic growth, is also relevant.

- Internal Factors: These are specific to the company. While the sources list “Internal Factors”, they don’t provide specific examples of what these factors are in the same way they do for external factors.

- Capital Rationing: This refers to a situation where a firm has limited funds available for investment, even if multiple projects have positive NPVs. In this scenario, the firm must select the combination of projects that maximizes the total NPV within the budget constraint. Capital rationing can be ‘soft’ (an internal budget ceiling) or ‘hard’ (inability to obtain funds externally). This constraint significantly impacts which projects are undertaken.

- Organizational Factors: The size of the organization, the number of projects under consideration, the direct financial benefit of individual projects, the existing asset composition, and the timing of expenditures can influence how formalized and systematic the capital budgeting process is. While these factors might not directly determine if a single project is accepted, they shape the framework and procedures used to evaluate all investment proposals.

In summary, capital investment decisions are affected by the inherent nature of these long-term, irreversible, and risky commitments, the accuracy and relevance of estimated cash flows, the project’s expected rate of return relative to the cost of capital, sophisticated risk analysis techniques, the selection criteria used (capital budgeting techniques), alignment with strategic goals, the specific purpose of the investment (e.g., expansion, diversification), broader market and societal impacts (social and environmental), external economic and policy changes, internal company-specific factors, and potential constraints on available capital (capital rationing).