Introduction to Financial Planning and Capital Structure

Financial Management is a managerial activity focused on the planning and controlling of a firm’s financial resources. It involves crucial financial decisions, including investment decisions (Capital Budgeting), financing decisions (Capital Structure), dividend decisions, and working capital management decisions. Financial Planning and Capital Structure are identified as key topics and major areas within the field of financial management. Financial Management is broadly concerned with the managerial decisions that result in the acquisition and financing of short-term and long-term credits for the firm.

Financial Planning

Financial planning serves as the backbone of both business planning and corporate planning. It is described as a systematic approach where a financial planner assists the customer in maximizing their existing financial resources through the use of financial tools to achieve their financial goals. Financial planning plays a major role in financial management.

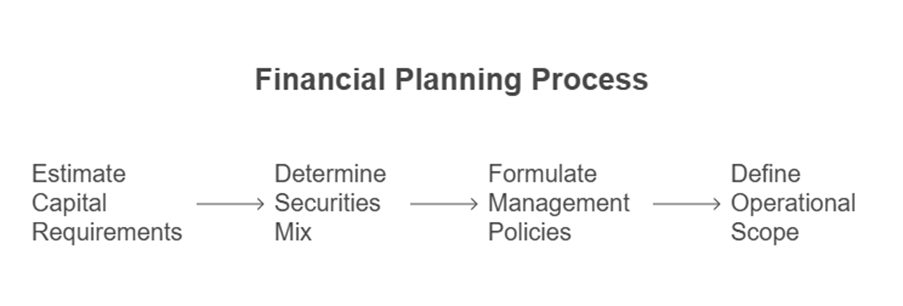

The important parts of financial planning include:

- Estimating the amount of capital to be raised: This involves determining the total financial requirements of the business.

- Determining the form and proportionate amount of securities: This refers to deciding the mix of different types of financing instruments, such as shares and debentures, and their relative proportions. This directly relates to the capital structure decision.

- Formulating policies to manage the financial plan: This involves establishing guidelines and procedures to effectively implement and oversee the financial strategy.

Financial planning helps in defining the feasible area of operation for all types of activities, thereby setting the overall planning framework.

Capital Structure

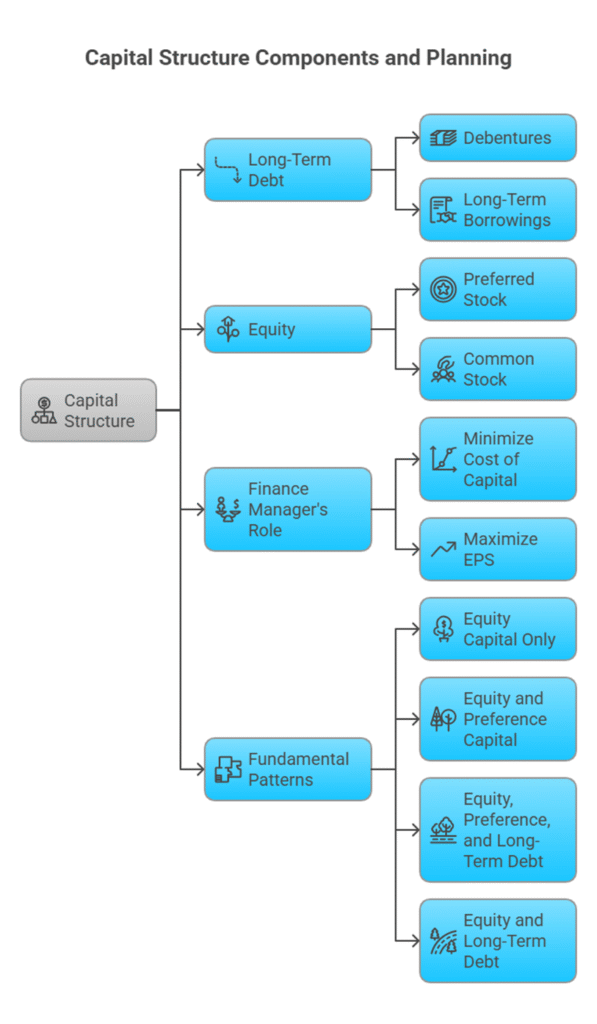

Capital structure is a critical component of financing decisions. It represents the permanent financing of a company. It is primarily composed of long-term debt and equity. More formally, capital structure refers to the composition or makeup of a company’s capitalization, and it includes all long-term capital resources. This mix of a firm’s permanent long-term financing includes debt, preferred stock, and common stock equity.

The capital of a company, as it relates to capital structure, consists of equity shareholders’ funds, preference share capital, and long-term external debts. Long-term sources of finance, which form the capital structure, are required for substantial investments in the business. These long-term needs generally refer to fund requirements for a period exceeding 5-10 years, such as investments in plant, machinery, land, buildings, and funds needed for permanent or hard-core working capital. The primary long-term sources of finance include share capital (both equity and preference) and debt (including debentures, long-term borrowings, or other debt instruments). Owner’s capital or equity capital is considered a source of permanent capital. Debentures are long-term loans raised from the public, typically carrying different rates of interest and issued under terms and conditions listed in a debenture trust deed. Security financing, which involves mobilizing finance through the issue of securities like shares and debentures, plays a major role in deciding the capital structure.

According to Gere Stenberg, the capital structure of a company refers to the composition of its capitalization and includes all long-term capital resources such as loans, bonds, shares, and reserves. Capital structure is thus made up of debt and equity securities and represents the permanent financing of a firm.

The finance manager’s role involves planning the appropriate mix of different securities within the total capitalization. This planning aims to minimize the cost of capital and maximize the earnings per share (EPS) for equity shareholders.

Fundamental patterns of capital structure include:

- Equity capital only (including Reserves and Surplus)

- Equity and preference capital

- Equity, preference, and long-term debt (e.g., debentures, bonds, loans from financial institutions)

- Equity and long-term debt

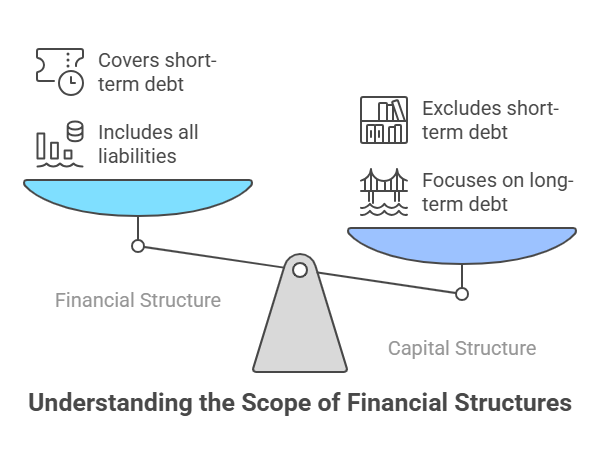

Capital Structure vs. Financial Structure

While some authors use the terms capital structure and financial structure interchangeably, they are distinct concepts. Financial structure illustrates the pattern of total financing. It measures the extent to which total funds are available to finance the total assets of the business. Financial structure encompasses the entire liabilities side of the Balance Sheet.

In contrast, capital structure is that part of the financial structure that represents only long-term sources. It is generally defined to include only long-term debt and total shareholders’ investment, excluding all short-term debt and current liabilities. Therefore, financial structure is a broader concept, and capital structure is just a part of it. The relationship can be expressed as: Financial Structure = Total liabilities OR Financial Structure = Capital Structure + Current liabilities.

Financing Decisions and Their Relation to Capital Structure

Financing decisions are one of the main functions of financial management. These decisions relate to acquiring the optimum finance required to meet financial objectives. A key aspect of financing decisions is ensuring that the company has a sound capital structure. A sound capital structure involves a proper balance between equity capital and debt.

The decision regarding the source and quantum of capital is crucial. Capital structure decisions are concerned with obtaining funds to meet the firm’s long-term investment requirements. The finance manager must decide how much funds to raise, from which sources, and when. This involves deciding the forms of financing (which sources to use), their actual requirements (the amount to be funded), and their relative proportions (the mix) in the total capitalization.

Factors Affecting Capital Structure

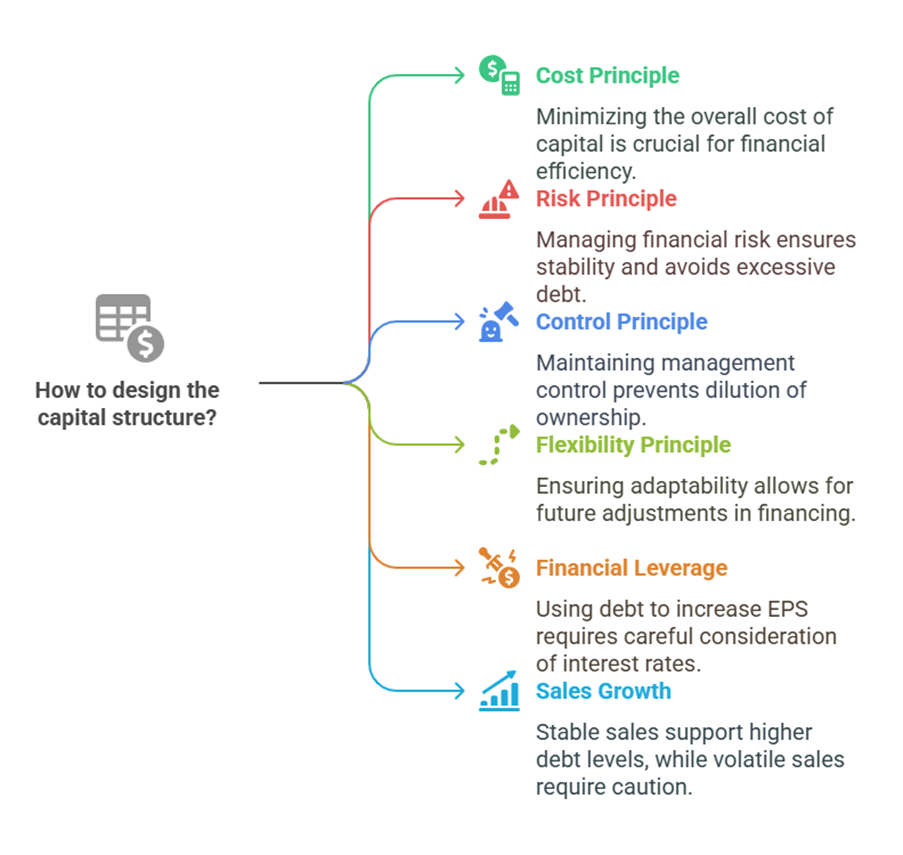

When choosing a suitable financing pattern and designing the capital structure, certain fundamental principles and factors should be considered:

- Cost Principle: A primary goal is to ensure that the overall cost of capital remains minimal. To achieve this, the finance manager needs to calculate the cost of various sources of finance. The Weighted Average Cost of Capital (WACC) is a relevant concept for determining the overall cost. Different capital structures will have different overall costs depending on the proportion and cost of each component (e.g., equity, preference shares, debt).

- Risk Principle: The capital structure should be designed so that the financial risk of a company does not increase beyond a tolerable limit. Excessive debt carries a high risk for an organization. Financial risk can be understood as the variability in earnings or cash flows and market values. Using debt introduces fixed financial charges (interest), which increases the variability of earnings available to shareholders.

- Control Principle: While designing the capital structure, the finance manager may also aim to keep the existing management control and ownership undisturbed. Issuing new equity shares will dilute the existing control pattern and often involves a higher cost. Issuing more debt, on the other hand, does not cause dilution in control but significantly increases the degree of financial risk.

- Flexibility Principle: Flexibility means that the management chooses a combination of financing sources that can be easily adjusted in the future according to changes in the need for funds. For instance, debt might be interchanged (e.g., high-interest debt replaced with lower-interest debt), an option not typically available with equity investment.

- Financial Leverage or Trading on Equity: This principle involves the use of long-term fixed interest bearing debt and preference share capital along with equity share capital. The use of long-term debt can increase earnings per share (EPS) if the firm yields a return higher than the cost of debt. Using preference share capital also increases EPS, but the leverage impact of debt is much greater because interest is tax-deductible. This situation, where return on assets is higher than the cost of financing, leading to increased EPS with the use of fixed-charge financing, is known as favourable financial leverage or Trading on Equity. Conversely, leverage can operate adversely if the interest rate on debt is more than the expected rate of earnings of the firm, potentially reducing EPS. Therefore, caution is needed when planning the capital structure using leverage.

- Growth and Stability of Sales: The nature of the firm’s sales (their growth prospects and stability) can influence the appropriate capital structure. Firms with stable sales may tolerate higher levels of fixed charge financing (debt) compared to firms with volatile sales.

- Other Considerations: These can include the nature of the industry, the level of competition within the industry, and other specific circumstances facing the company.

Balancing these factors can be challenging, as it is practically difficult to achieve all three primary goals (Control, Risk, Cost) simultaneously. A finance manager must find a balance among these objectives.

Optimal Capital Structure

The ultimate objective of financial management, and thus of capital structure decisions, is to maximize wealth. This translates into maximizing the value of the company. An optimal capital structure is one that achieves this wealth maximization. When choosing a capital structure, the aim is to select the one that maximizes the market price per share (MPS).

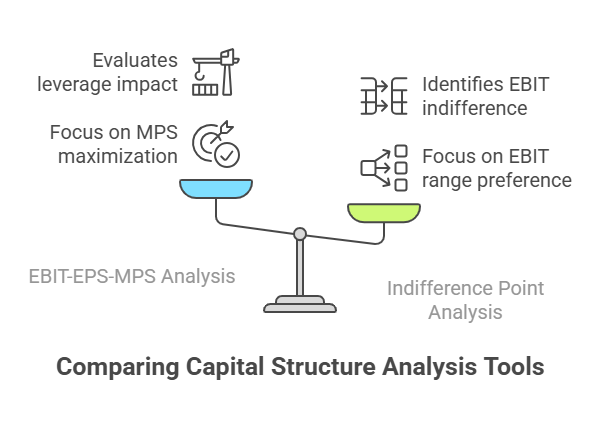

To determine the optimal capital structure, financial managers utilize various analytical tools. Two key tools mentioned are EBIT-EPS-MPS analysis and Indifference Point analysis.

- EBIT-EPS-MPS Analysis: This analysis evaluates how different capital structures impact Earnings Before Interest and Taxes (EBIT), Earnings Per Share (EPS), and subsequently, Market Price per Share (MPS). The goal is to choose a capital structure that maximizes MPS. For a given level of EBIT, different financing mixes (capital structures) will result in different EPS levels, primarily due to the fixed financial charges associated with debt and preference shares. The effect of leverage on EPS arises from the relationship between the rate of return on assets and the cost of fixed-charge financing. If the return on assets is higher than the financing cost, increasing fixed-charge financing increases EPS (favourable leverage). If the return is lower, increasing fixed-charge financing can reduce EPS (unfavourable leverage). This analysis provides useful guidance in selecting a particular level of debt financing and is an effective tool for planning and designing the capital structure.

- Indifference Point Analysis: This analysis, often performed in conjunction with EBIT-EPS analysis, identifies the level of EBIT at which the EPS remains the same for two or more alternative financing plans. It helps in understanding the range of EBIT over which one financing plan might be preferable to another.

While debt financing often appears attractive due to potentially lower explicit costs and the tax deductibility of interest, leading to a lower real cost compared to preference shares, the analysis of different capital structures and their effect on expected EPS provides insight into optimal debt levels.

Capital Structure Theories

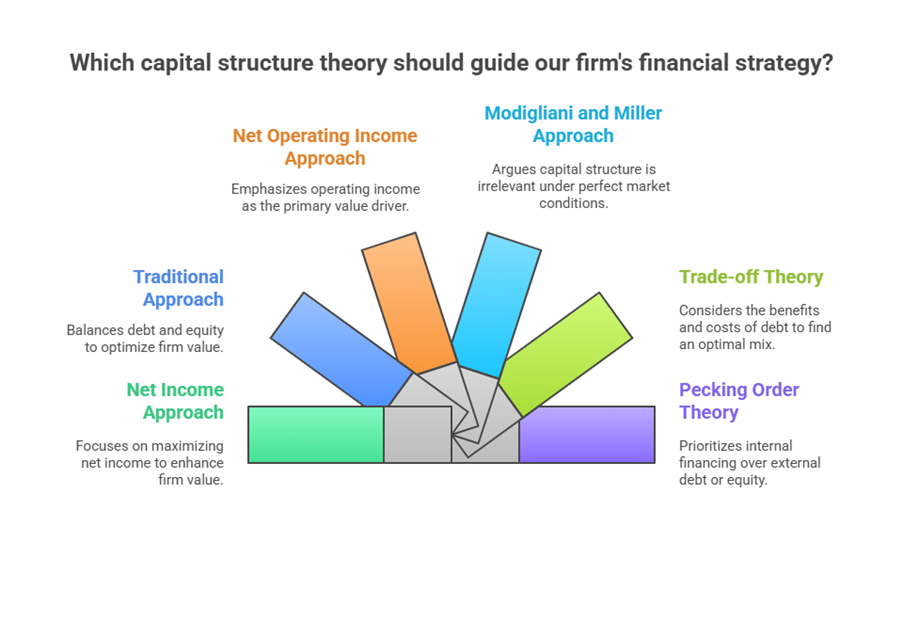

Various theories exist to explain the relationship between the cost of capital, the capital structure, and the value of the firm. These theories attempt to provide a framework for understanding how the debt-equity mix affects firm value and whether an optimal structure exists. Some prominent theories include:

- Net Income (NI) Approach

- Traditional Approach

- Net Operating Income (NOI) Approach

- Modigliani and Miller (MM) Approach

- Trade-off Theory

- Pecking Order Theory

These theories explore the relevancy or irrelevancy of capital structure decisions to the value of the firm.

In summary, Financial Planning provides the framework for estimating capital needs and determining financing sources, while Capital Structure defines the specific mix of long-term debt and equity used to finance the firm’s assets. Financing decisions involve carefully considering factors like cost, risk, control, and flexibility to design a capital structure that minimizes the cost of capital, manages risk, and ultimately maximizes shareholder wealth and firm value, often utilizing tools like EBIT-EPS and indifference point analysis.