Estimating capital requirements is a fundamental part of financial planning for a business. This process involves determining the amount of funds a firm needs to operate its business. Capital refers to the total investment of the company in terms of money and assets, also known as the total wealth of the company. Investing a large amount of finance into the business is referred to as capital.

Financial planning includes several important parts, with estimating the amount of capital to be raised being the first. The objective of financial management includes the procurement of funds. Business enterprises require funds to meet different types of requirements, which can be grouped into three categories: long-term, medium-term, and short-term financial needs.

Types of Financial Needs and Their Estimation

- Long-term financial needs: These requirements are generally for a period exceeding 5-10 years. They involve investments in fixed assets such as plant, machinery, land, and buildings. Funds required to finance the permanent or hard-core working capital should also be procured from long-term sources. Estimating these needs is linked to capital budgeting, which is the process of evaluating and selecting long-term investments that align with the goal of maximizing investor wealth. Capital budgeting involves plans for the appropriation and expenditure for fixed assets during a budget period. Decisions in this area affect the firm’s operations for many years. One of the most important tasks in capital budgeting is estimating future cash flows for a project, as the final decision depends on the accuracy of these estimates. Capital budgeting decisions are crucial due to the substantial expenditure involved, the long period for recovery of benefits, the irreversibility of decisions, and the complexity involved. Long-term financing sources can include equity share capital, preference share capital, debentures, long-term loans from financial institutions, and venture capital financing.

- Medium-term financial needs: These requirements are for a period exceeding one year but not exceeding 5 years. They might be needed for items like stores and spares, critical spares, tools, dies, and moulds. Medium-term sources can include debentures, public deposits, and bank loans/overdrafts.

- Short-term financial needs: These needs arise to finance current assets such as stock, debtors, and cash. Investments in these assets are known as meeting the working capital requirements of the concern. Short-term financial needs are for a short period, typically not exceeding the accounting period of one year.

Capitalization

Capitalization refers to the process of determining the quantum of funds that a firm needs to run its business. It is defined as the sum total of the par value of all shares. Importantly, capitalization only includes the par value of share capital and debenture and does not include reserve and surplus.

Theories of Capitalization relate to arriving at the value at which the company has to be capitalized after estimating financial requirements. The two theories mentioned are the Cost Theory and the Earning Theory.

- Cost Theory: According to this theory, the value of a company is determined by adding up the cost of fixed assets (like plants, machinery, patents) and the capital regularly required for continuous operation (working capital).

- Earning Theory: (Details on the Earning Theory are not provided in the excerpts).

Capitalization can result in different situations: Over Capitalization, Under Capitalization, and Water Capitalization.

- Over Capitalization: This is a situation where a company possesses an excess of capital in relation to its activity level and requirements. It means having more capital than actually required, and the funds are not properly used. In other words, assets are worth less than issued share capital, and earnings are insufficient to pay dividends and interest.

- Under Capitalization: This is the reverse of over-capitalization. It is a state where the actual capitalization is lower than the proper capitalization warranted by its earning capacity.

Understanding capitalization provides a framework for thinking about the total amount of funds considered necessary for the business’s operations.

Estimating Working Capital Requirements

Estimating working capital needs is a significant part of determining the total capital required, especially for meeting short-term financial needs. Working capital is commonly defined in accounting terms as the difference between current assets and current liabilities.

However, other definitions exist, such as “the amount of funds necessary to cover the cost of operating the enterprises” according to Shubin, or “current assets of a company that are changed in the ordinary course of business from one form to another as for e.g. Cash to inventories, inventories to receivables and receivables to cash” according to Gene Stenberg.

Working capital consists of various current assets and current liabilities. To estimate working capital requirements, a finance manager first estimates the required assets and the required Working Capital for a particular period. Sound financial and statistical techniques, supported by judgment, should be used to predict the quantum of working capital required at different times.

Methods for Estimating Working Capital Needs:

Some factors and methods to consider while planning for working capital requirements include:

- Need for Cash: Identifying the necessary cash balance for day-to-day expenses while minimizing cash holding costs.

- Current Assets Holding Period: Estimating working capital needs based on the average holding period of current assets and relating them to costs, often based on the company’s experience in the previous year. This method is essentially based on the Operating Cycle Concept. The operating cycle measures the time it takes for cash invested in inventory to be converted back into cash through sales and collections from debtors.

- Ratio of Sales: Estimating working capital needs as a ratio of sales, assuming that current assets change with changes in sales.

- Ratio of Fixed Investments: Estimating working capital requirements as a percentage of fixed investments.

- Estimation of Components Method: This is a common practical approach involving forecasting the amount required for each item of current assets and current liabilities.

Components to Estimate:

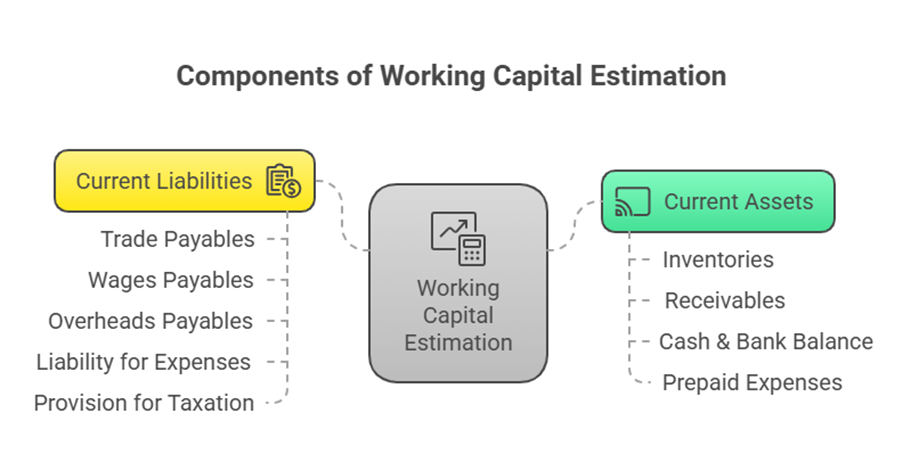

The estimation of working capital typically involves forecasting the levels of the following current assets and current liabilities:

- Current Assets:

- Inventories: This includes raw materials, work-in-process, and finished goods. Estimation involves considering average consumption, production time, and holding periods (e.g., in months or days). Stock of materials might be estimated based on months of average consumption. Finished goods stock might be based on months of average sales or requirements. Work-in-process estimation might involve considering raw material, labour, and overhead costs applied to incomplete units based on production time.

- Receivables (Debtors & Bills Receivable): These arise from credit sales. Estimation is based on average sales and the credit period allowed to customers (e.g., in months or days). Debtors are sometimes taken at cost. Opportunity cost of investment in receivables can also be considered.

- Cash & Bank Balance: Maintaining a minimum cash balance is necessary for day-to-day expenses and unexpected needs. Cash budgets are significant devices for planning and controlling cash receipts and payments. Capital budgets are also considered in cash flow budget preparation, as new capital investments and their associated costs/revenues need to be incorporated.

- Prepaid Expenses: Expenses paid in advance. Estimation is based on the time lag in payment. Sales promotion expenses are sometimes mentioned as payable quarterly in advance.

- Current Liabilities:

- Trade Payables (Creditors & Bills Payables): Amounts owed to suppliers for raw materials or goods. Estimation is based on purchases (specifically raw material purchases) and the credit period extended by suppliers (e.g., in months or days).

- Wages Payables: Wages due to employees. Estimation is based on total wages and the time lag in payment (e.g., half a month or one and a half weeks).

- Overheads Payables: Manufacturing, administrative, or other expenses that are due but not yet paid. Estimation is based on the respective expenses and the time lag in payment (e.g., one month).

- Liability for Expenses: A general category for accrued expenses.

- Provision for Taxation: Amounts set aside for future tax payments. Estimation might consider advance tax payments.

Calculating Net Working Capital:

Once the total current assets and total current liabilities are estimated, the net working capital is typically calculated as Total Current Assets (A) – Total Current Liabilities (B).

Often, a safety margin is added to the estimated net working capital to account for unforeseen contingencies. This margin is usually calculated as a percentage of the net working capital. The total working capital requirement would then be the estimated net working capital plus the safety margin.

Examples provided in the sources illustrate this process by detailing the calculation of each current asset and current liability component based on given data like production units, costs per unit, time lags in stock holding, credit periods, and minimum cash balances. These calculations often involve translating time periods (months, weeks, days) into fractions of a year or relevant period to determine the proportion of annual costs/sales tied up in each component.

Factors Affecting Working Capital Requirements:

Besides the specific component estimations, other factors influence working capital needs, such as:

- Earning Capacity: A business concern with a high earning capacity can generate more Working Capital through cash from operations. This is considered a factor determining working capital requirements.

- Scale of Operations: Production levels, such as single vs. double shift working, can significantly affect the quantities of raw materials, finished goods, and debtors, thus impacting working capital requirements.

The Reserve Bank of India previously prescribed methods for assessing working capital needs, such as the Maximum Permissible Bank Finance (MPBF) concept, but this was withdrawn in 1997, allowing banks to evolve their own assessment methods within prudential guidelines. However, concepts like inventory and receivable norms, suggesting reasonable levels of current assets should be financed, were part of recommendations like those from the Tandon Committee.

In summary, estimating capital requirements involves understanding the overall financial needs of the business, broken down into long-term (fixed assets and permanent working capital) and short-term (variable working capital) components. While capitalization theories relate to determining the aggregate value, practical estimation focuses on forecasting the specific investments needed for both fixed assets (through capital budgeting) and the day-to-day operations (through detailed working capital component estimation). Working capital estimation, in particular, relies on forecasting current assets and liabilities based on expected activity levels, holding periods, and payment lags, often incorporating a safety margin.