The term capital broadly refers to the total investment of the company in terms of money and assets. It is also called the total wealth of the company. When a company invests a large amount of finance into the business, it is called capital.

Capitalization is a more specific concept. It refers to the process of determining the quantum of funds that a firm needs to run its business. It can also be defined as the sum total of the par value of all shares. One source notes that capitalization does not include reserve and surplus, while another defines capital structure (closely related) as including all long-term capital resources, viz, loans, bonds, shares and reserves. Financial planning includes the important parts of estimating the amount of capital to be raised and determining the form and proportionate amount of securities.

Theories of Capitalisation

After estimating the financial requirements of a firm, management must decide on the value at which the company should be capitalized. The sources mention two theories of Capitalisation:

- Cost Theory: According to this theory, the value of a company is arrived at by adding up the cost of fixed assets like plants, machinery, and patents, plus the capital that is regularly required for the continuous operation of the company (working capital). Working capital is considered a major part of the company’s total capitalization.

- Earning Theory: This theory is mentioned as one of the two theories of capitalization, but the sources provided do not detail how value is arrived at under this theory.

Types of Capitalisation

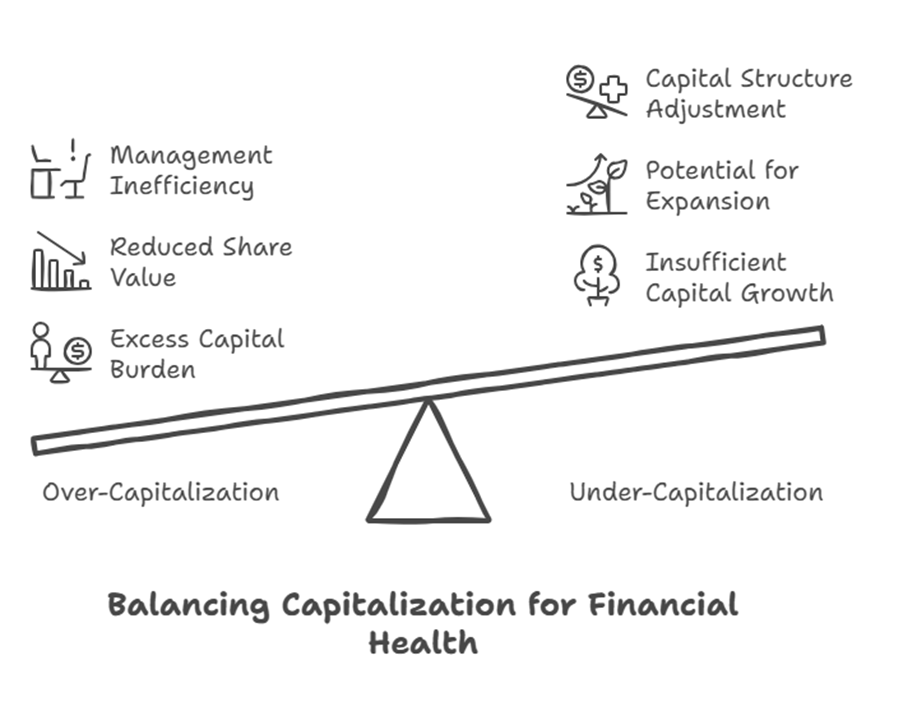

Based on the relationship between the capital structure and the earning capacity of the company, capitalization can be broadly classified into Over Capitalization and Under Capitalization. The sources also mention “Water Capitalization” but do not define it.

- Over-Capitalisation:

- Meaning: Over-capitalization is a situation where a firm has more capital than it needs or, in other words, assets are worth less than its issued share capital, and earnings are insufficient to pay dividend and interest. It means having more capital than actually required, and the funds are not properly used.

- Effects: Over-capitalization leads to several problems:

- It reduces the rate of earning capacity of the shares and can lead to a reduction of the dividend rate.

- It creates difficulties in obtaining necessary capital for the business.

- It leads to a fall in the market price of the shares.

- It creates problems on re-organization.

- It leads to the under or misutilization of available resources.

- Causes (implied by remedies): While not explicitly listed as causes, the remedies suggest potential contributing factors like inefficient management, high-dividend preference shares, or high debt levels. High rate of taxation and under estimation of capitalization rate are also listed under effects/causes in one place.

- Remedies: Over-capitalization can be reduced with the help of effective management and systematic design of the capital structure. Major steps include:

- Efficient management.

- Redemption of preference share capital which consists of a high rate of dividend.

- Reorganization of equity share capital.

- Reduction of debt capital.

- Severity: Over-capitalization is considered more dangerous to the company, shareholders, and society than under-capitalisation.

- Under-Capitalisation:

- Meaning: Under-capitalisation is the reverse of over-capitalisation. It is a state where a firm’s actual capitalization is lower than its proper capitalization as warranted by its earning capacity.

- Nature: Under-capitalisation is described as not an economic problem but a problem of adjusting capital structure.

- Severity: The situation of under-capitalisation can be handled more easily than the situation of over-capitalisation. It is considered less dangerous, but both situations are bad, and every company should strive to have a proper capitalisation.

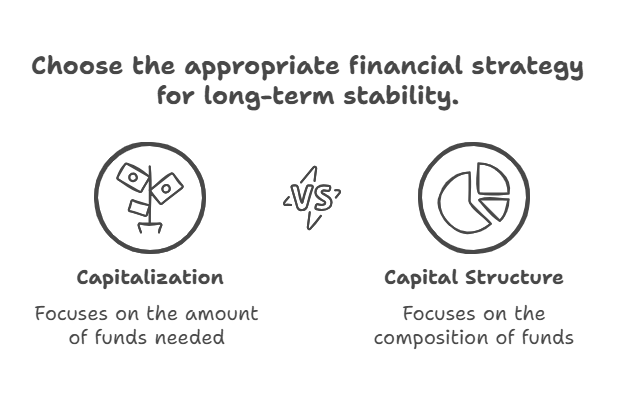

Capitalization vs. Capital Structure

While sometimes used interchangeably, the sources differentiate Capitalization and Capital Structure. Capitalization is about the amount of funds needed or represented by par value. Capital Structure of a company refers to the composition or make-up of its capitalization. It includes all long-term capital resources, viz, loans, bonds, shares and reserves. It is made up of debt and equity securities and refers to the permanent financing of a firm. The mix of various long-term sources of funds employed by a firm is called capital structure. These long-term sources include owner’s funds (equity share, preference shares, and retained earnings) and long-term debt (debentures and bonds).

Financial planning involves estimating the amount of capital to be raised and then determining the form and proportionate amount of securities, which aligns with designing the capital structure. The determination of the specific mix of these long-term funds (Capital Structure) is a major financing decision.

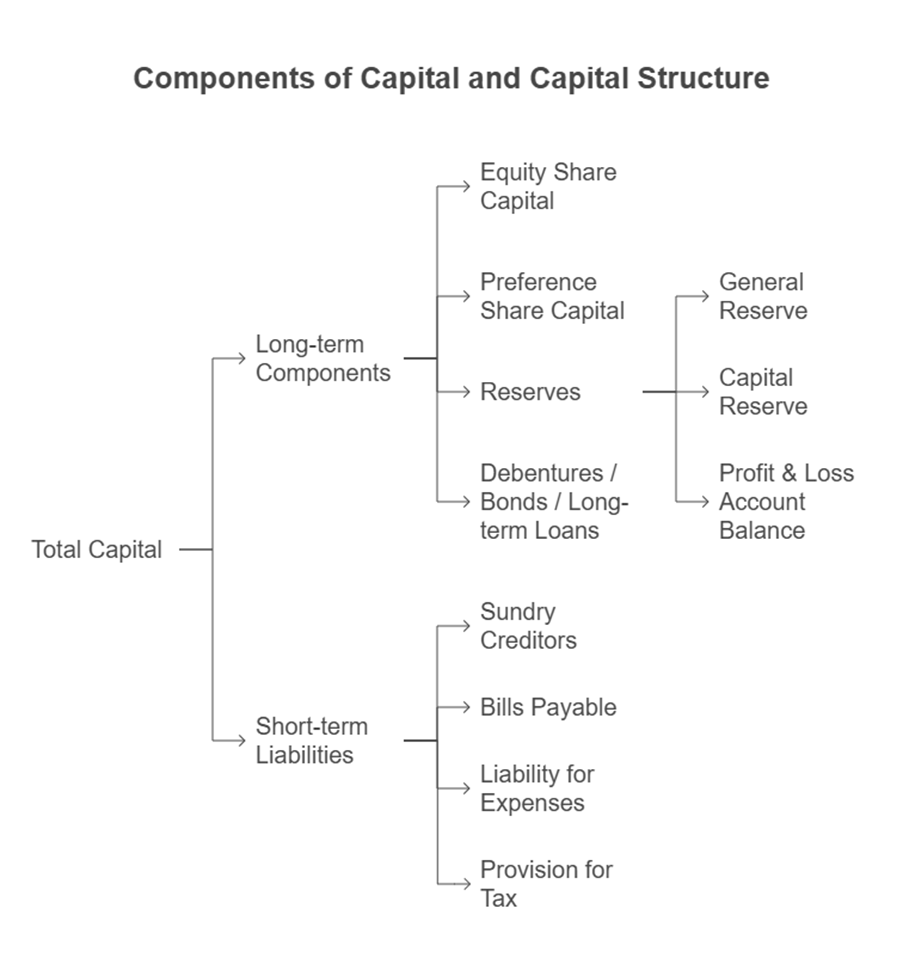

Components Contributing to Capital and Capital Structure

The total capital or the resources forming the capital structure are reflected in the liabilities side of the balance sheet, specifically the long-term components. Sources mention items like:

- Equity Share Capital

- Preference Share Capital

- Reserves (General Reserve, Capital Reserve, Profit & Loss Account balance/Retained Earnings)

- Debentures / Bonds / Long-term Loans

These components, particularly equity, preference shares, retained earnings, and long-term debt, constitute the capital structure used for permanent financing. Short-term liabilities like Sundry Creditors, Bills Payable, Liability for Expenses, and Provision for tax are typically current liabilities associated with working capital, though non-interest bearing current liabilities are sometimes excluded when calculating “Invested Capital” in valuation contexts.

Estimation and Management

Estimating capital requirements is a part of financial planning. This involves considering both fixed capital (for long-term assets) and working capital. Once the capital requirements are estimated, the appropriate capitalization value is determined, followed by designing the capital structure. Effective management and systematic design of capital structure are seen as ways to address over-capitalization.

In summary, Capital is the overall investment or wealth of the company. Capitalization is the process of determining the amount of funds needed and the value represented by the par value of shares and debentures. It’s distinct from Capital Structure, which is the specific mix of long-term sources like debt and equity used for permanent financing. Managing capitalization levels and the resulting capital structure is crucial for a company’s financial health, with both over- and under-capitalization posing risks, though over-capitalization is generally considered more detrimental.