Loan financing is a fundamental mode by which companies raise funds. It is considered a part of Creditorship Securities, which refers to finance mobilized from creditors. Unlike equity financing where funds come from owners, loan financing involves borrowing money from external parties who become creditors of the company. Debentures and Bonds are highlighted as two major parts of Creditorship Securities. A debenture is defined as a document issued by a company acknowledging a debt, serving as a certificate under the company’s seal as evidence of this debt. The Companies Act includes debenture stock, bonds, and other company securities within the definition of “debenture,” irrespective of whether they charge the company’s assets. Essentially, debentures and bonds are debt securities issued to raise long-term debt capital. A bond is a negotiable certificate that entitles the holder to repayment of the principal sum plus interest and is a debt security issued by a company or government agency.

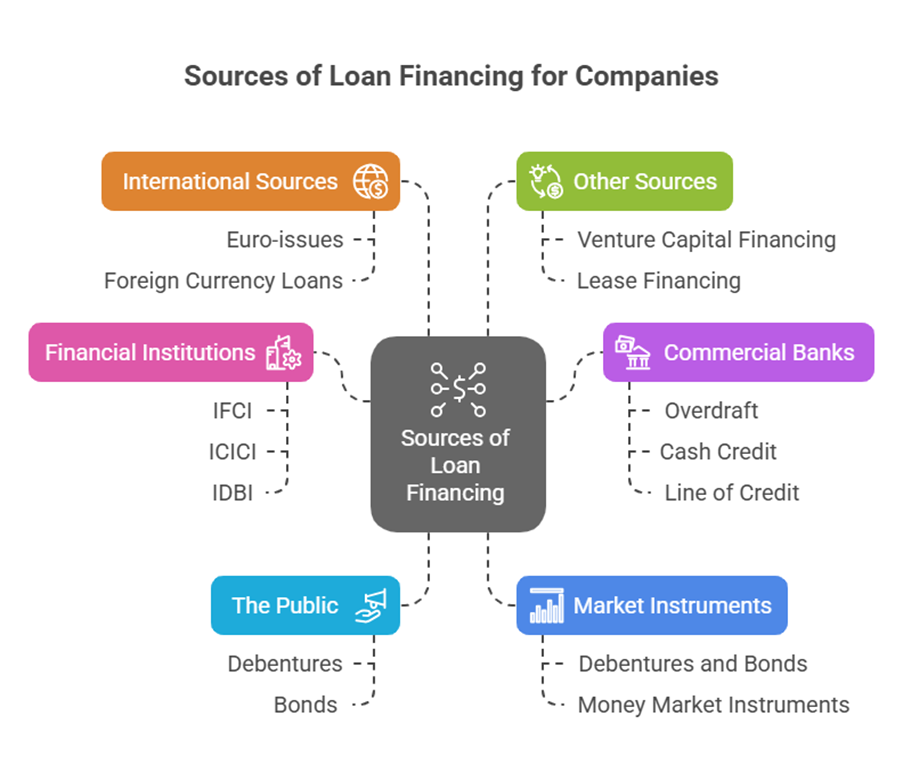

Sources of Loan Financing

Companies can obtain loan financing from various sources, categorized broadly by the tenure of the funds and the type of lender:

- Financial Institutions: These institutions play a key role in industrial development and meeting the financial requirements of business concerns. Nationwide and state-wide financial institutions were established to provide long-term financial assistance to industrial concerns. Examples of famous financial institutions include IFCI, ICICI, IDBI, SFC, and EXIM Bank. Loans from financial institutions are listed as a long-term source of finance. State Financial Corporations (SFCs) provide long and medium-term loans, often with limits based on the size and type of the industrial concern. IDBI also designs schemes like Seed Capital Assistance, which can involve interest-free loans initially.

- Commercial Banks: Commercial banks are significant providers of loan financing, particularly for short-term needs. They normally provide short-term finance repayable within a year, commonly in the form of short-term advances used for working capital requirements. Bank credit is considered a self-liquidating short-term financing, intended to carry the firm through seasonal peaks in financing need. Commercial banks also provide long-term loans. Various forms of bank credit exist to finance working capital, including Overdraft, Cash Credit, Bills Purchasing and Bills Discounting, Letter of Credit, Working Capital Term Loan, and Funded Interest Term Loan. Advances against goods (pledge, hypothecation) are an important and generally safe source of bank credit. A Line of Credit is a bank’s commitment to lend a certain maximum amount on demand. A Letter of Credit is a bank’s undertaking to pay against stipulated documents. Bank Guarantees are facilities extended by banks on behalf of clients.

- The Public: Companies can raise loans from the public by issuing debentures or bonds. Public deposits or fixed deposits from the public are also a source, typically considered medium-term (for a duration of three years is mentioned).

- Market Instruments:

- Debentures and Bonds: Issued by public limited companies, these are instruments for raising long-term capital with a fixed period of maturity. Bonds can be raised through Public Issue and Private Placement. They entitle the holder to repayment of the principal plus interest.

- Money Market Instruments: These are short-term debt instruments. Examples include Call/Notice Money Market (very short-term lending/borrowing without collateral), Treasury Bills (short-term government instruments), Commercial Bills, Commercial Papers (unsecured, short-term promissory notes issued by highly rated companies), Certificates of Deposits, Promissory Notes (short-term credit tools), and Collateralised Borrowing and Lending Obligation.

- International Sources: Indian companies with a good track record may raise funds by issuing debt capital in the international market. Sources include Euro-issues like Euro Debt Issue, Foreign currency loans, Syndicated Credits (large bank loans), and Foreign Currency Convertible Bonds (FCCBs).

- Other Sources:

- Venture Capital Financing: Although often associated with equity, venture capital can involve investment in debt securities from entrepreneurs undertaking risky ventures. Methods can include Conditional Loan and Income Notes (hybrid securities).

- Asset/Debt Securitization: This process can be used to address liquidity problems without altering the company’s debt-equity ratio by converting receivables into marketable securities.

- Lease Financing: While a contractual arrangement for asset use, a financial lease is long-term, non-cancellable, covers a major part of the asset’s life, and is regarded as a loan in disguise. It is an alternative to purchasing an asset with borrowed funds.

- Trade Credit: Credit provided by suppliers to customers, treated as accounts payable by the buying firm.

- Advances from Customers: Payments received from customers for goods or services not yet delivered.

- Inter Corporate Deposits: Business firms borrowing funds from other firms for a short period.

- Forfeiting: Discounting international trade receivables without recourse.

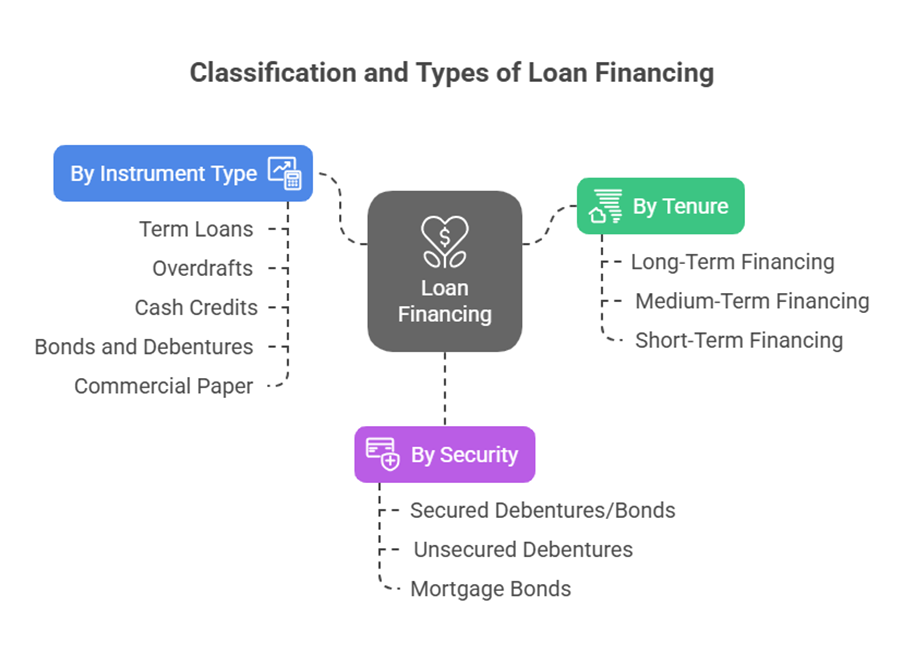

Classification and Types of Loan Financing

Loan financing can be classified based on various factors:

- By Tenure:

- Long-Term Financing: Required for capital expenditures like plant and machinery, and permanent working capital. Period exceeds 5 years, potentially 10-20 years. Sources include term loans from financial institutions and banks, debentures/bonds, and international long-term debt.

- Medium-Term Financing: Period is typically between 1 and 5 years. Sources include preference shares, debentures/bonds, public deposits (for up to 3 years), and medium-term loans from banks and financial institutions.

- Short-Term Financing: Period is less than 1 year. Required for working capital. Sources include trade credit, advances from commercial banks, commercial papers, treasury bills, commercial bills, certificates of deposits, promissory notes, and inter corporate deposits.

- By Security: Secured debentures/bonds are secured by a charge on assets. Unsecured (naked or simple) debentures are not given any security. Mortgage bonds are secured by a lien against property. Collateral may be required for bank advances.

- By Instrument Type: Specific instruments like Term Loans, Overdrafts, Cash Credits, Bills Purchased/Discounted, various types of Bonds and Debentures (as described in notes on Debentures), Commercial Paper, etc..

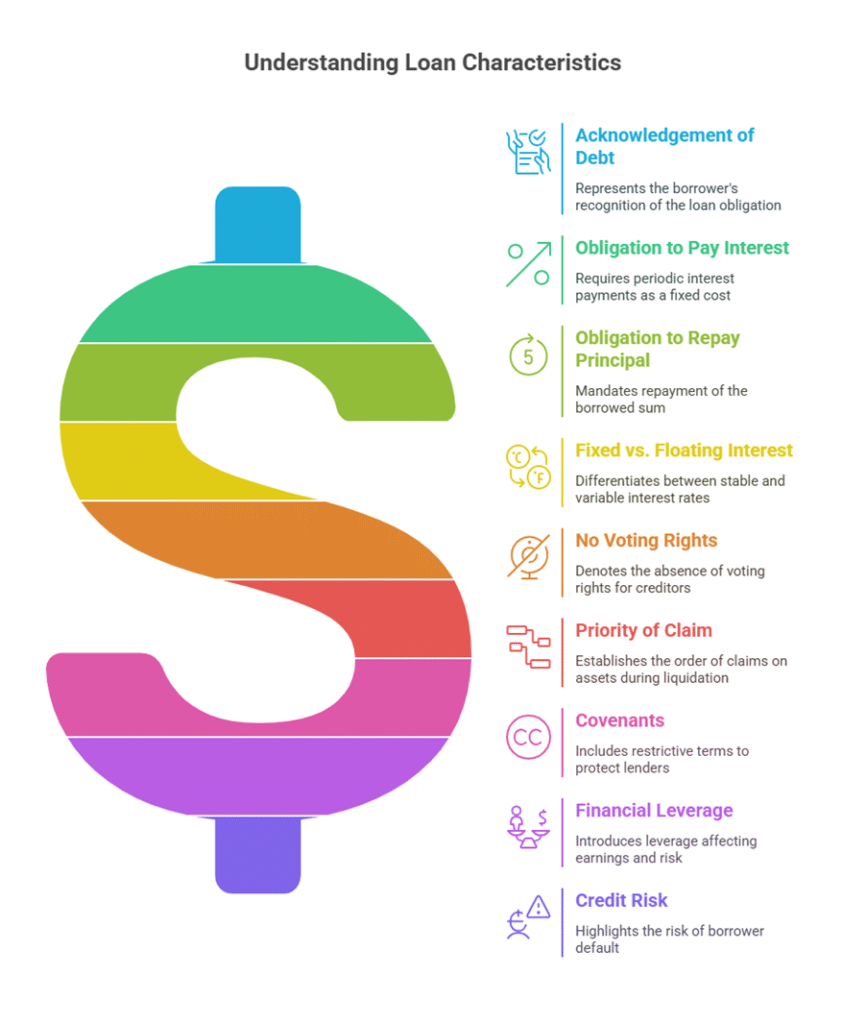

Key Features and Characteristics of Loans

Loan financing involves several defining characteristics:

- Acknowledgement of Debt: Loans represent an acknowledged debt by the company.

- Obligation to Pay Interest: Loan instruments typically require periodic interest payments. This interest is a fixed financing cost. Interest on loan payments must be made regardless of whether the company makes profits [implied by the nature of debt].

- Obligation to Repay Principal: The initial borrowed sum (principal) must be repaid according to the agreed terms, whether in instalments or as a lump sum at maturity.

- Fixed vs. Floating Interest: While some loans carry a fixed interest rate, others, like Syndicated Credits or arrangements covered by Forward Rate Agreements (FRAs), may have floating interest rates referenced to benchmark rates like LIBOR or SOFR. Interest rate risk can be managed using derivatives.

- No Voting Rights: Creditors, including loan holders, generally do not have voting rights in the company [implied by contrast with shareholders].

- Priority of Claim: Debenture holders and secured creditors have a priority of claim on the company’s income and assets over equity and preference shareholders, particularly during winding up.

- Covenants: Loan documents or bond issues may include covenants, which are restrictive terms put in place by lenders to protect themselves.

- Financial Leverage: Using debt financing, particularly interest on debt, introduces financial leverage, which can affect the level and variability of the firm’s earnings and overall risk. Borrowing affects leverage ratios like Borrowing/Shareholders funds and Borrowing/Value of firm.

- Credit Risk: A significant risk associated with loans is credit risk, the risk that an obligor (borrower) will default on any type of debt.

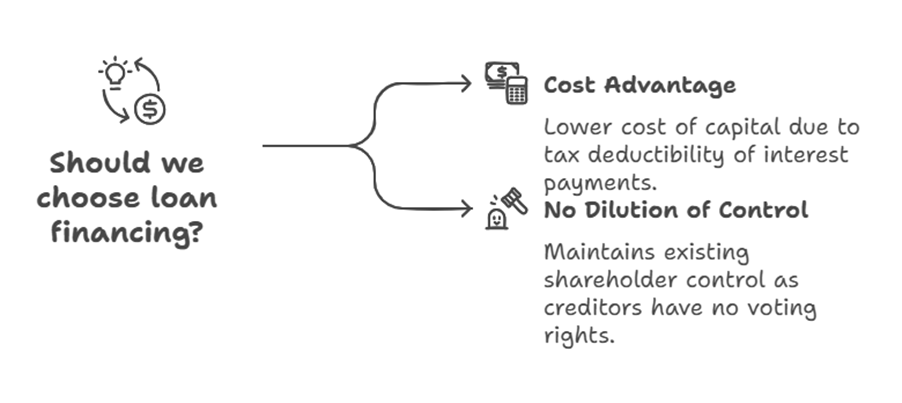

Advantages of Loan Financing

Based on the general nature of debt financing as discussed alongside equity and preference shares:

- Cost Advantage: The cost of debt capital can be lower than equity or preference capital, partly due to the tax deductibility of interest payments [implied by cost of capital calculations and discussions of tax].

- No Dilution of Control: Issuing debt does not dilute the control of existing shareholders as creditors do not have voting rights [implied].

Disadvantages of Loan Financing

- Obligatory Payments: Interest payments and principal repayments are mandatory regardless of the company’s financial health [implied by the nature of debt]. This contrasts with dividends, which are paid from profits.

- Increased Financial Risk: The fixed obligation to make payments increases the financial risk for the firm. Failure to meet these obligations can have severe consequences [implied].

- Repayment Burden: The need to repay the principal, especially a large sum at maturity, can be challenging for the company [implied].

- Restrictive Covenants: Loan agreements may impose restrictive covenants on the company’s operations or finances.

- Risk for Shareholders: If the return generated on the assets financed by debt is less than the cost of the debt, it can adversely affect the returns and increase the risk for shareholders [implied by financial leverage].

In summary, loan financing encompasses a wide range of debt instruments and sources, from short-term bank advances and money market instruments to long-term debentures, bonds, and institutional loans. While providing essential capital and potential cost benefits, particularly in avoiding equity dilution, it fundamentally carries the obligation of fixed payments and introduces significant financial risk for the borrowing entity. Concepts like credit rating and covenants are integral to understanding the terms and risks associated with loan financing.