Book building is presented as an important price discovery mechanism used by corporates issuing securities. Its fundamental purpose is to discover the price of the issuer’s securities. It is described as one of the ways of raising finance by a company.

Core Concept and Definition

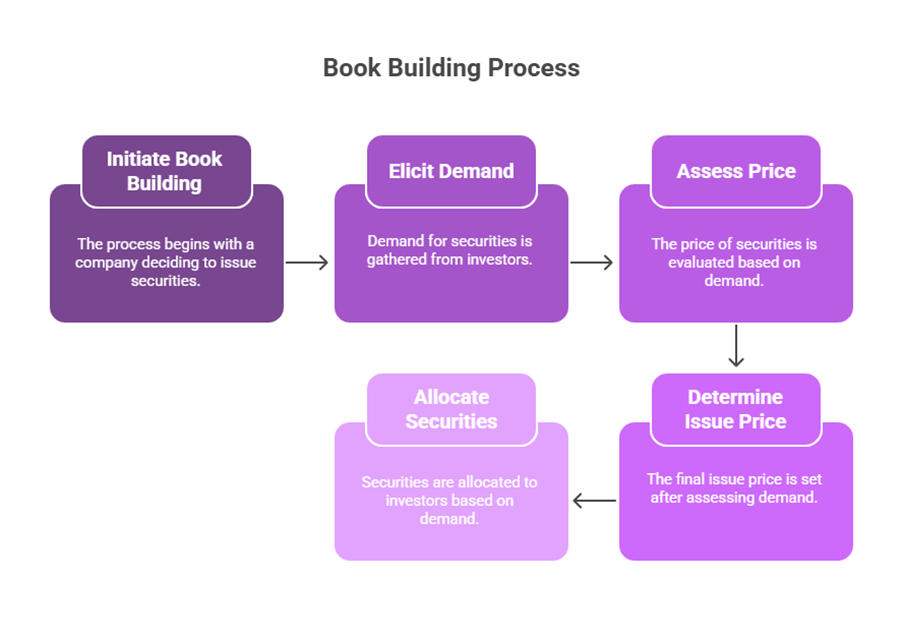

At its heart, book building is a process by which the demand for securities proposed to be issued by a body corporate is elicited and built up. During this process, the price for such securities is assessed for the determination of the quantum of such securities to be issued. The objective is to find the highest market clearing price.

According to SEBI’s definition, it is a process undertaken prior to the filing of the prospectus with the Registrar of Companies. The process involves collecting bids from investors at various prices within a specified price band during the offer period. The issue price is subsequently determined after the bid closure, based on the demand generated through this process. This method is directed towards both institutional investors and retail investors.

Book building is considered a mechanism where the issue price of a security is determined by the demand and supply forces in the capital market. It is a method used for marketing a public offer of equity shares of a company and is a common practice in most developed countries.

Purpose and Need

The process is undertaken primarily to determine investor appetite for a share at a particular price. Undertaken before making a public offer, it helps determine the issue price and the number of shares to be issued. The idea behind this process is to find a better price for the issue.

History and Regulation in India

Book building was introduced in India in public issues by SEBI in October 1995. This was based on the recommendations of the Malegoan Committee. Initially, the option of book building was available only to companies whose proposed public issue exceeded Rs. 100 crore. However, with effect from November 1996, the minimum size requirement for any company using the book building process has been removed. Despite this, for a 100 percent book building process for the issue of securities to the public through a prospectus, the issue of capital must be Rs. 25 crore and above.

The book-building system is specifically noted as being part of the Initial Public Offer (IPO) of the Indian Capital Market. It is described as the most practical, fast, and efficient management method for mega issues.

Key Participants

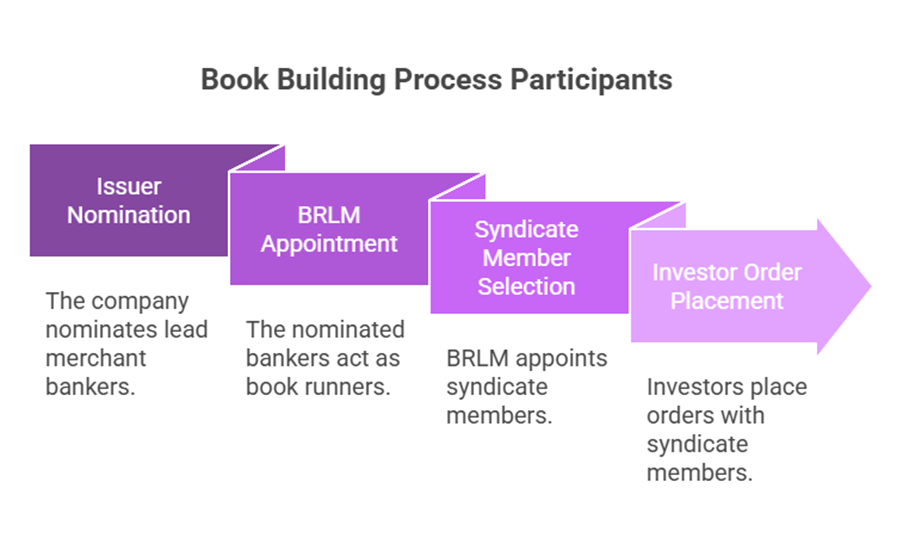

The principal intermediaries involved in a book building process are:

- The company (the Issuer).

- The Book Running Lead Manager (BRLM). The issuer nominates lead merchant banker(s) to act as book runners.

- Syndicate members. These members are appointed by the BRLM. They are intermediaries registered with SEBI and eligible to act as underwriters. Investors place their orders with these syndicate members.

Process and Mechanism

The process follows a defined sequence of steps:

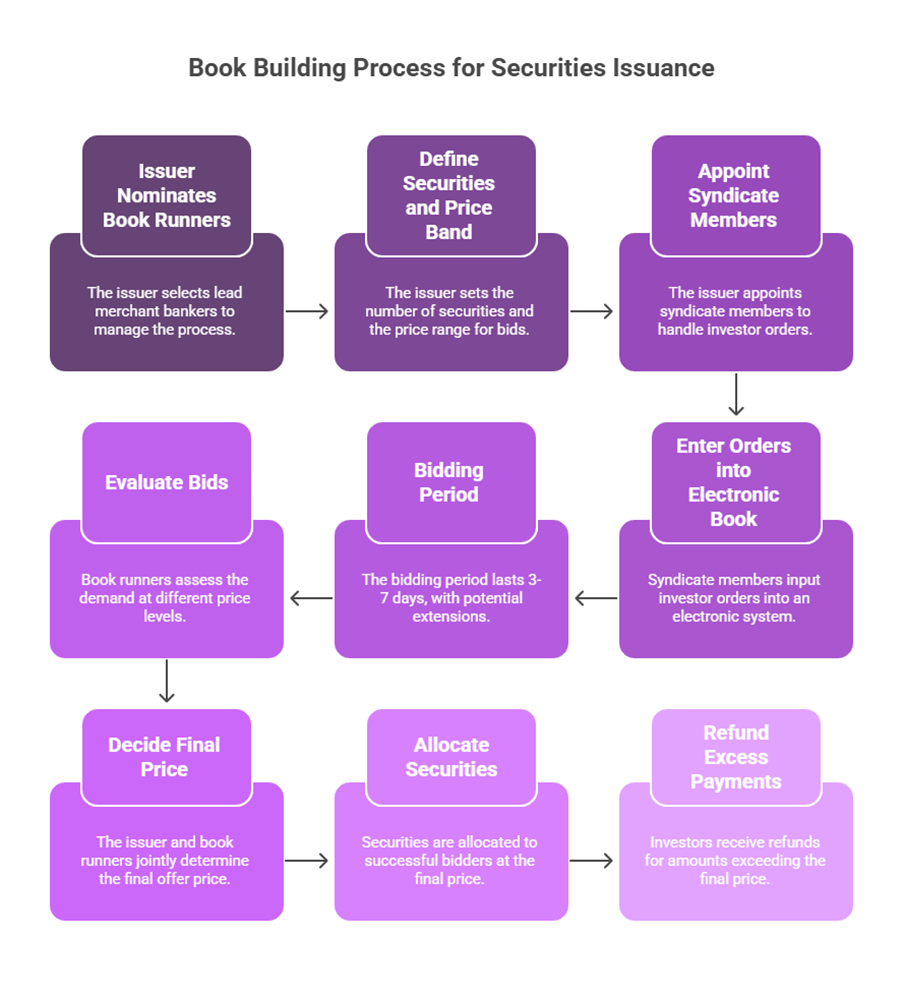

- The Issuer planning an offer nominates lead merchant banker(s) to act as ‘book runners’.

- The Issuer specifies the number of securities to be issued and defines the price band for the bids. This price band consists of a lowest price as the floor price and a highest price as the cap price.

- The Issuer also appoints syndicate members with whom investors can place their orders.

- The syndicate members enter the orders received from investors into an ‘electronic book’. This process is referred to as ‘bidding’ and is described as being similar to an open auction.

- The book for receiving bids normally remains open for a period of at least 3 days and not more than 7 days. If the price band is revised during this period, an additional 3 days are allowed for bidding, subject to a maximum total period of 10 days.

- Bids must be entered by investors within the specified price band.

- Bidders have the ability to revise their bids before the book closes.

- Upon the closure of the book building period, the book runners evaluate the bids based on the demand generated at various price levels.

- The book runners and the Issuer jointly decide the final price at which the securities will be issued. This final offer price is also known as the cut off price.

- Generally, the number of shares offered is fixed. The total issue size is then determined or ‘frozen’ based on the final price per share that is decided.

- Allocation of securities is made to the successful bidders whose bids meet the final price. Other bidders who do not receive an allotment get refund orders. If the price quoted by an investor is less than the final price, they will not receive an allotment. If the price quoted is higher than the final price and they receive an allotment, the amount paid in excess of the final price is refunded. The final price is defined as the equilibrium price or the highest price at which all the shares on offer can be sold smoothly.

It is noted that the company requires at least 30 centres for the book building process to raise share capital from the market. Sufficient opportunities are to be provided to investors to participate through the terminal.

Within the book building process for the net offer to the public, a company can choose to offer 100 percent of the net offer through book building, or offer 75 percent through book building and the remaining 25 percent at the price determined through the book building process (this fixed portion is conducted like a normal public issue after the price is set). The 75% route was specified early in the process in India, and then the 100% route was opened to the public.

Regarding minimum application size, while discussed under the “Book Building” heading, the sources mention minimum application sizes (100, hiked to 500, then brought down to 200) in the context of subscribing to the issue of share capital generally. This likely pertains to the post-pricing application stage rather than the bidding phase itself, though it’s listed alongside book-building details.

Comparison with Fixed Price Method

The sources highlight key differences between the book building method and the fixed price method:

- In the fixed price method, the issue price is decided right at the start, and investors must buy shares at this predetermined price, without the option to choose a price. In contrast, in book building, the issue price is not decided initially; investors bid within a specified price range (20% price band). The issue price is fixed only after evaluating the demand generated at various price levels.

- Under the fixed price method, the total demand for the issue is known only after the issue closes. In the book building method, the demand is known every day during the offer period.

Advantages of Book Building

The sources list several advantages of using the book building process:

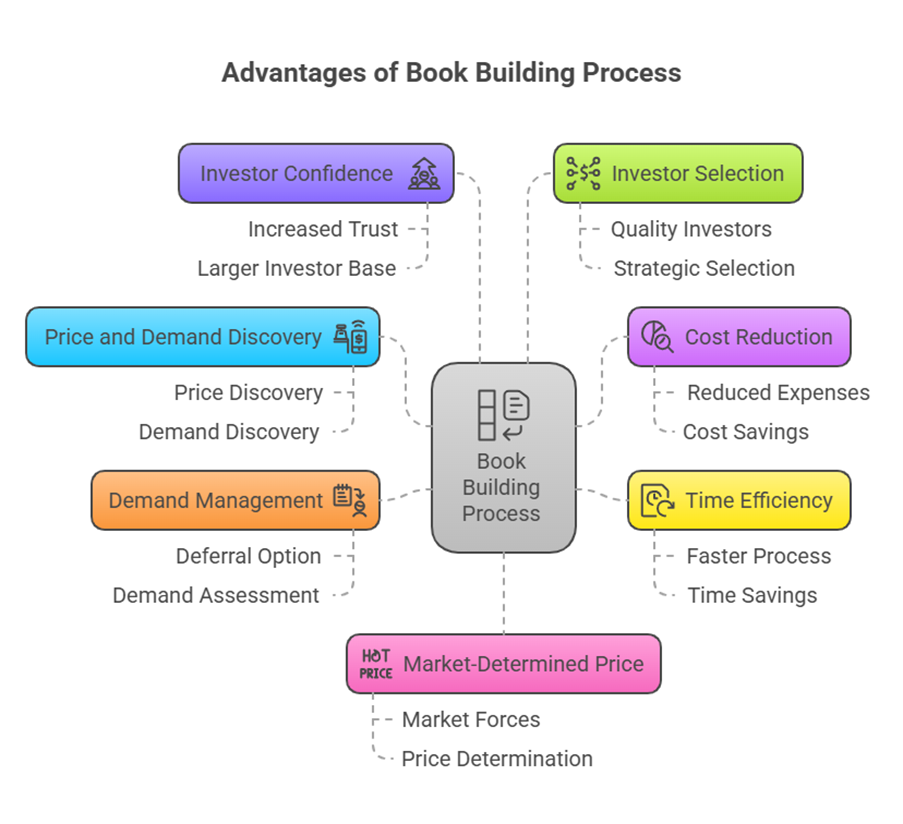

- It facilitates the discovery of price and demand for the securities.

- The costs of the public issue are much reduced compared to a normal public issue.

- The time taken for completing the entire process is significantly less than that in a normal public issue.

- Because demand is known before the issue closes, if the demand is insufficient, the issue can potentially be deferred.

- It is said to inspire investors’ confidence, leading to a larger investor universe.

- Issuers have the ability to choose investors by quality.

- The issue price is market determined.

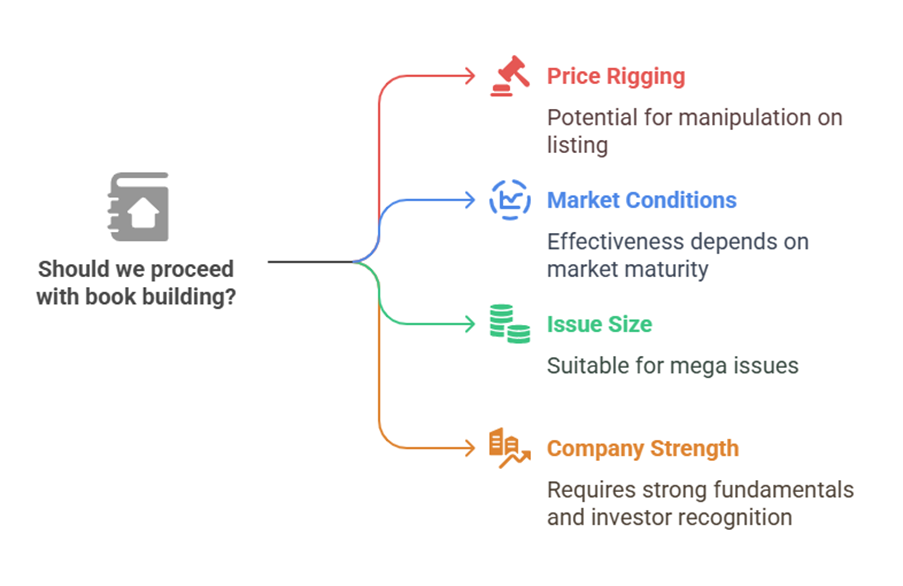

Disadvantages of Book Building

Despite its advantages, book building also has potential disadvantages according to the sources:

- There is a possibility of price rigging on listing, potentially as promoters might attempt to assist or bail out syndicate members.

- The system is stated to work very efficiently mainly in matured market conditions. Such conditions are not always commonly found in practice.

- It is considered appropriate primarily for mega issues, although the minimum size restriction was largely removed in India, except for 100% book built issues.

- The success of the book building process depends on the company being fundamentally strong and well known to investors. Without these factors, the process is likely to be unsuccessful.

In summary, book building is a dynamic, market-driven process for issuing securities, primarily aimed at discovering the optimal price and assessing demand before the final offer. Introduced in India based on expert recommendations, it involves key intermediaries working within a regulated framework to manage bids and determine a market-clearing price, offering distinct benefits and drawbacks compared to traditional fixed-price issues.