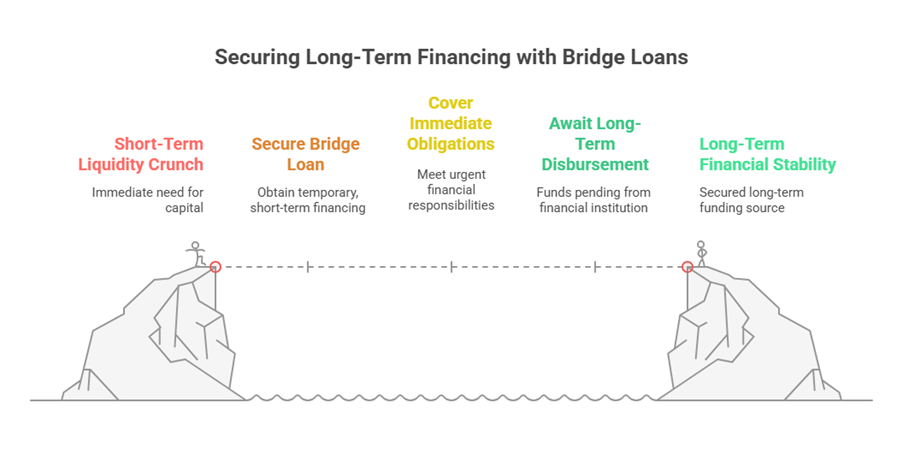

Bridge financing is described as a form of temporary financing. Its primary purpose is to cover a company’s short-term costs until regular long-term financing is secured. The term “bridge financing” is used because it acts like a bridge that connects a company to debt capital through short-term borrowings.

Core Concept and Purpose

The need for bridge financing arises when an institution or company requires capital urgently to meet immediate short-term obligations, such as working capital financing. A common scenario is when a company has been sanctioned a long-term loan from a bank or financial institution, but the disbursement of the funds is scheduled for a future date or in instalments. For example, if a company is sanctioned a ₹100 crore loan payable in four instalments, with the first instalment due in three months, but needs funds at the moment to operate, it can seek a three-month bridge loan. This bridge loan provides the necessary money to survive and operate until the first instalment of the long-term credit is received.

Another significant use of bridge financing is before a company goes public through an Initial Public Offering (IPO). Companies use bridge financing to cover flotation expenses related to the IPO, such as underwriting fees and payments to the stock exchange,. These expenses need to be incurred before the company actually raises money from the public offering.

Bridge finance refers specifically to loans taken by a company normally from commercial banks for a short period because of pending disbursement of loans sanctioned by financial institutions. Even though it is short-term in nature, it is considered an important step in the facilitation of long-term loan. Financial institutions often take time to disburse approved loans to companies. To avoid losing time in starting their projects after loan approval, companies arrange these short-term bridge loans from commercial banks. The bridge loans are designed to be repaid or adjusted out of the term loans as and when they are disbursed by the concerned institutions.

Key Features and Characteristics

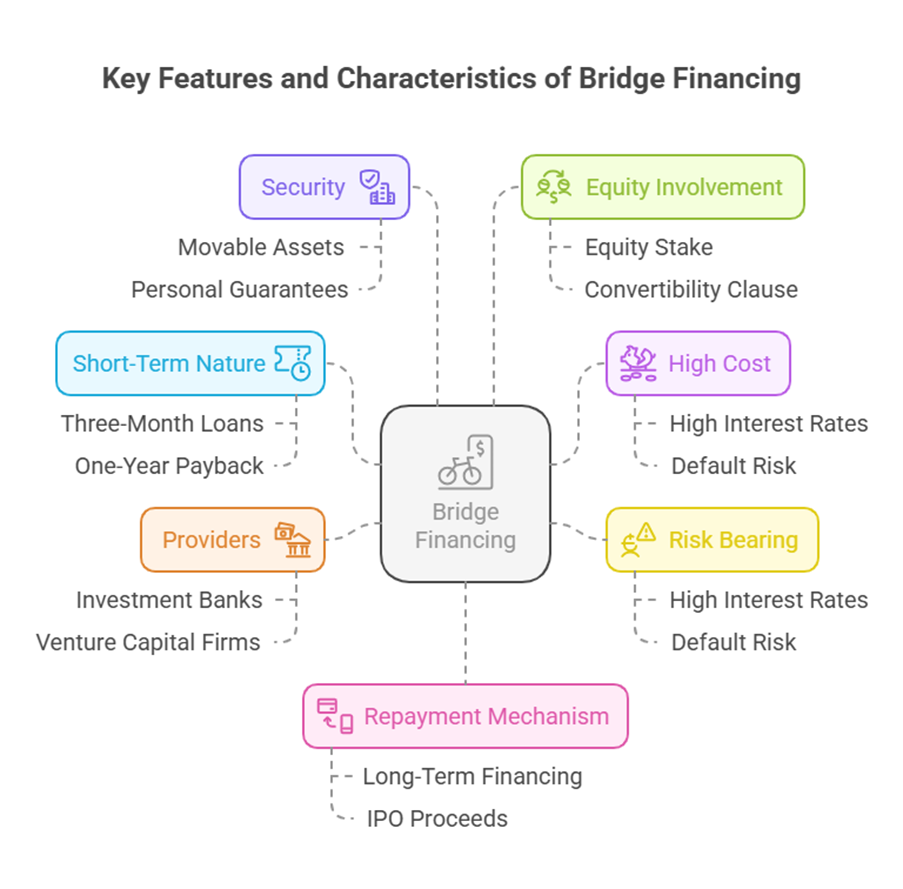

Bridge financing has several distinct features:

- Short-Term Nature: It is explicitly defined as short-term financing,. Its duration is temporary, typically covering a period until long-term financing is secured or a sanctioned loan is disbursed. In the context of covering the gap before the first instalment of a long-term loan, a three-month bridge loan is mentioned as an example. For equity bridge financing involving venture capital firms, a full payback is often required within one year.

- High Cost: Bridge loans are generally considered expensive,. Lenders demand a very high interest rate. This high cost is attributed to the significant portion of default risk that lenders bear when loaning funds for a short period. Venture capital firms, for instance, might charge a 20% interest rate for financing, potentially increasing to 25% per annum if the borrower fails to repay on time. Generally, the rate of interest on bridge finance is higher as compared with that on term loans.

- Risk Bearing: Lenders in bridge financing arrangements bear a notable risk of default. This is reflected in the high interest rates charged.

- Providers: Bridge loans are usually issued by investment banks or venture capital firms. Commercial banks are also noted as sources for bridge finance, particularly to cover the gap before financial institution loans are disbursed. Investment banks often provide bridge funds to cover IPO expenses when they are underwriting the stock issue.

- Security: Bridge loans are normally secured. The security commonly includes hypothecating movable assets, personal guarantees, and demand promissory notes.

- Potential for Equity Involvement: Equity financing can be an option for bridge financing, sometimes termed equity-for-capital swap. Equity bridge financing involves the lender exchanging capital for an equity stake in the borrowing company. This can occur when the high interest rates on bridge loans are prohibitive, leading the company to offer equity ownership to a venture capital firm in exchange for funds. Venture capital firms providing bridge finance may also include a convertibility clause, giving them the option to convert a certain credit amount into equity at a specified price.

- Repayment Mechanism: Bridge loans are repaid once the expected long-term financing is secured. In the case of pending loan disbursements, the bridge loans are repaid or adjusted when the term loans are disbursed. After an IPO, the bridge funds covering flotation costs are typically paid off immediately from the money raised.

Applications

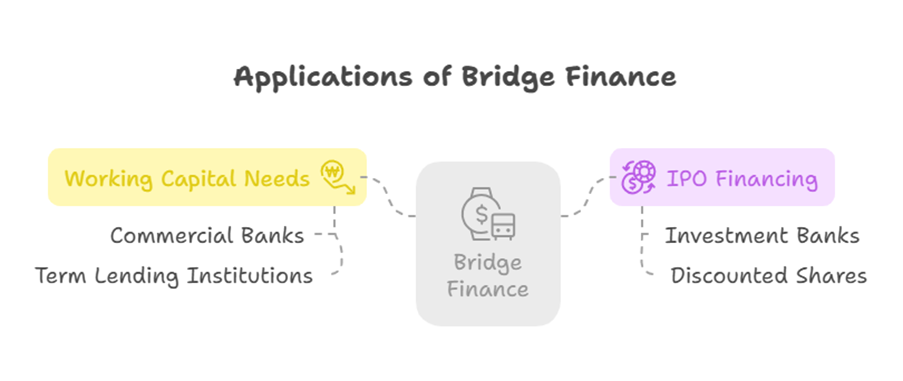

As highlighted, the main applications covered in the sources are:

- Covering short-term working capital needs while awaiting the first or subsequent disbursements of a sanctioned long-term loan,.

- Financing the flotation expenses incurred before an Initial Public Offering (IPO),.

In the IPO context, the bridge funds are often provided by the investment bank that is underwriting the new stock issue. The company might initiate a number of shares to the bank at a discount as part of this arrangement.

In the context of facilitating long-term loans, bridge finance is arranged from commercial banks to bridge the time gap between the sanction and actual disbursement of loans by term lending institutions, allowing companies to avoid delays in starting their projects.

Summary

Bridge finance serves as a critical, albeit temporary and costly, financial tool. It bridges the gap between an immediate need for funds and the eventual receipt of anticipated long-term financing. Whether used to cover the lag before a large loan disbursement or to fund IPO expenses, it is characterized by its short duration, high interest rates due to perceived risk, typical provision by investment banks, venture capitalists, or commercial banks, and is usually secured. Equity may sometimes be involved, particularly with venture capital lenders. The repayment is directly tied to the realization of the expected long-term funds.