Capital budgeting, also referred to as investment decision-making, is a crucial area within financial management. It involves the firm’s decision to invest its current funds most efficiently in long-term activities with the anticipation of receiving a flow of future benefits over a series of years. This area is concerned with the optimum utilization of funds to maximize the wealth of the organization and, in turn, the wealth of its shareholders.

Importance and Nature of Capital Budgeting Decisions

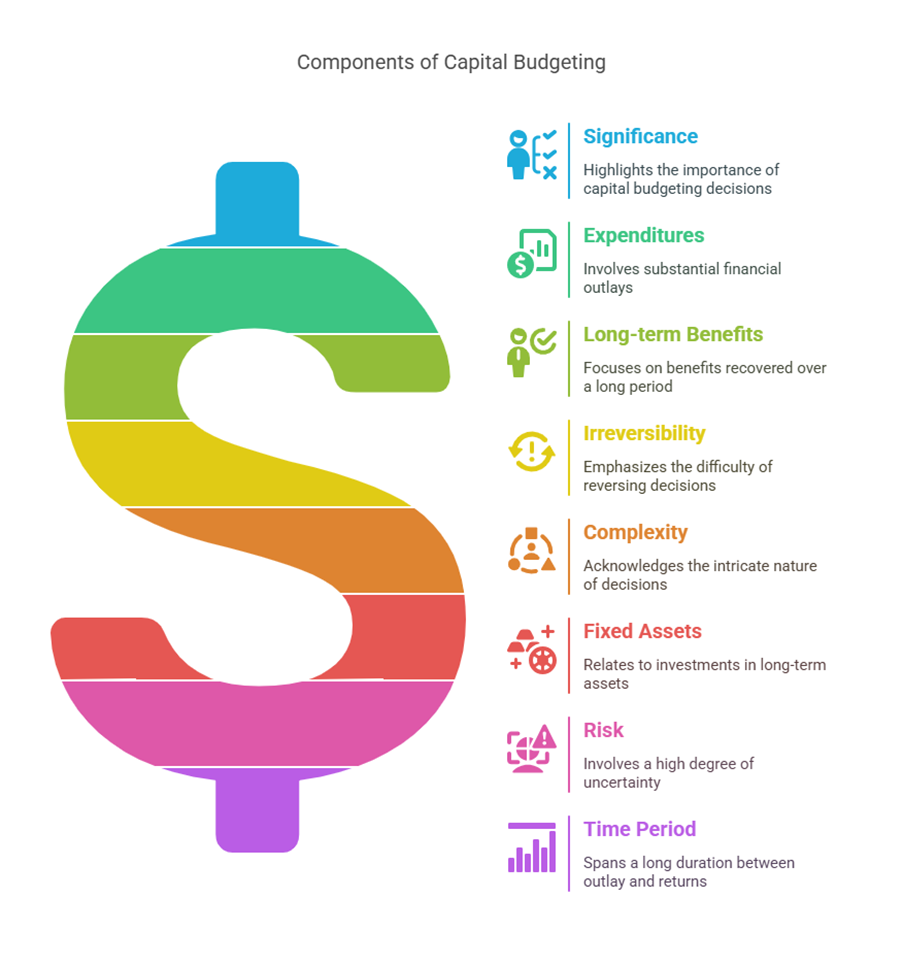

Capital budgeting decisions are highly significant, crucial, and critical business decisions for several reasons. They typically involve substantial expenditures. The benefits from these investments are recovered over a long period. Capital investment decisions are often irreversible, and the complexity involved in them requires proper care. These decisions relate primarily to fixed assets or long-term assets that are expected to operate and yield a return for more than one year. They require a current outlay or series of outlays of cash resources in exchange for an anticipated flow of future benefits.

The basic features of capital budgeting decisions include potentially large anticipated benefits, a relatively high degree of risk, and a relatively long time period between the initial outlay and the anticipated returns. Capital budgeting is not just about earning profit but is essential for generating revenue and ensuring the long-term existence of an organization, even for non-profit entities aiming to fulfil their mission.

The need for capital budgeting decisions generally arises for purposes such as expansion, diversification, or deciding whether to buy or lease assets. For example, diversification into new production lines or adding new lines requires large long-term investment funds. Similarly, the decision to acquire equipment and buildings on lease versus buying involves comparing the costs and benefits of periodic rental payments versus a large initial investment to determine the better course of action.

The Capital Budgeting Process

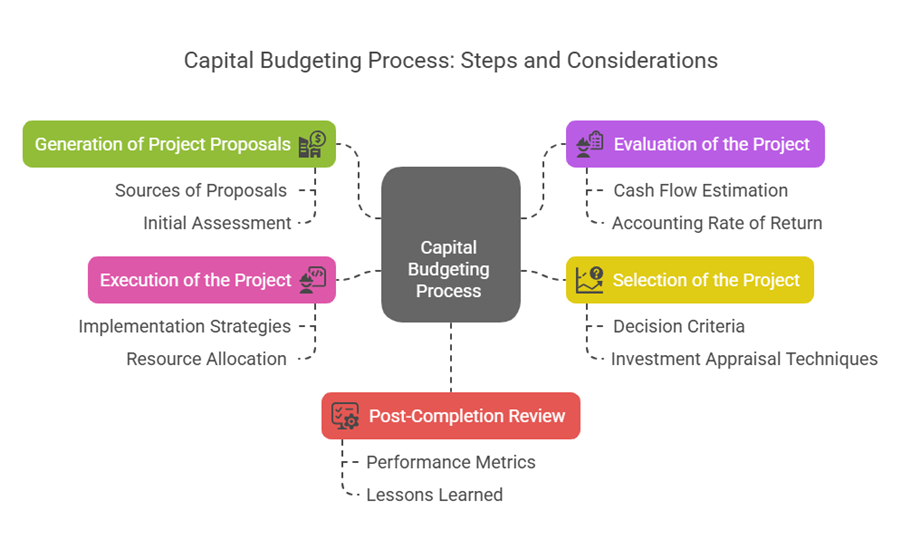

The process of capital budgeting involves several key steps, aimed at ensuring that each rupee raised, which bears some cost (cost of capital), is invested in a very prudent manner. Proper planning for capital investment is done through a structured budgeting process.

The major steps in the capital budgeting process include:

- Generation of project proposals. This is the initial phase where potential investment opportunities are identified. Proposals can originate from various sources depending on the firm’s nature.

- Evaluation of the project. This phase involves assessing the potential effect of the opportunity on the firm’s fortunes and the management’s ability to exploit it. Proposals with little merit are rejected, while promising ones advance for detailed evaluation. This step involves determining the project’s investments, inflows, and outflows. It requires the estimation of cash flows over the entire life for each project under consideration. One of the most important tasks in capital budgeting is estimating future cash flows for a project, as the final decision’s accuracy depends on the reliability of these estimates. While some techniques like Accounting Rate of Return (ARR) use accounting profit, capital budgeting analysis primarily considers incremental cash flows. Accounting profit has limitations; timing of cash flow may not match profit periods, and non-cash items like depreciation don’t involve immediate cash outflow. Therefore, it is important to evaluate projects based on after-tax cash incremental flows rather than accounting data. Cash flow estimation needs to consider all relevant cash inflows and outflows associated with the project.

- Selection of the project. This involves evaluating each alternative proposal using different decision criteria. Investment appraisal techniques are applied to appraise the proposals. The technique selected should enable the manager to make the best decision based on prevailing circumstances.

- Execution of the project. After selection, the chosen project is implemented.

- Post-completion review (implied, as process involves planning and control).

Another perspective on the steps of capital budgeting procedure lists:

- Estimation of Cash flows over the entire life for each of the projects under consideration.

- Evaluate each of the alternative, using different decision criteria.

- Determining the minimum required rate of return (i.e., WACC) to be used as discount rate.

Capital Budgeting Appraisal Methods

Various techniques are available for the appraisal of investment proposals to help companies decide the desirability of a proposal and rank them based on their relative income-generating capacity. These methods should enable the measurement of the real worth of the investment proposal and should possess several good characteristics, such as considering all cash flows, accounting for the time value of money, incorporating risk, and providing a clear acceptance/rejection criterion.

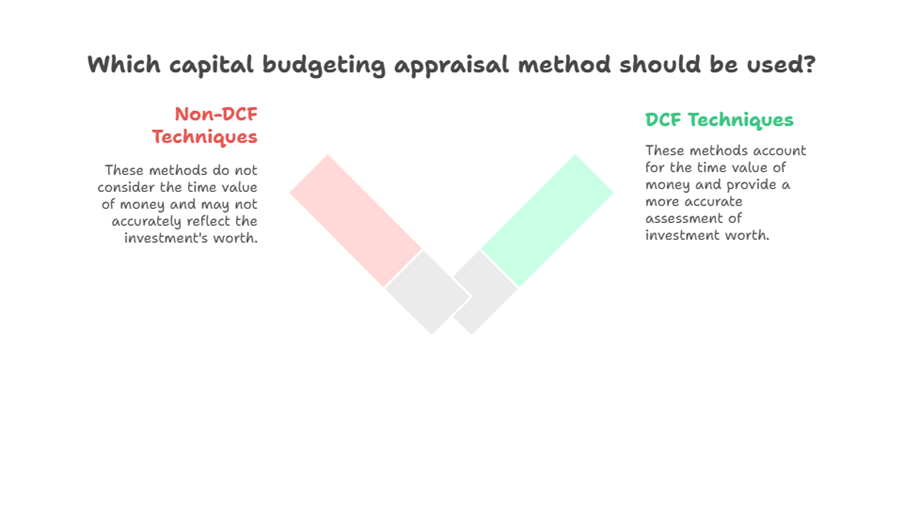

Capital budgeting appraisal methods can be classified into two broad categories: Traditional or Non-Discounted Cash Flow (Non-DCF) Techniques and Discounted Cash Flow (DCF) or Time-Adjusted Techniques.

A. Traditional or Non-Discounted Cash Flow (Non-DCF) Techniques

These methods determine the desirability of an investment project based on its useful life and expected returns, often using accounting information. A major limitation is that they do not take into account the concept of ‘time value of money’, which is significant for evaluating a project’s present value.

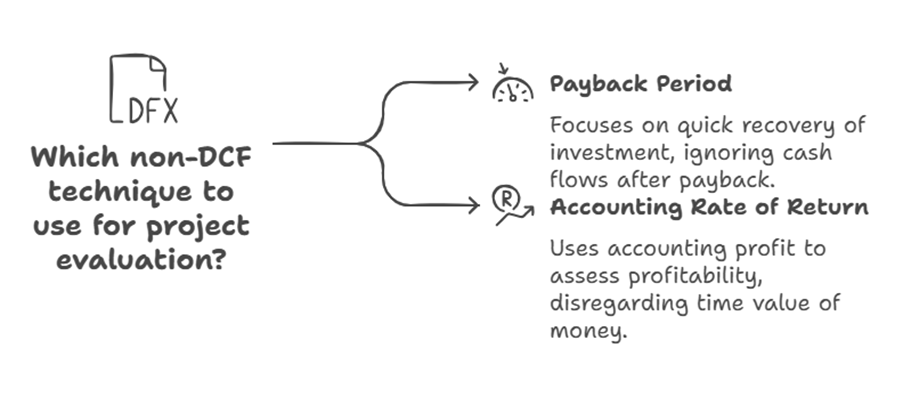

- Payback Period

- Concept: The payback period is the time required for the cumulative cash inflows from a project to equal the initial investment. It measures how quickly the initial outlay is recovered.

- Principle: Projects with shorter payback periods are generally preferred because they recover the investment faster, implying lower risk and higher liquidity.

- Decision Rule: For independent projects, accept the project if its payback period is less than a predetermined maximum acceptable period. For mutually exclusive projects, the one with the shortest payback period is often preferred.

- Disadvantages: A significant limitation is that it ignores cash flows received after the payback period. It also fails to consider the time value of money.

- Accounting Rate of Return (ARR)

- Concept: The Accounting Rate of Return (ARR), also known as Average Rate of Return, expresses the project’s profitability as a percentage of the investment. It is calculated using accounting profit (or earnings after tax) rather than cash flows.

- Calculation: ARR is typically calculated as (Average Annual Profit after Tax / Average Investment) * 100. Average investment might be calculated as ½ (Initial investment – Salvage value) + Salvage value.

- Decision Rule: For independent projects, accept the project if its ARR is higher than a predetermined required rate of return or target rate. For mutually exclusive projects, the one with the highest ARR is often preferred.

- Limitations: ARR suffers from using accounting profit instead of cash flows and does not consider the time value of money.

B. Discounted Cash Flow (DCF) or Time-Adjusted Techniques

These techniques are considered more sophisticated as they take into account the time value of money by discounting future cash flows to their Present Value. They discount cash flows using a predetermined discount rate, often the Weighted Average Cost of Capital (WACC), which represents the minimum required rate of return.

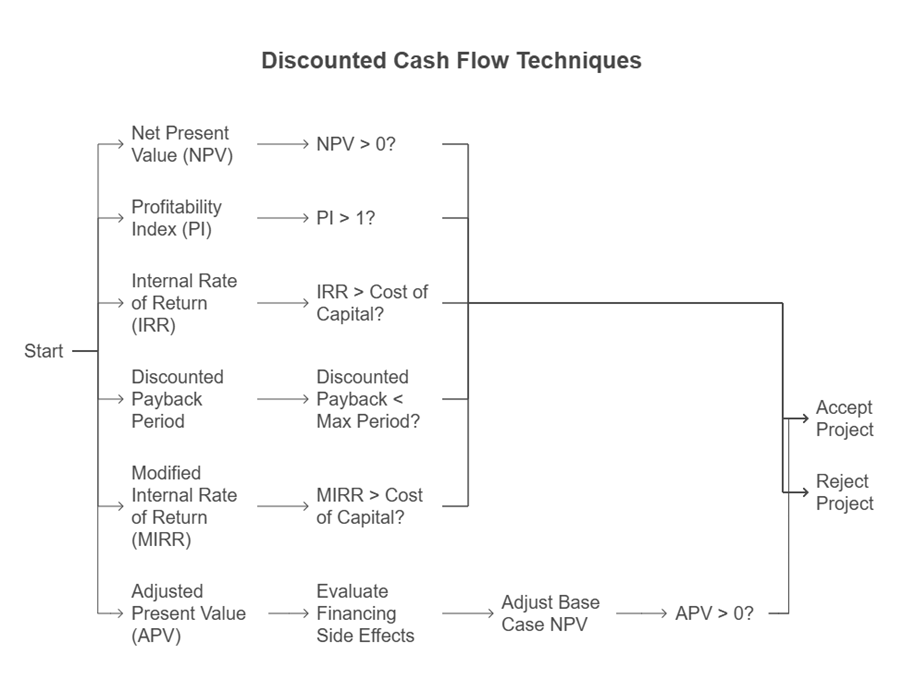

- Net Present Value (NPV)

- Concept: NPV is a classic method that calculates the present value of a project’s cash flows using the opportunity cost of capital (or required rate of return) as the discount rate. The net present value is then found by subtracting the initial investment (or present value of cash outflows) from the present value of cash inflows.

- Principle: NPV is based on the concept that a project should generate returns greater than the cost of the capital used to finance it. It correctly recognizes that cash flows occurring at different times have different values and should be compared only after converting them to their present values.

- Calculation: NPV = (Sum of the present values of future cash inflows) – (Initial cash outlay or present value of cash outflows). The present value of future cash flows is calculated using the formula: V0 = C1/(1+K)^1 + C2/(1+K)^2 + … + Cn/(1+K)^n, where V0 is the present value, C is the cash flow, K is the discount rate (cost of capital), and n is the time period.

- Decision Rule: For independent projects, accept the project if its NPV is positive (NPV > 0). A positive NPV indicates that the project is expected to generate returns exceeding the cost of capital, thereby increasing the firm’s value. For mutually exclusive projects, the one with the highest positive NPV should be accepted.

- Advantages: Considers the time value of money. Includes all cash flows over the project’s life. Provides a direct measure of the increase in firm value.

- Disadvantages: Requires determining the appropriate discount rate (cost of capital).

- Profitability Index (PI)

- Concept: The Profitability Index, also known as the Desirability Factor or Present Value Index Method, is the ratio of the present value of cash inflows to the initial cash outlay (or total discounted cash outflow).

- Calculation: PI = (Sum of discounted cash inflows) / (Initial cash outlay or Total discounted cash outflow).

- Decision Rule: For independent projects, accept the project if its PI is greater than 1 (PI > 1). A PI greater than 1 indicates that the present value of benefits exceeds the cost. For mutually exclusive projects, the one with the highest PI should be accepted.

- Relationship with NPV: A project with a positive NPV will have a PI greater than 1, and a project with a negative NPV will have a PI less than 1. They generally lead to the same acceptance-rejection decision for independent projects. However, they may conflict when ranking mutually exclusive projects, particularly under capital rationing.

- Advantages: Considers the time value of money. Includes all cash flows. Useful in capital rationing decisions for ranking projects, especially divisible ones.

- Disadvantages: Requires determining the appropriate discount rate. May conflict with NPV in ranking mutually exclusive projects.

- Internal Rate of Return (IRR)

- Concept: The Internal Rate of Return (IRR) is the discount rate that makes the Net Present Value (NPV) of a project’s cash flows equal to zero. It represents the rate of return that the project is expected to earn.

- Calculation: IRR is found by solving for the discount rate (K) in the NPV equation such that: Initial Outlay = C1/(1+K)^1 + C2/(1+K)^2 + … + Cn/(1+K)^n. This often requires iterative calculations or interpolation.

- Decision Rule: For independent projects, accept the project if its IRR is greater than the required rate of return or cost of capital (IRR > Cost of Capital). For mutually exclusive projects, the one with the highest IRR is generally preferred.

- Advantages: Considers the time value of money. Includes all cash flows. Provides a single rate of return measure that is easy to understand.

- Disadvantages: May lead to multiple IRRs for non-conventional cash flow patterns (where cash flows change sign more than once). Can conflict with NPV when ranking mutually exclusive projects, especially if they differ in scale or cash flow patterns. Assumes that intermediate cash flows are reinvested at the IRR, which may not be realistic.

- Discounted Payback Period

- Concept: Similar to the traditional payback period, but it calculates the time required to recover the initial investment using the present values of the expected cash flows.

- Principle: This method incorporates the time value of money while still focusing on the liquidity aspect (speed of recovery).

- Decision Rule: Accept projects if the discounted payback period is less than a predetermined maximum acceptable period.

- Advantages: Considers the time value of money. Provides information about how long funds will be tied up.

- Disadvantages: Still ignores cash flows received after the discounted payback period.

- Modified Internal Rate of Return (MIRR)

- Concept: MIRR is a variation of the IRR that addresses some of its limitations, particularly the reinvestment rate assumption and the possibility of multiple IRRs. It assumes that cash inflows are reinvested at the cost of capital (or another specified rate) rather than the IRR itself.

- Calculation: MIRR is the discount rate that equates the initial investment to the present value of the terminal value of the project’s cash flows, where the terminal value is the future value of the cash inflows compounded at the reinvestment rate.

- Decision Rule: Accept projects if the MIRR is greater than the cost of capital.

- Advantages: Addresses the unrealistic reinvestment rate assumption of the traditional IRR. Avoids the problem of multiple IRRs.

- Disadvantages: Requires determining an appropriate reinvestment rate.

- Adjusted Present Value (APV)

- Concept: APV is a valuation method used in capital budgeting that separates the value of the project itself from the value of its financing side effects. It is calculated by first determining the project’s value assuming it is financed purely by equity (the base case NPV) and then adding the present value of financing side effects (such as the tax shield from debt).

- Principle: Useful in situations where the financing mix and its associated benefits (like tax shields) change over the project’s life or are not proportionate to the project’s risk.

- Calculation: APV = Base Case NPV (assuming all-equity financing) + Present Value of Financing Side Effects.

- Advantages: Can be more flexible than WACC when financing structure is complex or changes over time. Clearly separates investment and financing decisions.

- Disadvantages: Identifying and valuing all financing side effects can be complex.

Organisations may use one or more of these techniques for investment evaluation. Some use different methods for different types of projects, while others may use multiple methods for each project.

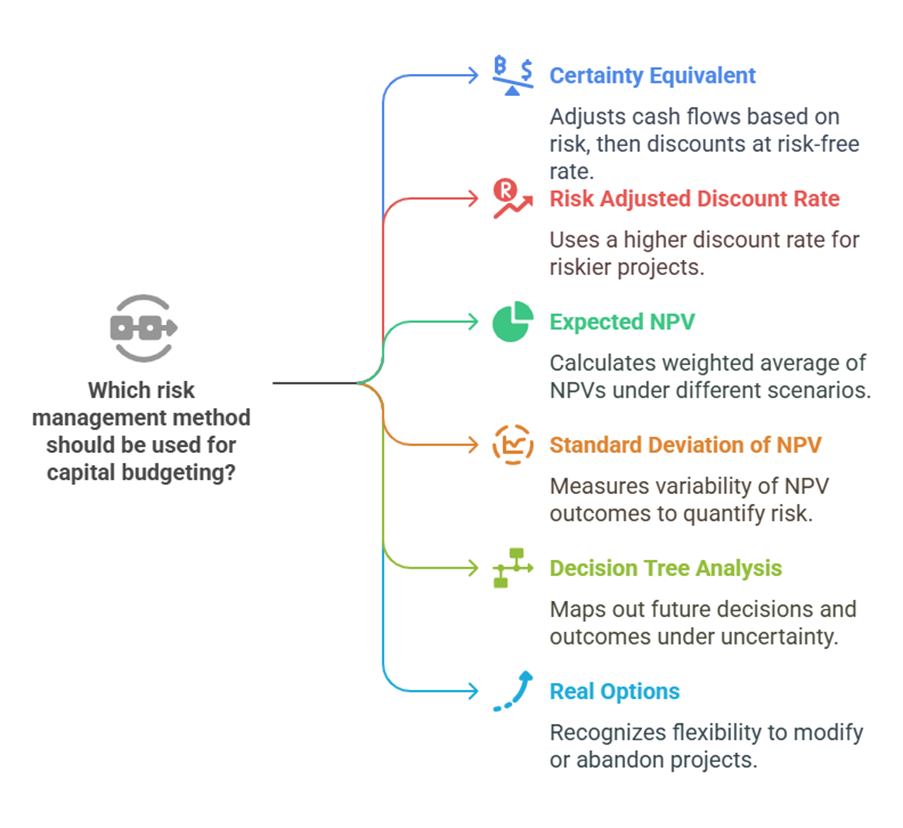

Risk in Capital Budgeting

While basic capital budgeting techniques often assume known cash flows with certainty, in practice, investment projects are exposed to various types of risk and uncertainty. Dealing with risk is a key aspect of advanced capital budgeting. Methods for incorporating risk include:

- Certainty Equivalent Approach: Adjusting expected cash flows downwards based on their perceived risk, then discounting these adjusted cash flows at the risk-free rate.

- Risk Adjusted Discount Rate: Using a higher discount rate for projects perceived as riskier.

- Expected NPV: Calculating the weighted average of possible NPVs under different scenarios, using probability estimates.

- Standard Deviation of NPV: Measuring the variability of possible NPV outcomes to quantify risk.

- Decision Tree Analysis: Mapping out possible future decisions and their potential outcomes under uncertainty.

- Options in Capital Budgeting (Real Options): Recognizing that managers have flexibility (options) to modify or abandon projects in the future based on market conditions. For example, a project with a negative initial NPV might be accepted if it provides significant future growth options.

Factors affecting capital budgeting decisions can be internal or external. Current trends in capital budgeting also consider the impact of inflation on cash flow forecasting and the effects of changes in technology and government policies.

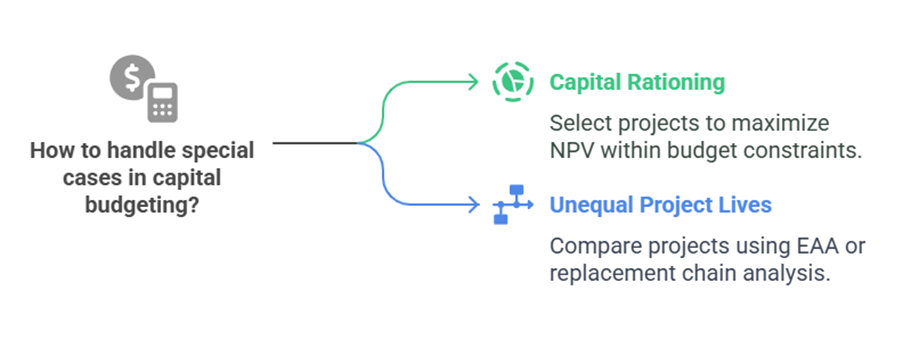

Special Cases in Capital Budgeting

- Capital Rationing

- Concept: Capital rationing occurs when a firm has more potentially acceptable investment projects (those with positive NPVs) than it has the financial resources to fund.

- Objective: The objective is to select the combination of projects (or parts of projects if divisible) that maximizes the total NPV within the given capital spending limit.

- Method: Projects acceptable under the basic criteria (like NPV > 0) are ranked. For divisible projects, ranking is often based on the Profitability Index (PI) or NPV per unit of investment, and projects are selected in descending order of rank until the capital budget is exhausted.

- Projects with Unequal Lives

- Concept: When comparing mutually exclusive projects that have different useful lives, simply comparing their NPVs can be misleading.

- Method: Techniques like the Equivalent Annual Annuity (EAA) method or replacement chain analysis are used to compare projects on a common basis over a consistent time horizon.

In summary, capital budgeting appraisal methods provide the framework for evaluating potential long-term investments. By employing techniques like NPV, IRR, and others, while considering cash flows, the time value of money, risk, and potential capital constraints, financial managers can make informed decisions that contribute to the objective of maximizing shareholder wealth.