Capital rationing is a significant situation in financial management, particularly within the realm of investment decisions or capital budgeting. It arises when a firm is faced with a constraint, either externally imposed or self-imposed, that limits its ability to obtain the necessary funds to invest in all available projects that are financially viable and have a positive Net Present Value (NPV).

Meaning and Definition

In simple terms, capital rationing refers to a situation where the amount of funds available for capital investment during a specific period is limited, despite the existence of multiple potentially profitable investment opportunities. The sources define capital rationing as a constraint on obtaining necessary funds, stemming from external or self-imposed reasons. It is the process of choosing investment proposals under financial constraints, specifically regarding a given size of a capital expenditure budget. Under capital rationing, management’s task is not just to identify profitable investment opportunities but to decide on the combination of profitable projects that yields the highest total net present value within the available funds.

Capital budgeting, of which capital rationing can be a special case, involves evaluating and selecting long-term investments that align with the objective of maximizing investor’s wealth. Investment decisions are crucial and critical business decisions due to the substantial expenditure involved, the long period for the recovery of benefits, the irreversibility of decisions, and the complexity involved. Estimating future cash flows is one of the most important tasks in capital budgeting. However, even after identifying projects with positive NPV or an Internal Rate of Return (IRR) greater than the cutoff rate, and a Profitability Index (PI) greater than 1, meaning they are financially viable and acceptable, a firm might not have enough funds to undertake all of them. This is precisely when capital rationing occurs.

Capital rationing forces a firm to make a choice among acceptable projects because its financial resources are limited. The objective in such a scenario is to select a group of investment proposals from many acceptable ones that, when taken together, maximize the total NPV, thereby maximizing the wealth of shareholders. This differs from situations without capital constraints, where all projects with a positive NPV would ideally be accepted.

Need for Capital Rationing

The need for capital rationing arises when a firm faces a situation where the total initial investment required for all projects with positive NPV (or acceptable IRR/PI) exceeds the available capital budget. As investment decisions often involve significant financial outlays, securing adequate finance is a critical aspect of financial management. When the procurement of funds is limited despite opportunities for effective utilization, capital rationing becomes necessary.

Types of Capital Rationing

The sources identify two main types of capital rationing based on the nature of the constraint:

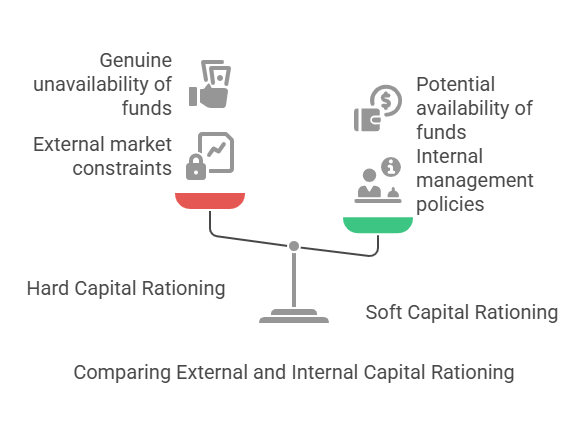

- Hard Capital Rationing (External Capital Rationing): This type occurs due to market constraints on the amount of funds available for investment during a period. The firm is unable to obtain funds from the external capital market due to external factors. External capital rationing mainly occurs on account of imperfections in capital markets. These imperfections may be caused by deficiencies in market information or by rigidities of attitude that hamper the free flow of capital. If shareholders do not have access to the capital markets, the standard NPV rule (accepting all positive NPV projects) may not work. This represents a genuine unavailability of funds from external sources like issuing equity shares, preference shares, debentures, or securing loans.

- Soft Capital Rationing (Internal Capital Rationing): This type arises when a firm fixes a maximum amount that can be invested in capital projects during a given period, such as a year. This budget ceiling is imposed internally by the management. While the firm might potentially be able to raise more funds from the market, it chooses not to, perhaps due to policy reasons, a desire to avoid increasing debt or equity beyond a certain level, management’s risk aversion, or a lack of sufficient managerial expertise to handle a larger volume of projects simultaneously. The decision to plough back earnings, for example, depends on factors like the rate of return generated versus the expected cost of equity. Internal constraints like this can lead to soft capital rationing.

A statement in one source suggests capital rationing is a situation when the government has imposed a ceiling on investment by a firm. However, the primary descriptions of external capital rationing focus on market imperfections rather than direct government mandates. Therefore, the government imposing a ceiling might be a specific instance but is not the general definition provided by the sources for capital rationing.

Objective and Decision Making under Capital Rationing

The fundamental objective under capital rationing is to maximize the total Net Present Value (NPV) from the portfolio of projects selected, given the limited capital available. This means finding the best combination of profitable projects that fit within the budget constraint.

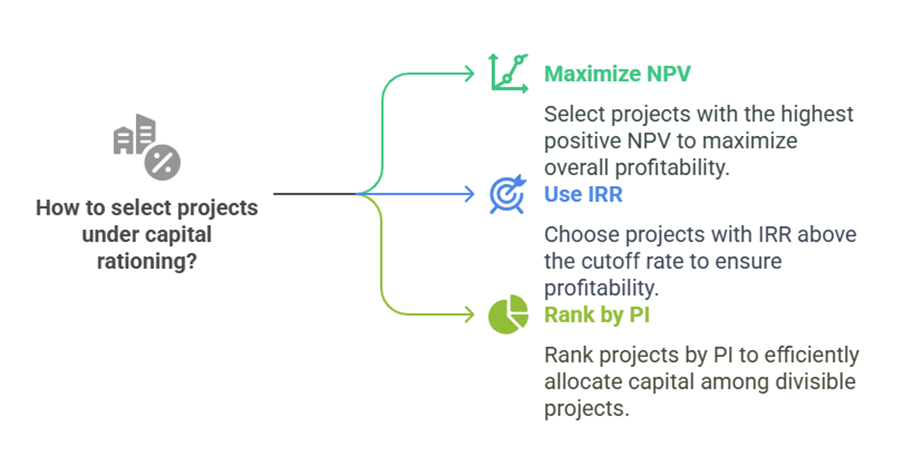

The process generally involves evaluating individual projects using capital budgeting techniques like NPV, Internal Rate of Return (IRR), and Profitability Index (PI). Projects with negative NPV or PI less than 1 are rejected outright, regardless of capital constraints. Capital rationing only concerns the selection among acceptable projects (those with positive NPV, IRR > cutoff rate, PI > 1).

To make decisions under capital rationing, projects are typically ranked based on a predetermined criterion. While IRR and NPV are key evaluation methods, the Profitability Index (PI) is particularly useful for ranking projects under capital rationing, especially if projects are divisible. The PI measures the present value of future cash flows relative to the initial investment. A PI greater than 1 indicates a positive NPV. Projects can be ranked in descending order of their PI.

Divisible vs. Non-Divisible Projects

The approach to selecting projects under capital rationing depends on whether the projects are divisible or non-divisible:

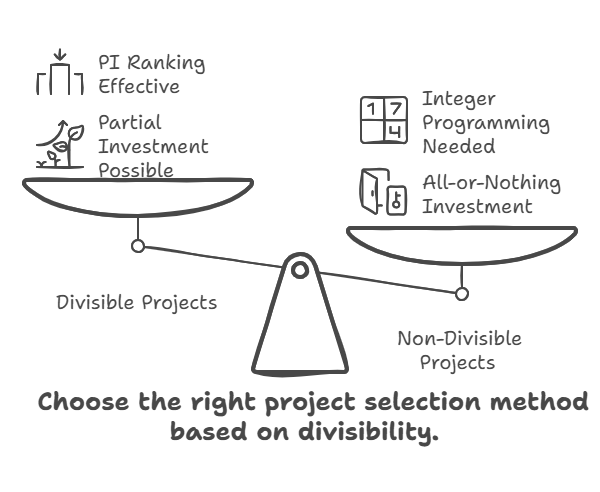

- Divisible Projects: If projects can be undertaken in parts (i.e., partial investment is possible, and returns are proportional to the investment), the PI ranking method is effective. The firm should rank the acceptable projects by their PI in descending order and invest in them starting from the highest PI project until the capital budget is exhausted. If the last selected project requires more capital than the remaining budget, only a fraction of that project can be undertaken, proportional to the remaining funds.

- Non-Divisible Projects: If projects must be accepted or rejected in their entirety (i.e., partial investment is not possible), simple PI ranking may not yield the optimal solution. Selecting projects strictly by PI might lead to a situation where the best combination of projects that fit within the budget involves skipping a higher-ranked project to take a lower-ranked one or a group of lower-ranked ones that collectively yield a higher total NPV. For non-divisible projects, the source mentions the application of Integer Programming as a technique. Integer programming is a mathematical optimization technique used to find the best combination of discrete choices (accept or reject each project) subject to constraints (the budget limit) to maximize an objective function (total NPV). This involves evaluating different combinations of projects to identify the one that maximizes the total NPV without exceeding the available funds.

Let’s consider the example provided in source to illustrate the PI ranking for divisible projects and the concept of finding the optimal combination for non-divisible projects. Projects: A, B, C, D, E, F Investments (): A=70,00,000, B=25,00,000, C=50,00,000, D=20,00,000, E=55,00,000, F=75,00,000 NPV (): A=30,00,000, B=16,00,000, C=20,00,000, D=10,00,000, E=45,00,000, F=-25,00,000

First, identify acceptable projects. Projects with positive NPV are A, B, C, D, and E. Project F has a negative NPV and is not acceptable.

Calculate the Profitability Index (PI) for the acceptable projects. PI = 1 + (NPV / Investment). PI_A = 1 + (30,00,000 / 70,00,000) ≈ 1 + 0.4286 = 1.4286 PI_B = 1 + (16,00,000 / 25,00,000) = 1 + 0.64 = 1.6400 PI_C = 1 + (20,00,000 / 50,00,000) = 1 + 0.40 = 1.4000 PI_D = 1 + (10,00,000 / 20,00,000) = 1 + 0.50 = 1.5000 PI_E = 1 + (45,00,000 / 55,00,000) ≈ 1 + 0.8182 = 1.8182

Rank the acceptable projects by PI in descending order:

- E (PI ≈ 1.8182, Investment 55,00,000, NPV 45,00,000)

- B (PI = 1.6400, Investment 25,00,000, NPV 16,00,000)

- D (PI = 1.5000, Investment 20,00,000, NPV 10,00,000)

- A (PI ≈ 1.4286, Investment 70,00,000, NPV 30,00,000)

- C (PI = 1.4000, Investment 50,00,000, NPV 20,00,000)

Now, assume a hypothetical capital budget, for instance, ` 80,00,000.

If projects are divisible: Start selecting projects based on the PI ranking until the budget is exhausted.

- Select Project E: Investment = 55,00,000. Remaining budget = 80,00,000 – 55,00,000 = 25,00,000.

- Next highest PI is Project B: Investment = 25,00,000. Remaining budget = 25,00,000 – 25,00,000 = 0. Total investment in this case is 55,00,000 (E) + 25,00,000 (B) = 80,00,000. Total NPV = NPV of E + NPV of B = 45,00,000 + 16,00,000 = 61,00,000. The firm invests the full budget and achieves a total NPV of 61,00,000.

If projects are non-divisible: Simple PI ranking might not be optimal. The firm needs to evaluate combinations of projects that fit within the ` 80,00,000 budget and select the combination that maximizes total NPV.

Let’s list combinations of acceptable projects whose total investment is less than or equal to ` 80,00,000 and calculate their total NPV:

- Project A alone: Investment 70,00,000, NPV 30,00,000.

- Project B alone: Investment 25,00,000, NPV 16,00,000.

- Project C alone: Investment 50,00,000, NPV 20,00,000.

- Project D alone: Investment 20,00,000, NPV 10,00,000.

- Project E alone: Investment 55,00,000, NPV 45,00,000.

- Combination B and D: Investment 25,00,000 + 20,00,000 = 45,00,000, NPV 16,00,000 + 10,00,000 = 26,00,000.

- Combination B and C: Investment 25,00,000 + 50,00,000 = 75,00,000, NPV 16,00,000 + 20,00,000 = 36,00,000.

- Combination B and E: Investment 25,00,000 + 55,00,000 = 80,00,000, NPV 16,00,000 + 45,00,000 = 61,00,000.

- Combination D and C: Investment 20,00,000 + 50,00,000 = 70,00,000, NPV 10,00,000 + 20,00,000 = 30,00,000.

- Combination D and E: Investment 20,00,000 + 55,00,000 = 75,00,000, NPV 10,00,000 + 45,00,000 = 55,00,000.

- Other combinations like B, D, and C (25+20+50 = 95,00,000) or B, D, and A (25+20+70 = 115,00,000) exceed the budget of 80,00,000.

Comparing the total NPVs of all feasible combinations:

- A: 30,00,000

- B: 16,00,000

- C: 20,00,000

- D: 10,00,000

- E: 45,00,000

- B+D: 26,00,000

- B+C: 36,00,000

- B+E: 61,00,000

- D+C: 30,00,000

- D+E: 55,00,000

The combination of Projects B and E yields the highest total NPV (61,00,000) within the ` 80,00,000 budget. In this specific example, the outcome for divisible and non-divisible projects with a budget of 80,00,000 is the same. However, with different project investments, NPVs, or budget constraints, simple PI ranking for non-divisible projects might lead to a suboptimal solution. Integer programming is a formal technique mentioned for solving the non-divisible capital rationing problem.

Capital rationing is a challenge that requires careful consideration of project viability and strategic selection to maximize value creation under financial constraints. It underscores the importance of not only identifying profitable projects but also managing the procurement and allocation of funds effectively.