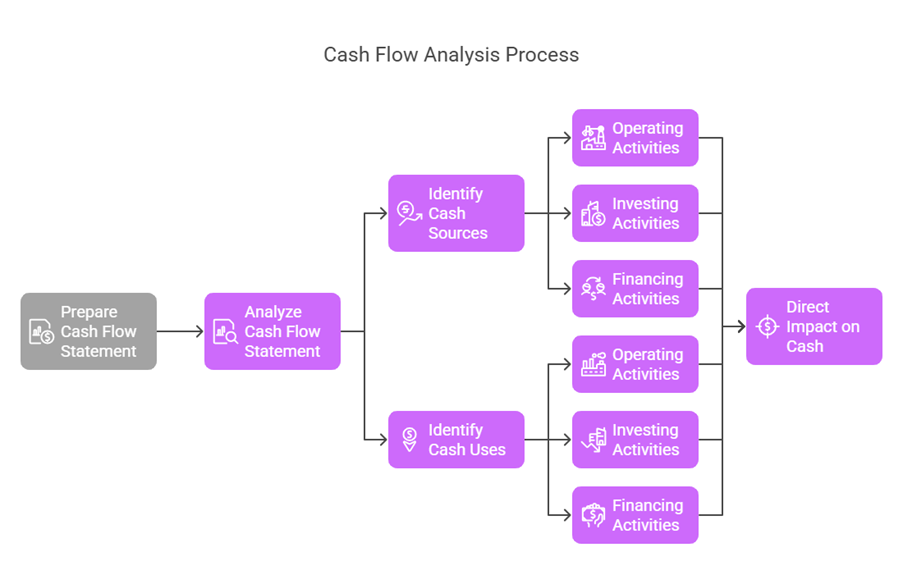

Cash Flow Analysis is a vital tool for financial analysis and planning. It involves the preparation and analysis of a Cash Flow Statement. According to Accounting Standard – 3 (Revised) and Ind AS-7, an enterprise is required to prepare a Cash Flow Statement and present it for each period alongside its financial statements.

The primary purpose of a Cash Flow Statement is to reveal the causes of changes in a business concern’s cash position between two balance sheet dates. It provides details regarding the cash generated and utilised through the entity’s operating, investing, and financing activities. This statement focuses on transactions that have a direct impact on cash.

Key Concepts in Cash Flow Analysis

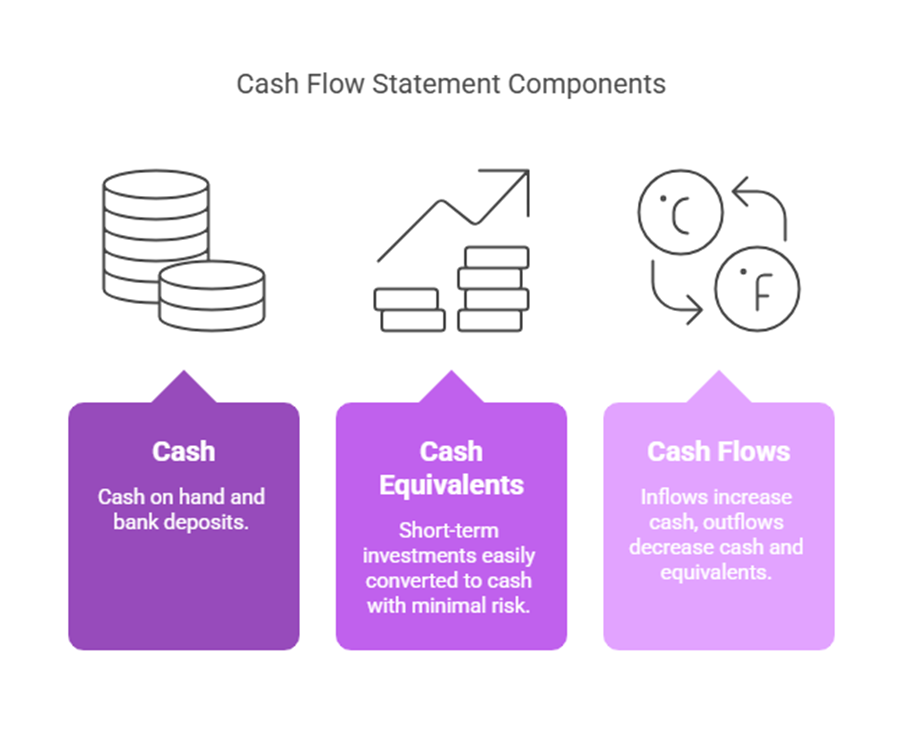

The sources define the fundamental terms used in Cash Flow Statements:

- Cash: This includes cash on hand and demand deposits with banks.

- Cash Equivalents: These are short-term, highly liquid investments that are readily convertible into cash and are subject to an insignificant risk of changes in value. An investment typically qualifies as a cash equivalent only when it has a short maturity, such as three months or less. Examples include short-term investments.

- Cash Flows: These encompass both inflows (sources) and outflows (uses) of cash and cash equivalents. An inflow increases the total cash and equivalents, while an outflow decreases it.

Classification of Cash Flows

The Cash Flow Statement reports cash flows classified by three main activities: operating, investing, and financing. This classification helps users understand the impact of these different activities on the entity’s cash position.

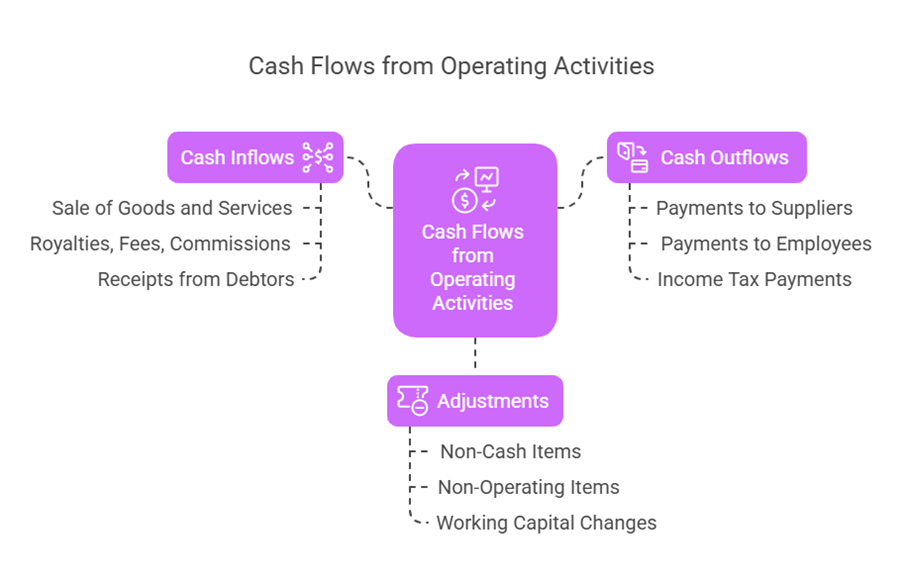

- Cash Flows from Operating Activities: These are the cash flows derived from the principal revenue-producing activities of the enterprise. They generally result from the transactions and other events that determine the entity’s net profit or loss. Examples of cash inflows from operating activities include:

- Cash receipts from the sale of goods and services.

- Cash receipts from royalties, fees, commissions, and other revenue.

- Cash receipts from debtors. Examples of cash outflows from operating activities include:

- Cash payments to suppliers for goods and services.

- Cash payments to employees and for overheads.

- Cash payments or refunds of income taxes, unless specifically identifiable with financing and investing activities.

- Cash payments relating to future contracts, forward contracts, option contracts, and swap contracts when held for dealing or trading purposes.

Calculating Cash Flow from Operating Activities: The sources show formats that often start with the net profit before tax and extraordinary items. Adjustments are then made for non-cash and non-operating items that were included in the profit or loss calculation. Items typically added back (as they reduced profit but didn’t use cash) include:

- Depreciation.

- Transfer to reserves and provisions.

- Goodwill written off.

- Preliminary expenses written off.

- Other intangible assets written off (e.g., discount or loss on issue of shares/debentures, underwriting commission).

- Loss on sale or disposal of fixed assets.

- Premium on Redemption of Debentures.

- Proposed Dividend.

- Interest on Debentures. Items typically deducted (as they increased profit but didn’t generate cash, or relate to investing/financing) would include gains on sale of assets or investment income, though specific subtractions are less detailed in the generic format provided.

After these adjustments, the result is the operating profit before working capital changes. Further adjustments are made for changes in current assets and current liabilities (excluding cash and cash equivalents).

- Increases in current assets (like debtors, stock) generally represent a use of cash (or less cash received) and are deducted.

- Decreases in current assets generally represent a source of cash (more cash received) and are added.

- Increases in current liabilities (like creditors, bills payable) generally represent a source of cash (less cash paid) and are added.

- Decreases in current liabilities generally represent a use of cash (more cash paid) and are deducted.

This leads to cash generated from operations before tax, from which income tax paid is deducted to arrive at the net cash from operating activities.

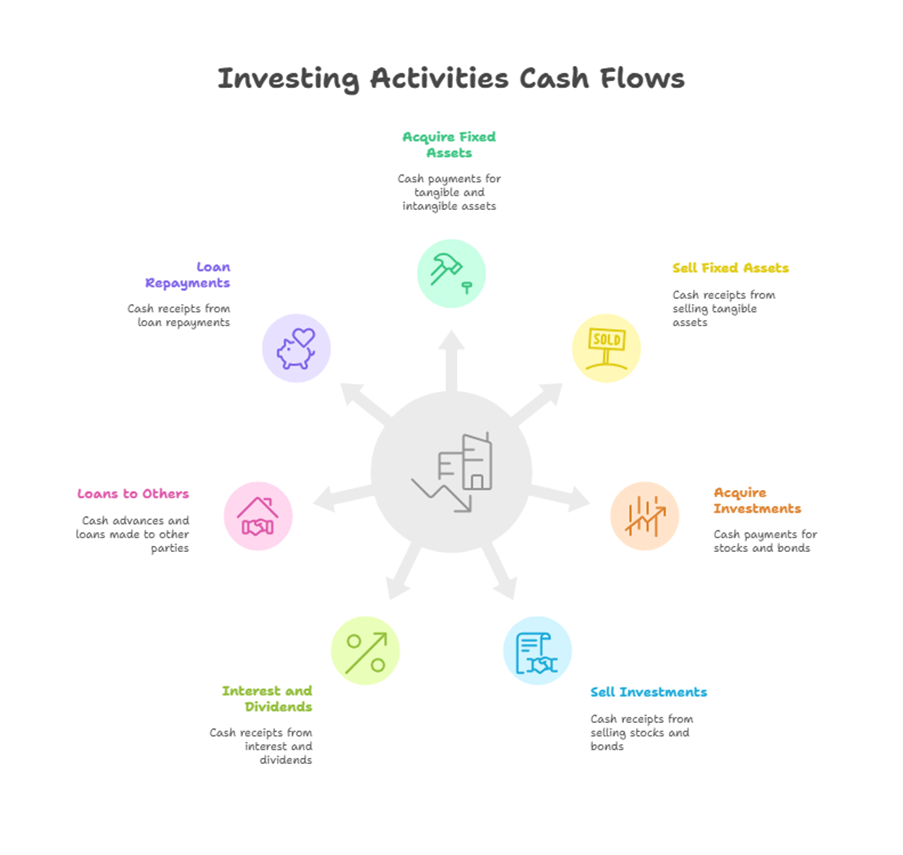

- Cash Flows from Investing Activities: These are cash flows resulting from the acquisition and disposal of long-term assets and other investments not included in cash equivalents. They represent the extent to which expenditures have been made for resources intended to generate future income and cash flows. Examples of cash flows from investing activities include:

- Cash payments to acquire fixed assets (tangible and intangible).

- Cash receipts from the sale of fixed assets.

- Cash payments to acquire investments.

- Cash receipts from the sale of investments.

- Cash receipts from interest and dividends received.

- Cash advances and loans made to other parties.

- Cash receipts from the repayment of advances and loans made to other parties.

- Cash Flows from Financing Activities: These are cash flows that result in changes in the size and composition of the equity capital and borrowings of the enterprise. Examples of cash flows from financing activities include:

- Cash proceeds from issuing shares or other similar instruments.

- Cash proceeds from issuing debentures, loans, notes, bonds, and other short- or long-term borrowings.

- Cash repayments of amounts borrowed, such as redemption of debentures, bonds, preference shares.

- Cash payments for interest paid.

- Cash payments for dividends paid.

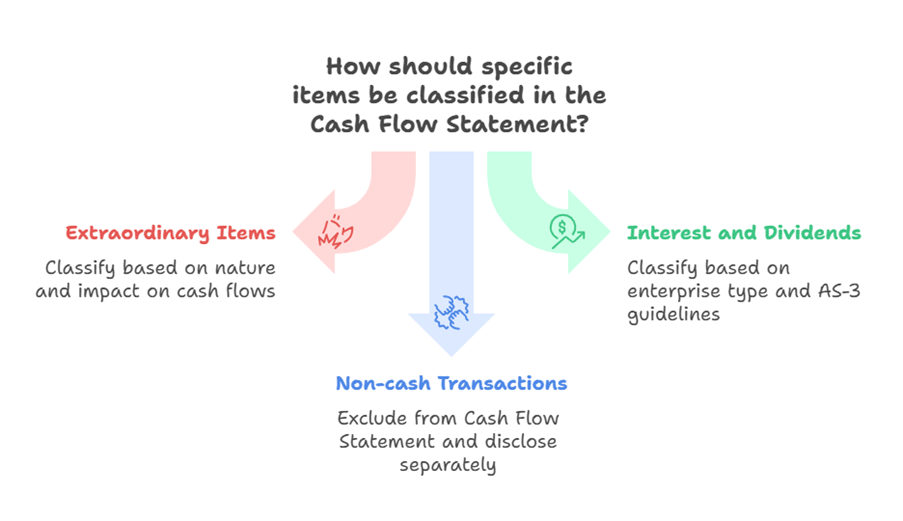

Treatment of Specific Items

- Extraordinary Items: Cash flows related to extraordinary items should be classified as operating, investing, or financing as appropriate and disclosed separately to help users understand their nature and impact on cash flows.

- Interest and Dividends: Cash flows from interest and dividends received and paid should be disclosed separately. The classification depends on the nature of the enterprise. For financial enterprises, cash flows from interest paid and received, and dividends received and paid are typically classified as cash flows from operating activities. For other enterprises, interest paid and dividends paid are generally classified as financing cash flows, while interest received and dividends received are generally classified as investing cash flows. However, AS-3 (Revised) allows interest received and paid, and dividends received to be classified as operating cash flows, and dividends paid as financing cash flows.

- Non-cash Transactions: Many investing and financing activities do not directly impact current cash flows but affect the capital and asset structure. These transactions should be excluded from the Cash Flow Statement and disclosed elsewhere in the financial statements. Examples include acquiring assets by assuming liabilities, acquiring an enterprise by issuing shares, or converting debt to equity.

Preparation of Cash Flow Statement

While AS-3 (Revised) and Ind AS-7 do not mandate a specific format, a widely used format classifies cash flows into the three activity types. The statement reconciles the beginning and ending cash and cash equivalents balances.

The cash flow from operating activities can be reported using either the direct method or the indirect method. The indirect method is illustrated in several examples, starting with net profit and adjusting for non-cash items and changes in working capital. The sources also provide examples of direct cash receipts from customers and cash paid to suppliers and employees within the operating activities section.

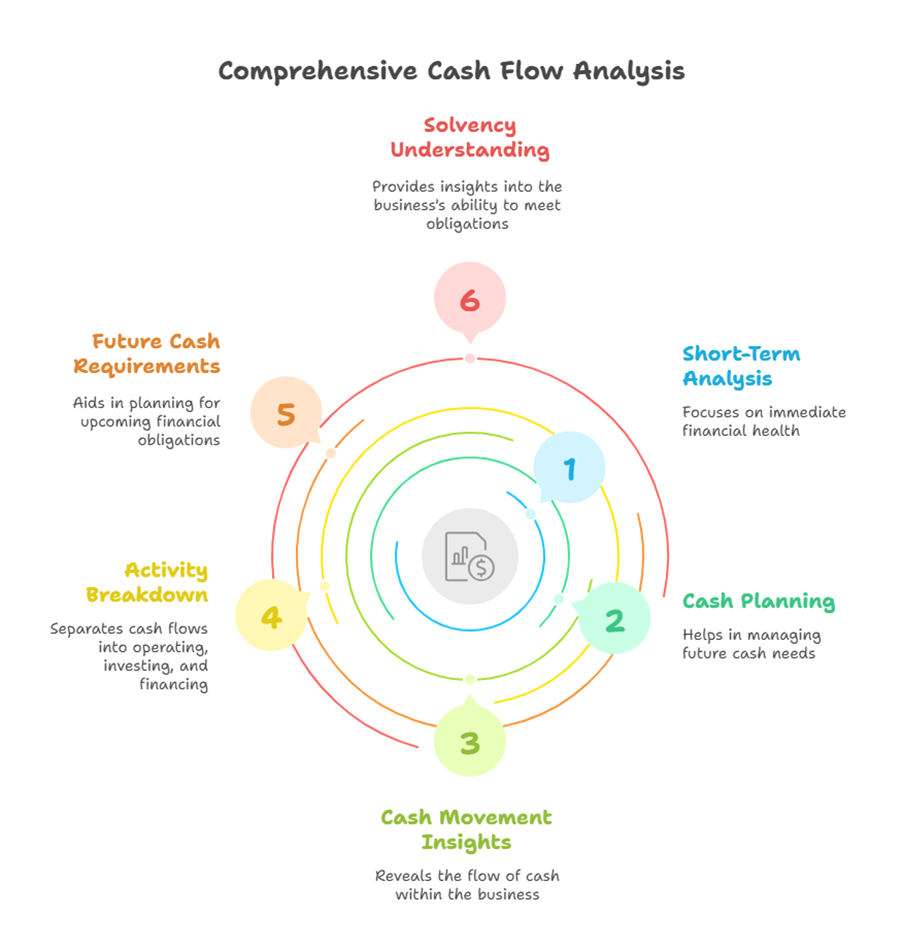

Significance and Uses of Cash Flow Analysis

Cash Flow Statement is a valuable tool for financial analysis and planning, particularly useful for short-term analysis and cash planning. Its significance includes:

- Revealing the complete story of cash movement and the reasons for changes in cash and cash equivalents.

- Providing information on operating, investing, and financing activities separately.

- Helping management plan for future cash requirements, such as for redeeming long-term liabilities or replacing fixed assets.

- A projected Cash Flow Statement helps a firm know how much cash it can generate and how much cash will be needed for various payments.

- Cash Flow Statements prepared according to AS-3 (Revised) are more suitable for comparison than funds flow statements due to the lack of standard formats for the latter.

- It helps in understanding the solvency of a business.

Limitations of Cash Flow Statement

Despite its usefulness, the Cash Flow Statement has limitations:

- It is based on cash accounting, ignoring the basic accounting concept of accrual basis.

- It reveals the movement of cash only and ignores most liquid current assets like sundry debtors and bills receivable.

- Defining the term ‘cash’ precisely can be difficult, with controversies over including near-cash items like cheques, stamps, and postal orders.

- It does not provide a complete picture of the concern’s financial position.

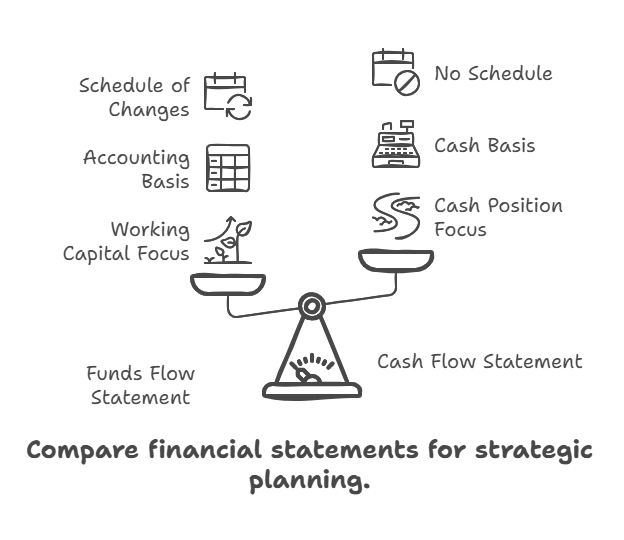

Differences between Funds Flow Statement and Cash Flow Statement

The sources highlight key differences between these two statements, both of which are tools for financial analysis:

- Focus: Funds Flow Statement reveals the change in working capital between two balance sheet dates. Cash Flow Statement reveals the changes in the cash position between two balance sheet dates.

- Basis: Funds Flow Statement is based on accounting. Cash Flow Statement is based on a cash basis of accounting.

- Schedule of Changes: A schedule of changes in working capital is prepared for a Funds Flow Statement. No such schedule is prepared for a Cash Flow Statement.

- Usefulness: Funds Flow Statement is useful for planning intermediate and long-term financing. Cash Flow Statement is more useful for short-term analysis and cash planning.

- Components: Funds Flow Statement deals with all components of working capital. Cash Flow Statement deals only with cash and cash equivalents.

- Reporting: Funds Flow Statement shows the sources and application of funds, with the difference being the net increase or decrease in working capital. Cash Flow Statement is prepared by considering inflows and outflows from operating, investing, and financing activities, with the net difference representing the net increase or decrease in cash and cash equivalents.

Cash Flow Analysis, alongside tools like Ratio Analysis and Funds Flow Analysis, is considered a fundamental tool for financial analysis and planning within the broader scope of Financial Management. It helps assess a company’s ability to generate cash, meet its obligations, and fund its investments.