Commercial Paper (CP) Definition and Nature

Commercial Paper is widely described as an unsecured short-term debt paper or instrument. It is issued in the form of a promissory note or dematerialized form. In India, due to varying state stamp duty structures and the lower duty for Usance Promissory Notes (UPN) of short-term maturity (up to one year), CP is often retained as a UPN. The stamping of a UPN is governed by the Central Act. CP essentially transforms a debt obligation of the issuer into a tradable instrument, specifically an unsecured promissory note that is negotiable and transferable by endorsement and delivery.

Origin and Purpose

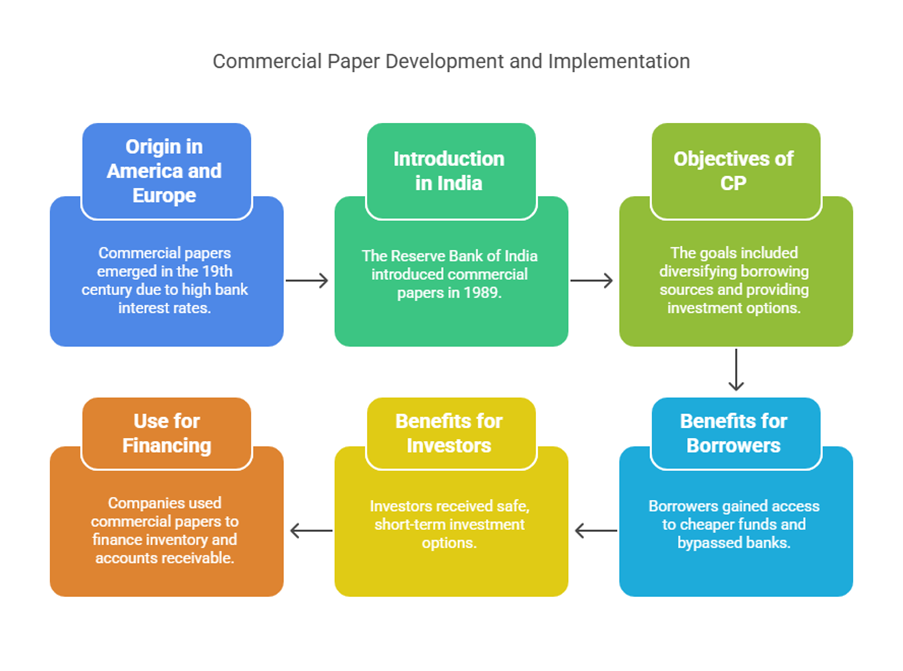

The concept of Commercial Papers originated in the financial markets of America and Europe. In the USA, they emerged in the early 19th century when commercial banks had a monopoly and charged high interest rates on loans and advances.

In India, the CP scheme was introduced by the Reserve Bank of India (RBI) in 1989, with mentions of January 1990 as the implementation date. The introduction of CP was a part of the financial sector reforms and aimed to achieve several objectives:

- Enable highly-rated corporate borrowers to diversify their sources of short-term borrowings.

- Provide an additional financial instrument to investors.

- Facilitate raising short-term funds for meeting working capital requirements directly from the market, bypassing the intermediary role of the banking system through securitization. CP partly replaces the working capital limits companies enjoy with commercial banks.

- Provide a cheap source of funds for the corporate sector.

- Offer investors a very safe investment due to the short maturity and the ability to easily predict a company’s financial situation over a few months.

- Allow companies to finance investments such as inventory and accounts receivable.

Eligible Issuers

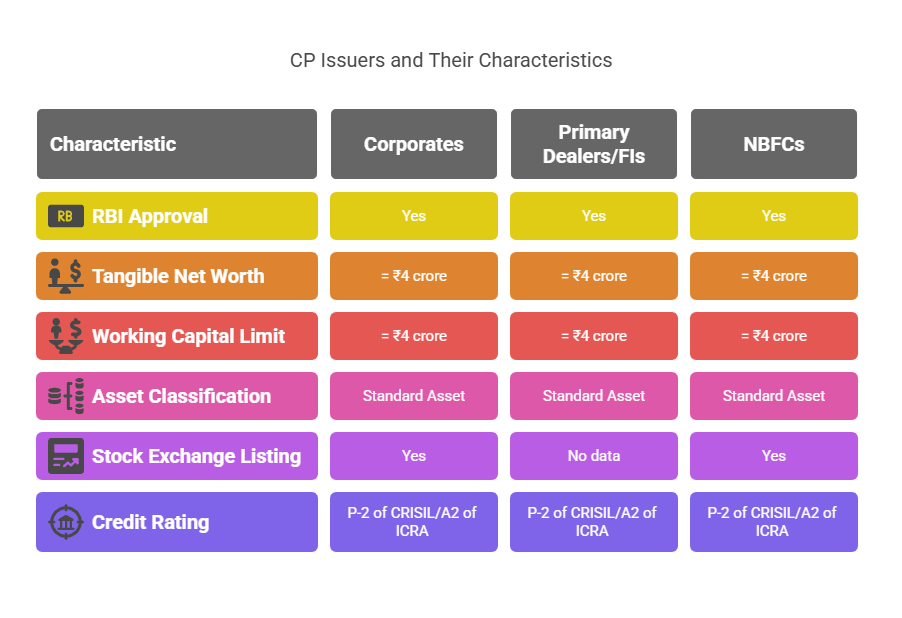

Initially, only corporates were eligible to issue CPs in India. Subsequently, Primary Dealers (PDs) and All-India Financial Institutions (FIs) permitted by the RBI were also allowed to issue Commercial Papers. Non-banking finance companies can also issue commercial paper. Commercial paper is typically issued by large, well-known, creditworthy companies or those with high credit ratings.

Specific eligibility criteria for companies issuing CP in India include guidelines from the RBI:

- The tangible net worth of the company, as per the latest audited balance sheet, must not be less than ₹4 crore. (Note: one source specifies ₹5 crore).

- The fund-based working capital limit of the company from the banking system must not be less than ₹4 crore.

- The borrowal account of the company must be classified as a Standard Asset by the financing bank/s.

- The company must be listed on a stock exchange.

- The minimum credit rating required is P-2 of CRISIL or A2 of ICRA.

All-India Financial Institutions eligible to issue CP are those specifically permitted by the RBI to raise resources within their umbrella limit, using instruments like Term Money, Term Deposits, Certificates of Deposit, Commercial Paper, and Inter-Corporate Deposits.

Denomination and Maturity Period

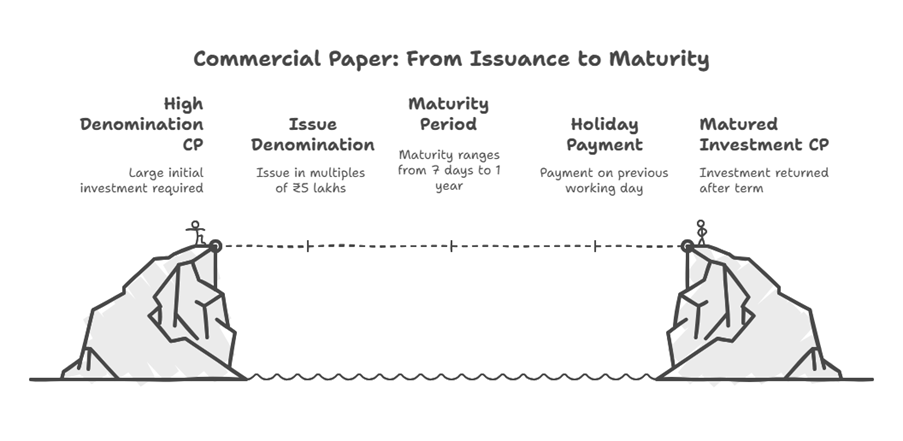

Commercial Papers in India are issued in denominations of ₹5 lakhs or multiples thereof. An older guideline mentioned issuance in multiples of ₹25 lakhs with a minimum size of ₹1 crore, but the more recent and consistently cited denomination is ₹5 lakhs.

The maturity period for Commercial Paper ranges from a minimum of 7 days to a maximum of up to one year (or 365 days) from the date of issue. Other sources specify slightly different ranges, such as 15 days to 1 year or 90 days to 360 days. The period generally varies from a few days to a few months. CP cannot be redeemed before maturity, nor can its maturity period be extended. If the maturity date falls on a holiday, payment should be made on the previous working day, as no grace period is allowed.

Issuance Process and Yield

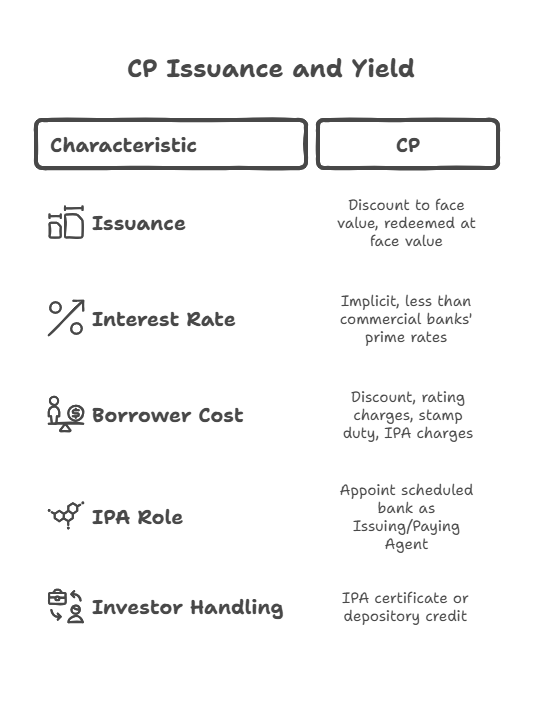

CP is typically issued at a discount to its face value and redeemed at its face value. The discount rate is determined by market forces, and the yield on CP is freely determined by the market.

The implicit interest rate is a function of the size of the discount and the period of maturity. The interest cost of CP is generally less than the prime lending rates of Commercial Banks. While a firm does not pay explicit interest, the cost to the borrower includes the discount (the difference between face value and issue price), rating charges, stamp duty, and Issuing and Paying Agent (IPA) charges. A formula is provided for calculating the interest yield: (Face value – Sale price) / Sale price * (360 days / Days of maturity).

Every issuer is required to appoint a scheduled bank to act as the Issuing and Paying Agent (IPA) for the CP issue. Investors are provided with the IPA certificate or arrangements are made to credit the CP to the investor’s account with a depository.

Transferability and Secondary Market

CP is a freely negotiable instrument, transferable by endorsement and delivery. However, Commercial Paper is often directly placed with investors who intend to hold it until maturity. Consequently, there is no well-developed secondary market for Commercial Paper.

Advantages

Several advantages of issuing Commercial Paper are highlighted:

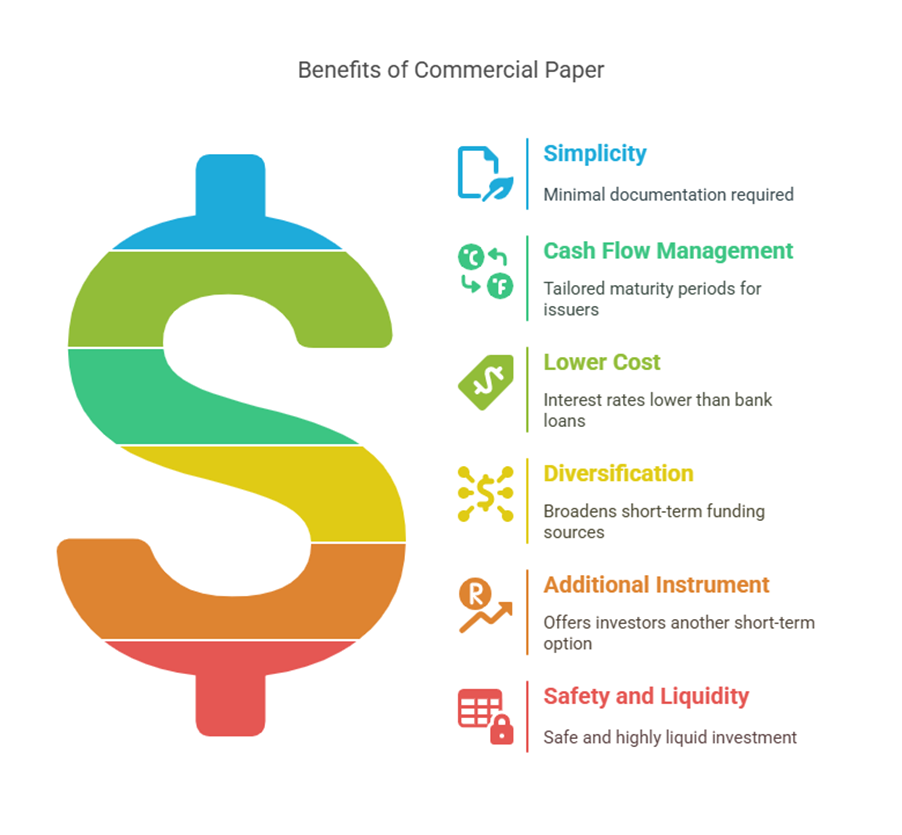

- Simplicity: The documentation involved in issuing CP is described as simple and minimum.

- Cash Flow Management: Issuers can manage their cash flow effectively by issuing CP with maturity periods that suit their needs.

- Lower Cost: The interest cost involved is typically lower than the prime lending rates from banks.

- Diversification: Enables corporate borrowers to diversify their sources of short-term funding.

- Additional Instrument: Provides investors with another option for short-term investment.

- Safety and Liquidity: Considered a very safe investment due to its short-term nature and generally possesses high liquidity.

Euro Commercial Paper (ECP)

Within the context of International Financial Management, Euro Commercial Paper is mentioned as a type of Euronote. ECPs are short-term money market securities, usually issued at a discount, with maturities of less than one year. They are unsecured promissory notes that promise to repay a fixed amount on a future date. Unlike domestic CPs in some systems, Euro Commercial Papers are not underwritten. They typically have maturities up to one year, most commonly being three-month or six-month paper. ECPs are usually designated in US Dollars.

In summary, Commercial Paper is a crucial, unsecured short-term money market instrument in India and internationally, regulated by the RBI in India. It provides creditworthy entities with a flexible, low-cost avenue for short-term financing and offers investors a relatively safe and liquid investment option, despite the limited secondary market.