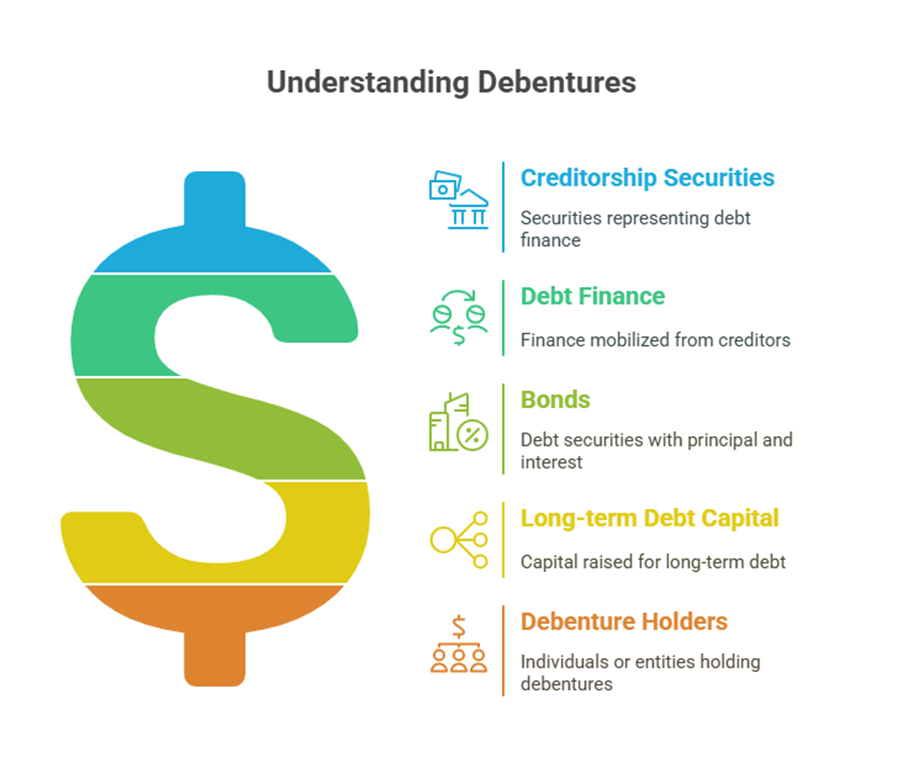

A debenture is fundamentally a document issued by a company acknowledging a debt. It is a certificate issued under the company’s seal that serves as evidence of this debt. Debentures are considered a part of Creditorship Securities, also known as debt finance, which refers to finance mobilized from creditors. The Companies Act 1956/2013 defines “debenture” to include debenture stock, bonds, and any other securities of a company, whether or not they constitute a charge on the assets of the company. Essentially, a debenture is a debt security issued by a company that promises to pay interest for the money it borrows for a specific period. Debenture holders are treated as creditors of the company.

A bond or a debenture is described as the basic debt instrument. Bonds are also debt securities issued by a company or government agency that entitle the holder to repayment of the principal sum plus interest. Debentures are instruments used for raising long-term debt capital.

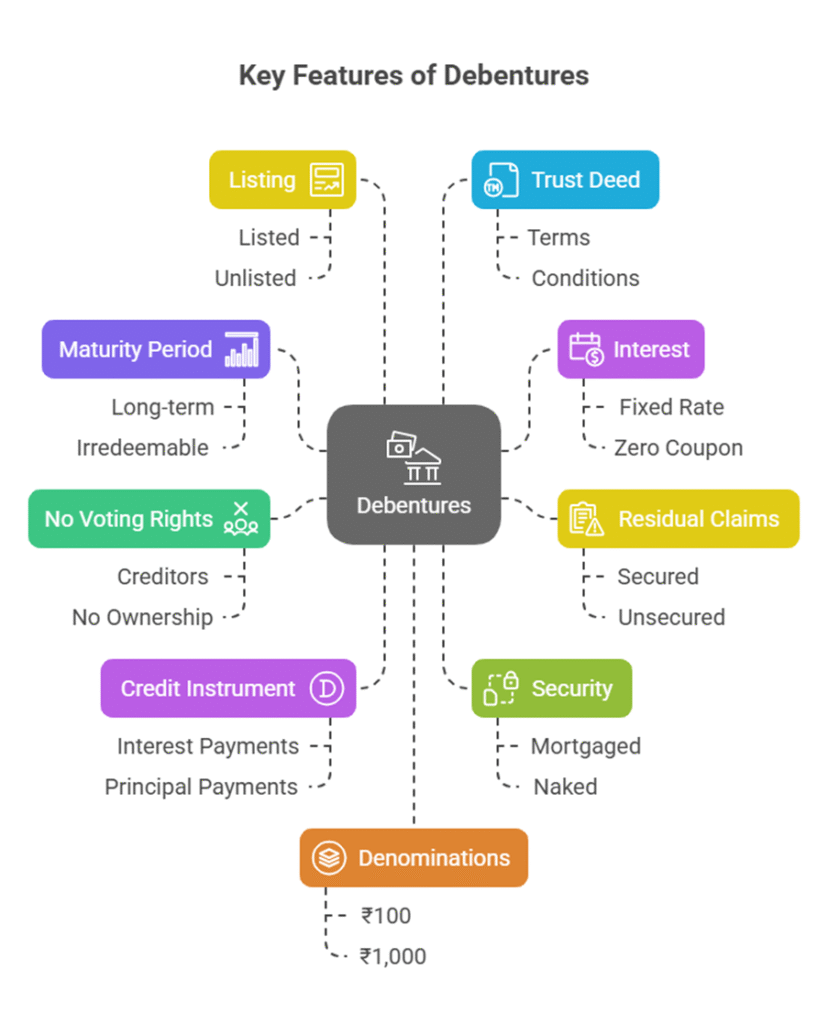

Key Features of Debentures

The sources outline several important features of debentures:

- Maturity Period: Debentures generally have a long-term fixed maturity period. This period typically ranges from 10 to 20 years, with the principal investment repayable at the end of this term. However, the maturity period can normally vary from 3 to 10 years and potentially increase for projects with high gestation periods. Some types, known as irredeemable debentures, have no defined maturity period and are taken as infinite.

- Interest: Debentures usually yield a fixed rate of interest until maturity. This interest (also known as the coupon rate) is paid periodically, typically at the end of every accounting period. A key characteristic is that interest on debenture loans must be paid even when times are hard or the company does not make profits, unlike dividend payments. Exceptions include Zero Coupon Bonds and Zero Interest Bonds/Debentures, which do not bear a fixed interest rate.

- Residual Claims: Debenture holders have a priority of claim in the income and assets of the company over equity and preference shareholders. This priority is significant, especially in the event of winding up. Debenture holders may have either a specific charge on assets (treated as secured creditors) or a floating charge (treated as unsecured creditors).

- No Voting Rights: As debenture holders are creditors and not owners, they do not have voting rights in the company. They do not have control over the business’s performance.

- Credit Instrument: A debenture holder is a creditor entitled to receive interest and principal payments and enjoys other rights.

- Security: Debentures may or may not be secured. They can be secured (mortgaged) against assets or unsecured (naked).

- Listing: Debentures may or may not be listed on the stock exchange.

- Trust Deed: Normally, debentures are issued based on a debenture trust deed that outlines the terms and conditions.

- Denominations: Debentures are typically issued in various denominations, such as from ₹100 to ₹1,000, and carry different interest rates.

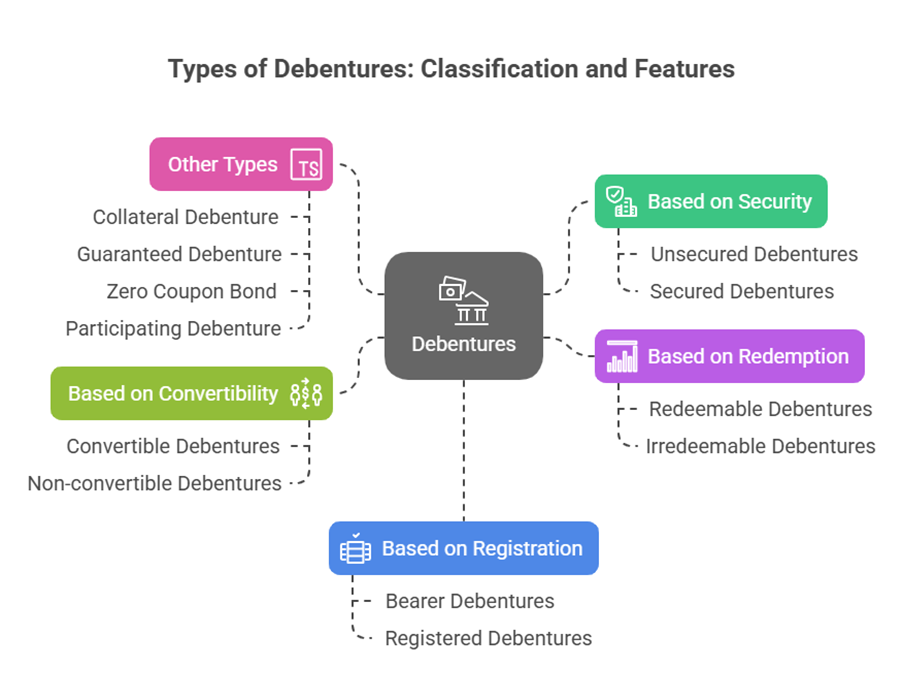

Types of Debentures

Debentures can be classified based on various criteria:

- Based on Security:

- Unsecured/Naked Debentures: These debentures are not given any security on the company’s assets. They are treated as unsecured creditors at the time of winding up.

- Secured Debentures: These are given security on the assets of the company. They are also called mortgaged debentures because they are issued against a mortgage of the company’s assets. Secured debenture holders with a specific charge are treated as secured creditors. This category includes First Debentures (those with a first claim on assets charged) and Second Mortgage Debentures (those charged after the claim of first-mortgage debentures).

- Based on Redemption:

- Redeemable Debentures: These debentures are repaid on the expiry of a certain period. The interest is paid periodically, and the initial investment is returned after the fixed maturity period. Repayment can be one time or in instalments.

- Irredeemable/Perpetual Debentures: These debentures cannot be redeemed during the lifetime of the business concern. They are repayable on the winding up of the company or on the expiry of a long time. For calculating the cost of capital, their maturity period is considered infinite.

- Based on Convertibility:

- Convertible Debentures: Holders have the option to convert them wholly or partly into shares. This conversion is usually into equity shares. Convertible debentures can be Fully Convertible Debentures (FCD) or Partly Convertible Debentures (PCD). Interest rates on Fully Convertible Debentures are generally lower than on non-convertible debentures because they offer the attractive feature of conversion into shares later.

- Non-convertible Debentures (NCD): These debentures do not have a conversion feature and are repayable only on maturity.

- Fully Convertible Debentures: Such debentures are entirely converted into equity shares according to the terms of issue (price and time of conversion).

- Partly Convertible Debentures: These possess features of both convertible and non-convertible debentures, giving investors both options in one instrument.

- Compulsory Convertible Debenture (CCD): A type of bond that must be converted into stock by a specified date. It is classified as a hybrid security.

- Optionally Convertible Debentures (OCD): These include the option for the investor to convert them into equity at a price decided by the issuer or agreed upon at issue.

- Foreign Currency Convertible Bond (FCCB): A bond that comes at a very low interest rate and can be converted into Depository Receipts or local shares after a minimum lock-in period. The issuer benefits from obtaining foreign currency at a low cost.

- Based on Registration:

- Bearer Debentures: These are transferable like negotiable instruments by delivery. Interest is paid to the bearer of the coupon attached.

- Registered Debentures: Interest is payable only to the person registered as the debenture holder. They are transferable through a transfer deed.

- Other Types:

- Collateral Debenture

- Guaranteed Debenture: An obligation guaranteed by another entity.

- Zero Coupon Bond (ZCB): These debentures (or bonds) do not bear a fixed interest (coupon) rate. They are issued at a discount and redeemed at face value or a premium.

- Zero Interest Bond/Debenture: Similar to ZCB, these do not carry interest. Zero Interest Fully Convertible Debentures are fully convertible and automatically converted after a specified period. They are beneficial to the company as no interest is paid.

- Participating Debenture: A hybrid security with varying interest charges depending on the stage of operation (no interest in start-up, low rate up to a certain level, then a high rate).

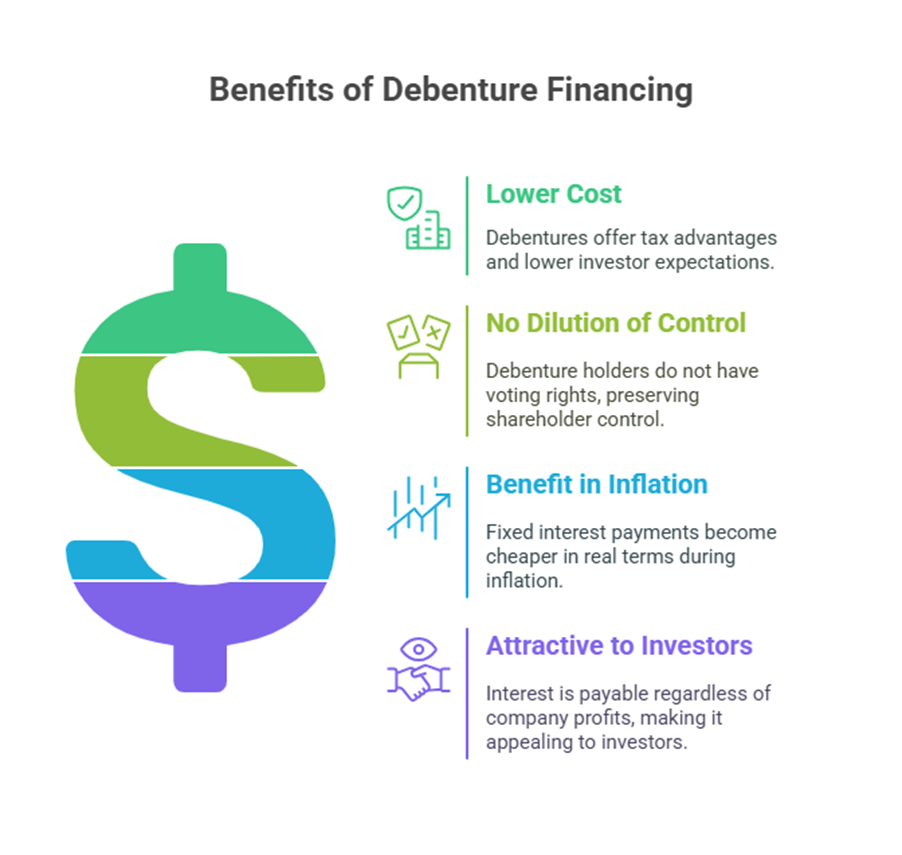

Advantages of Debenture Financing

Raising finance through debentures offers several advantages:

- Lower Cost: The cost of debentures is significantly lower than that of preference or equity capital. This is largely due to the tax advantage: the interest paid on debentures is deductible as an expense before calculating tax, unlike dividends which are paid from taxed profits. Additionally, investors may accept a lower return because debenture investment is perceived as safer than equity or preferred investment.

- No Dilution of Control: Issuing debentures does not result in the dilution of control for existing shareholders, as debenture holders do not have voting rights.

- Benefit in Inflation: Debenture issues are advantageous during periods of rising prices. The fixed monetary outflow for interest payments decreases in real terms as the price level increases. The company only has to pay a fixed rate of interest regardless of inflation.

- Attractive to Investors: From the investors’ perspective, debentures are more attractive than preference shares because interest is payable regardless of whether the company makes profits.

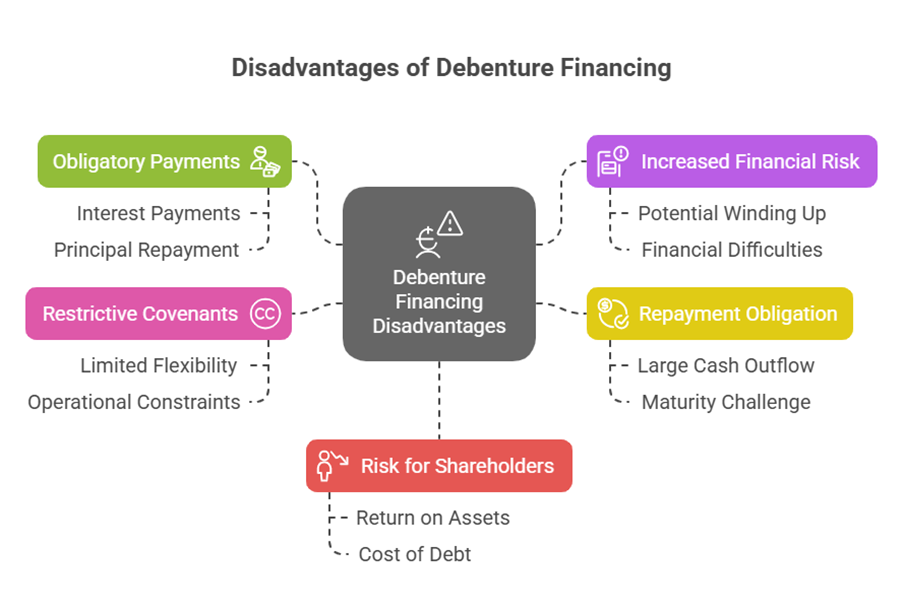

Disadvantages of Debenture Financing

Despite the advantages, debenture financing has drawbacks:

- Obligatory Payments: Debenture interest and the repayment of the principal amount are obligatory payments. This means the company is legally required to make these payments, even when facing financial difficulties or making no profits.

- Increased Financial Risk: The obligatory nature of debenture payments enhances the financial risk associated with the firm. Failure to make these payments can lead to serious consequences for the company, including potential winding up.

- Repayment Obligation: Debentures have to be repaid according to the agreed terms. The need to pay a large amount of cash outflow at maturity can be a challenge.

- Restrictive Covenants: Debenture issues may come with protective covenants that are restrictive for the company.

- Risk for Shareholders: If the return generated on assets is less than the cost of debt, it can increase the risk for shareholders.

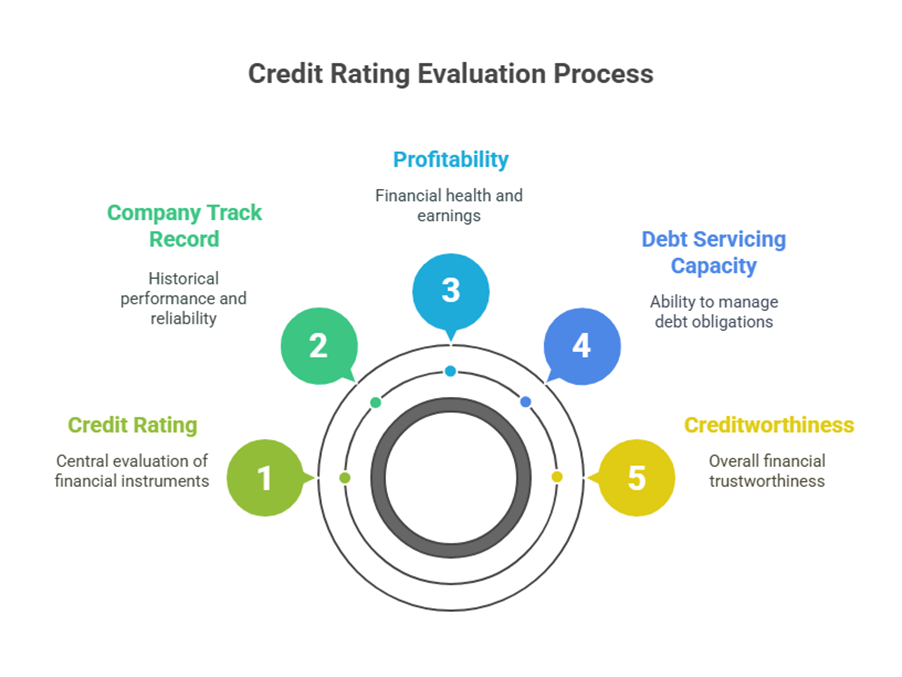

Credit Rating

Public issues of debentures and private placements to mutual funds typically require a credit rating from a credit rating agency, such as CRISIL (Credit Rating and Information Services of India Ltd.). This rating is assigned after evaluating factors including the company’s track record, profitability, debt servicing capacity, creditworthiness, and the perceived risk of lending. Credit rating agencies also rate other debt instruments like Commercial Paper and Bank Loan Ratings.

In summary, debentures are crucial long-term debt instruments used by companies to raise finance. They represent an acknowledgement of debt and come with fixed interest payments and principal repayment obligations, offering priority claims to holders over shareholders but without voting rights. While they provide cost advantages and avoid equity dilution, the mandatory nature of their payments introduces significant financial risk for the issuing company. Their features and types vary based on security, redemption terms, and convertibility options.