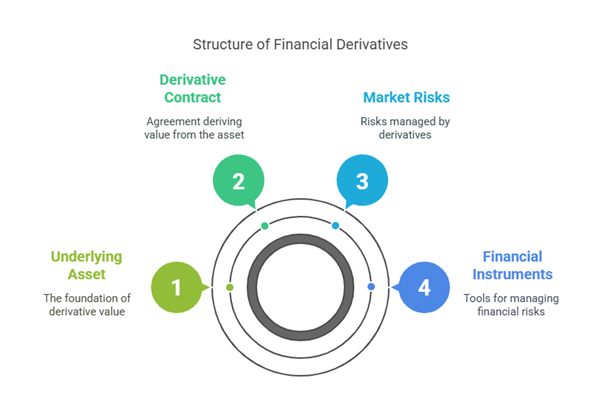

A derivative is a financial contract that derives its value from an underlying asset. It is a product whose value is to be derived from the value of one or more basic variables called bases. These underlying assets can be stock, currencies, commodities, and more. Derivatives are a mechanism to hedge market, interest rate, and exchange rate risks. They are financial instruments whose value depends, or derives from, one or more underlying financial assets. In this sense, a derivative offers a return based on the return of some other underlying instrument. In financial literature, the term ‘derivative’ refers to a contract which has no independent value but whose value is entirely derived from the value of the underlying asset. The underlying asset can be securities, commodities, bullion, currency, livestock or anything else. These are essentially financial products. A derivatives transaction is a bilateral contract or payment exchange agreement whose value depends on – derives from – the value of an underlying asset, reference rate or index.

Purpose and Functions

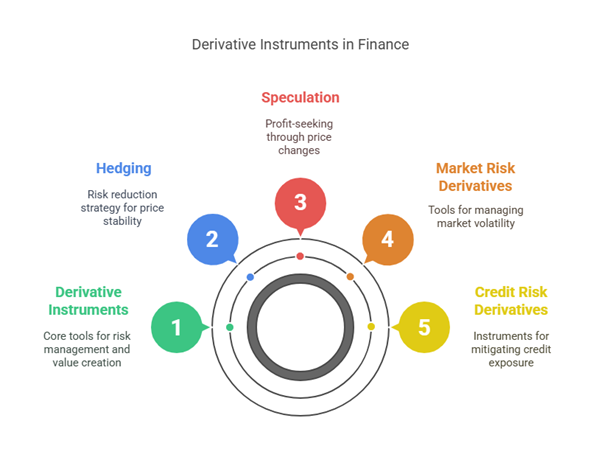

Investors primarily use derivative instruments for two objectives: hedging and speculating. Hedging attempts to reduce the amount of risk or volatility associated with a security’s price, while speculation tries to make a profit from a security’s price change. Speculators are seen as risk lovers, whereas hedging is risk averse. While derivatives can be used for hedging purposes, simultaneously they can also be used for speculation. Derivatives are powerful tools that mitigate risk and build value, helping companies develop a risk mitigation strategy. Financial derivatives can be used to hedge market risk. Credit derivatives emerged to mitigate credit risk. Interest rate derivatives are valuable tools in managing risks and are often used as hedges by institutional investors, banks, companies, and individuals to protect against changes in market interest rates, though they can also be used to increase or refine the holder’s risk profile or to speculate on rate moves.

The derivatives market performs several economic functions.

Underlying Assets

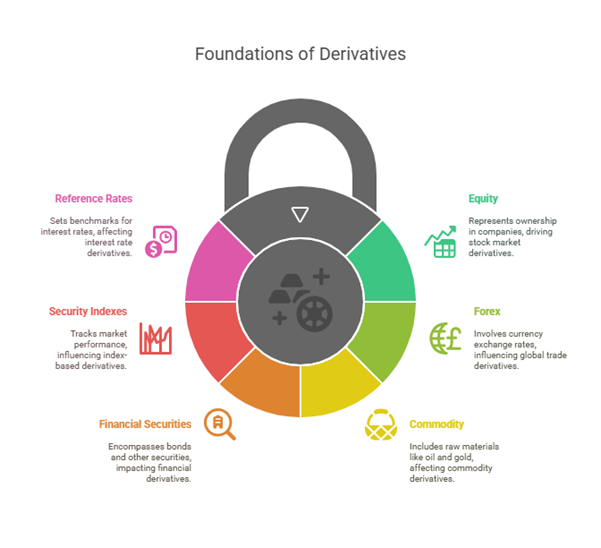

The underlying assets or bases for derivatives can be Equity, Forex, and Commodity. The underlying assets include financial securities, security indexes, reference rates, and some combination of them. They can also be tangible or intangible assets like an index or rates. Today, derivatives transactions cover a broad range of underlying assets including interest rates, exchange rates, commodities, equities, and other indices. In addition to agricultural commodities, there are futures for financial instruments and intangibles such as currencies, bonds and stock market indexes.

Types of Derivatives

Derivatives are broadly classified into two categories: Financial Derivatives and Commodity Derivatives.

The sources discuss several specific types of derivative products:

- Forward Contract: The simplest form of derivatives is the forward contract. It is a customized contract between two entities, where settlement takes place on a specific date in the future at today’s pre-agreed price. It obliges one party to buy, and the other to sell, a specified quantity of a nominated underlying financial instrument at a specific price, on a specified date in the future. Forwards are very popular in the foreign exchange market. Examples include foreign exchange forwards and forward rate agreements (FRAs).

- Futures Contract: A futures contract is an agreement between two parties to buy or sell an asset at a certain time in the future at a certain price. Futures contracts are special types of forward contracts as they are standardized exchange-traded contracts. Unlike forward contracts, the counterparty to a futures contract is the clearing corporation on the appropriate exchange. There are markets for a multitude of underlying assets for futures, including traditional agricultural or physical commodities, currencies, bonds, and stock market indexes. Hedging can be done using futures.

- Options: An option may be understood as a privilege, sold by one party to another, that gives the buyer the right, but not the obligation, to buy (call) or sell (put) any underlying asset at an agreed-upon price (the “strike price”) within a certain period or on a specific date, regardless of changes in the underlying’s market price during that period. Various kinds of stock options include put and call options, which can be purchased for speculation or hedging. A put gives the holder the option to sell shares at a fixed price even if the market price declines. A call gives the holder the option to buy shares at a fixed price even if the market price rises. Options generally have lives of up to one year.

- Swaps: Swaps are private agreements between two parties to exchange cash flows in the future according to a prearranged formula. They can be regarded as portfolios of forward contracts. Swaps generally are traded OTC through swap dealers.

- Credit Derivatives: Credit Derivatives is a summation of two terms, Credit + Derivatives. As derivatives imply value deriving from an underlying, and this underlying can be anything like stock, share, currency, interest, etc., credit derivatives emerged to mitigate credit risk. A credit derivative is a contract whose value depends on the creditworthiness or a credit event experienced by the entity referenced in the contract. Credit derivatives include credit default swaps, collateralized debt obligations, total return swaps, credit default swap options, and credit spread forwards. A CDS in which the buyer does not own the underlying debt is referred to as a naked credit default swap.

- Interest Rate Derivatives (IRD): An IRD is a financial derivative contract whose value is derived from one or more interest rates, prices of interest rate instruments, or interest rate indices. They are often used as hedges to protect against changes in market interest rates. In India, popular interest rate derivatives include Interest Rate Futures or Interest Rate Options. An interest rate cap is a type of interest rate derivative where the buyer receives payments when the interest rate exceeds the agreed strike price. An interest rate collar is an instrument that combines both a cap and a floor.

- Foreign Exchange Derivatives: A foreign currency derivative is a financial derivative whose payoff depends on the foreign exchange rates of two (or more) currencies. These instruments are commonly used for hedging foreign exchange risk or for currency speculation and arbitrage. Specific types include foreign currency forward contracts, foreign currency futures, foreign currency swaps, currency options, and foreign exchange binary options. Transaction risk can also be hedged using these products. A “Forward Importer” product consists of an FX Transaction where the Counterparty will buy a notional amount of USD against INR at the forward rate under predefined conditions, helping protect against appreciation in USD against INR.

- Commodity Derivatives: These are derivatives where the underlying is a commodity. Sources mention futures for agricultural commodities.

- Other Types: The sources also mention Complex Derivatives built from two or more other derivatives, such as Warrants (longer-dated options, generally traded over-the-counter) and LEAPS (Long-term Equity Anticipation Securities, options with maturity up to three years). Other specific option types mentioned include Spread Options (payoff depends on difference between two underlying prices), Look back options (holder chooses the most favourable strike price on maturity based on historical prices), and various option strategies like Straddle, Strangle, Strap, Strip.

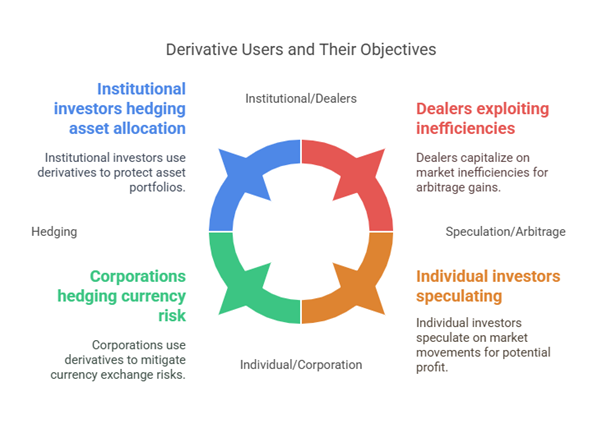

Users of Derivatives

The main users of Derivatives are:

- Corporations: To hedge currency risk and inventory risk.

- Individual Investors: For speculation, hedging, and yield enhancement.

- Institutional Investor: For hedging asset allocation, yield enhancement, and to avail arbitrage opportunities.

- Dealers: For hedging position taking, exploiting inefficiencies, and earning dealer spreads.

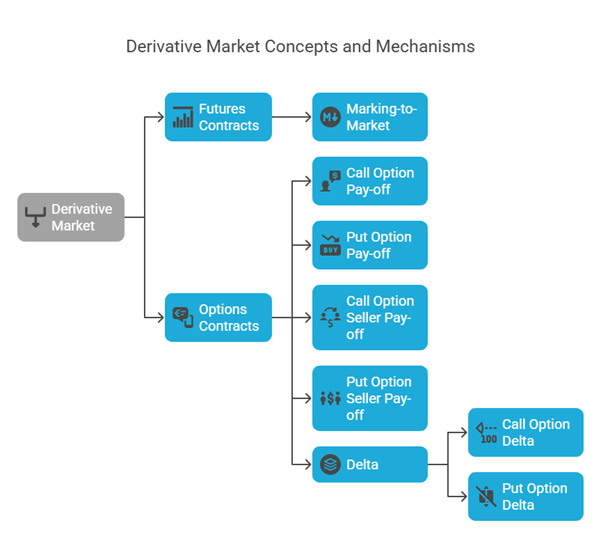

Mechanism and Concepts

In the derivative market, contracts based on tangible or intangibles assets like index or rates are traded, whereas in the cash market, tangible assets are traded.

One concept mentioned in the context of futures contracts is marking-to-market. This is where the margin accounts, also called the equity of the buyer and the seller, get adjusted at the end of the day in keeping with the price movement, and the futures contract gets replaced with a new one at the price used for adjustment. Each future contract is rolled over to the next day at a new price.

For options, the sources discuss pay-offs and “Greeks”. For a call option, the pay-off for the buyer is calculated as Max [0, Spot Price – Exercise Price] minus the premium. The pay-off for a put option buyer is Max [0, Exercise Price – Spot Price] minus the premium. The pay-off for a call seller is the mirror image of the long call. The pay-off for a short put is the mirror image of the long put.

Delta (Δ) is discussed as part of option valuation. It represents the composition of the implied risk-less hedge portfolio at the valuation date. Delta of a Call Option is always positive, while Delta of a Put Option is always negative, reflecting the inverse relationship between the Put option price and the underlying stock price. The Put Delta equals (Call Delta – 1). Delta is calculated as the change in Option Price divided by the change in Stock Price.

Risks and Mishaps

While Derivatives can be used for hedging, they can also be used for speculation. Due to this attribute, legendary investor Warren Buffet believes that derivatives are financial weapons of mass destruction. The sources mention that derivatives have proven very fatal for various organizations and even brought them to their knees, highlighting the potential for derivative mishaps.

Derivatives in India

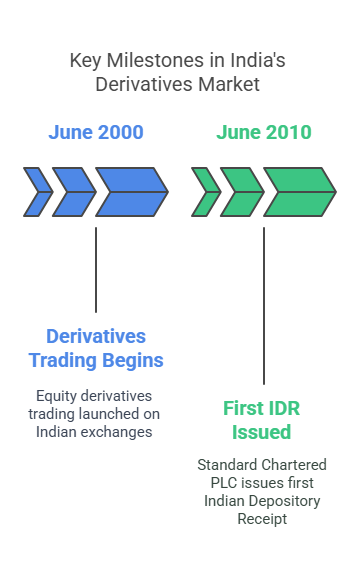

Derivatives trading in equities started in India in June 2000. At present, there are four equity derivative products traded in India: Stock Futures, Stock Options, Index Futures, and Index Options. Derivative trading is permitted on two stock exchanges in India: NSE and BSE. Currently, the derivatives market turnover is more than the cash market turnover in India. Popular interest rate derivatives in India include Interest Rate Futures or Interest Rate Options. Standard Chartered PLC was the first company that issued Indian Depository Receipt (IDR) in the Indian securities market in June 2010. While an IDR is not a derivative, it is a financial instrument related to allowing foreign companies access to the Indian market, conceptually similar to how some derivatives provide exposure to underlying foreign assets.