Factoring is fundamentally a financial service involving the conversion of credit bills into cash. It refers to the outright sale of accounts receivable to a factor or a financial agency. A factor is a firm that acquires the receivables of other firms, acting as a financial intermediary. This service is also known as “Invoice Agent” or the purchase and discount of all “receivables”. Factoring can be seen as a method of financing whereby a firm sells its trade debts at a discount to a financial institution. It is a continuous arrangement between a financial institution, called the factor, and a firm, called the client, which sells goods and services to trade customers on credit. Factoring provides resources to finance receivables and facilitates their collection. It is an alternative to the in-house management of receivables.

Factoring involves the factor purchasing the client’s trade debts, including accounts receivables, and assuming the task of collecting these receivables and handling the associated paperwork. The factor lays down the conditions of sale in a factoring agreement. The factor collects the dues of their client for a certain fee. This fee is usually expressed as a percentage of the total value of the receivables factored.

The modus operandi of a factoring scheme generally involves the seller raising a bill on the customer and issuing a notification that the invoice is assigned to the factor and payment must be made to them. Copies of the invoice are sent to the factor. The client hands over the invoices to the factor along with supporting documents like delivery challans or R/R or L/R copies. The factor may provide a prepayment of up to a maximum of 80% of the total invoice value. The factor undertakes the follow-up procedure with customers for the realization of payments. The balance payment is made to the client upon the realization of the dues. The seller is kept informed through monthly statements of account sent by the factor.

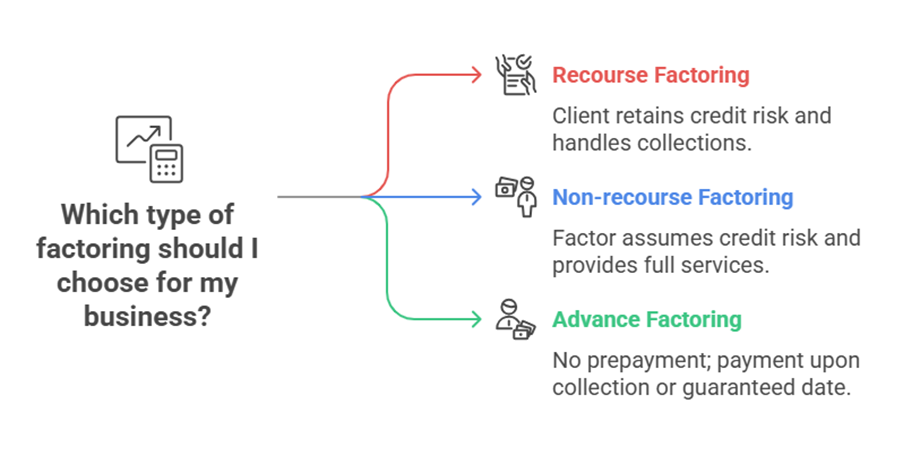

There are basic types of factoring:

- Recourse Factoring or Pure Factoring: Under this type, the factor does not assume the credit risk. If debtors fail to repay their dues on time or if debts are outstanding beyond a fixed period (e.g., 60-90 days), such debts are automatically assigned back to the client. The client then takes up the collection work for the overdue account themselves, although they can pay extra charges for the factor to continue. The seller/client bears any loss arising from irrecoverable debts.

- Non-recourse Factoring or Full-Service Factoring: This is where the factor assumes the credit risk. The factor purchases the trade debt, becoming a holder for value. If debtors fail to repay, the entire responsibility falls on the factor’s shoulders, and they cannot pass this responsibility back to the client. The factor provides all services including finance, administering the sales ledger, collecting debts at their risk, and rendering consultancy services. The client gets full protection and all service components. Factoring is usually done on a ‘non-recourse’ basis, although it can be with or without recourse.

- Advance Factoring or Maturity Factoring: In this type, no advance or prepayment is made by the factor. Payment is made to the client either on a guaranteed payment date or on the actual date of collection from the customer.

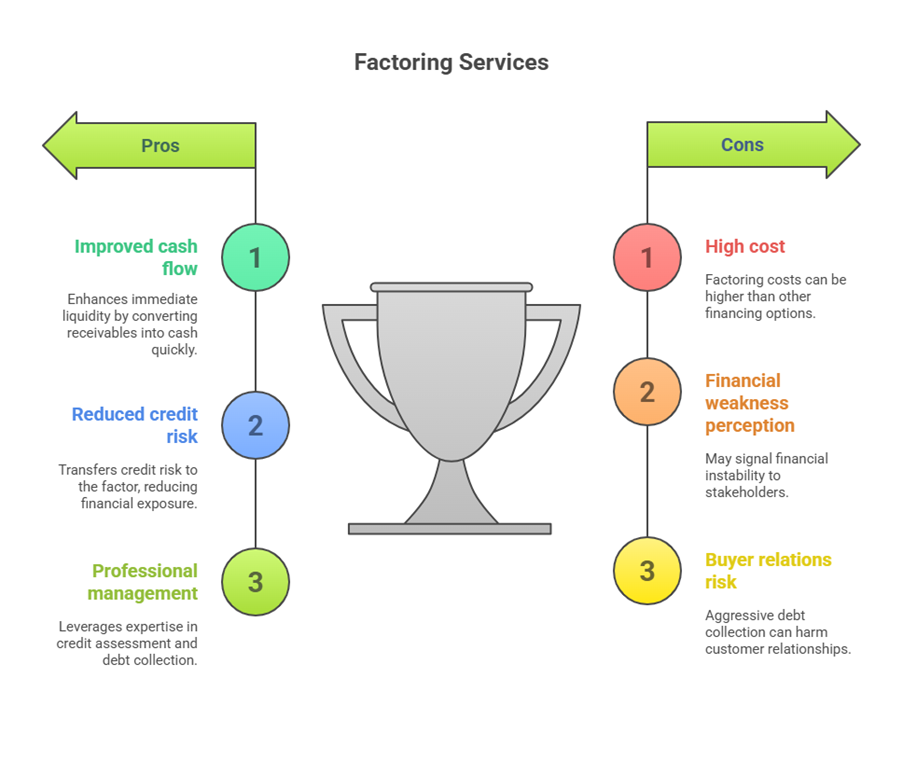

Factoring services are becoming popular worldwide due to the various services offered. Advantages and Benefits of factoring include:

- Conversion of accounts receivable into cash, improving the company’s liquidity. This replaces balance-sheet items like book credits with cash.

- Transfer of the risk of credit, risk of credit worthiness of the debtor, and other incidental risks to the factor. In non-recourse factoring, the whole credit risk is absorbed by the factor.

- Reduction in workload for the firm by transferring tasks like credit assessment, debt collection, and management of the sales ledger to the factor.

- Avoidance of bad debt losses (in non-recourse factoring).

- Saving costs associated with maintaining accounts receivable, such as bookkeeping, collections, and credit verifications. These can be avoidable costs like telephonic/fax bills and staff salaries.

- Potential for increased solvency.

- Possibility of interest savings due to a reduction in the average collection period.

- Consultancy services may be provided by the factor.

- Factoring can sometimes be performed on a non-notification basis, meaning customers might not be aware their accounts have been sold.

- Comparison between the costs saved and the fee paid to the factor often shows that utilizing factoring can be fruitful.

Despite the benefits, factoring also has limitations or drawbacks:

- The cost of factoring is often high compared to other sources of short-term finance. The discount rate charged by the factor includes compensation for the loss of interest, the risk of credit, and the risk of loss of both principal and interest on the amount involved.

- Using factoring services can create a perception of financial weakness about the firm availing the service.

- If the factor takes a tough stance against a defaulting buyer, it could have an adverse impact on the borrower’s future sales.

In India, a study group under the chairmanship of C.S. Kalyana Sundram was constituted in 1998 to examine the feasibility, constitution, organizational setup, and scope of factoring services. This group recommended setting up specialized agencies or subsidiaries with professional expertise in credit assessment, debt collection, and sales ledger management. The Vaghul Committee report on money market reforms also confirmed the need for factoring services to be developed in India as part of money market instruments. However, factoring service has not developed to any significant extent in India. Currently, factoring is rendered by only a few financial institutions, primarily on a recourse basis. The Vaghul Committee recommended that banks should be encouraged to establish factoring divisions to provide speedy finance to corporate entities. Non-Banking Financial Company – Factors (NBFC-Factors) are a registered type of NBFC specifically engaged in the principal business of factoring, where factoring constitutes at least 50% of their total assets and income.

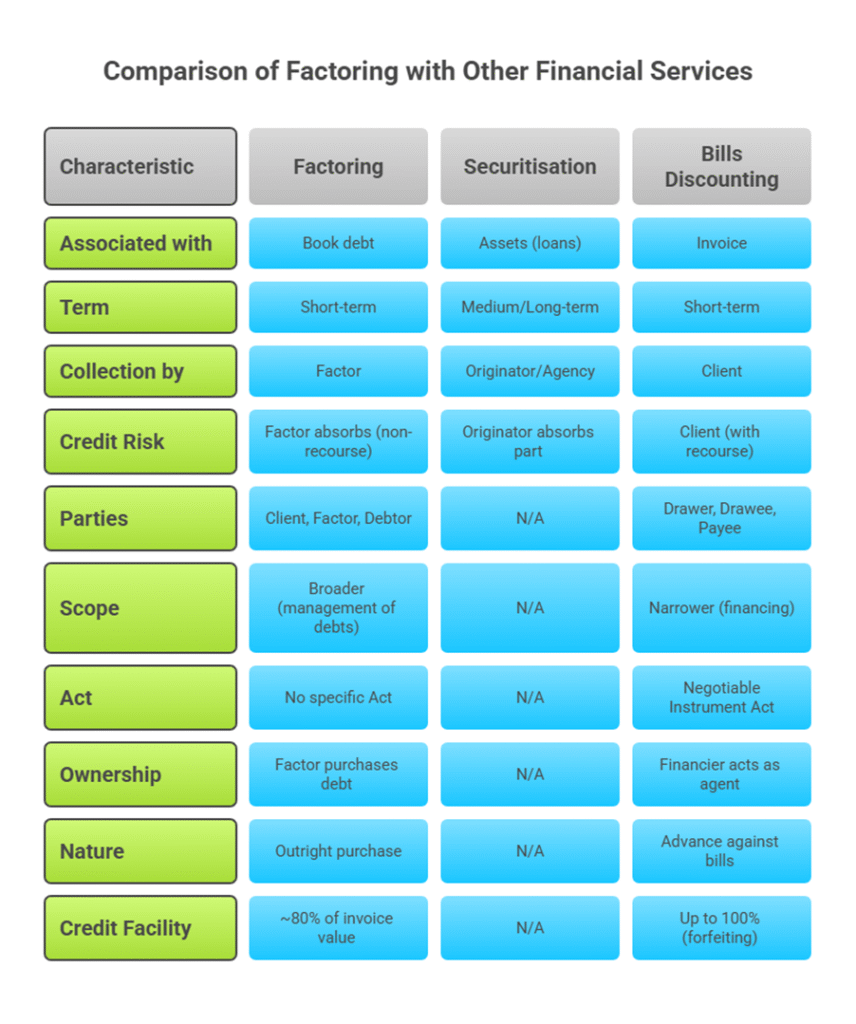

Factoring is distinct from other financial instruments and services:

- Factoring vs. Securitisation: Factoring is associated with book debt and deals with bills receivable. It is typically short-term. Collection is usually done by the factor themselves. In non-recourse factoring, the factor absorbs the whole credit risk. Securitisation, on the other hand, is associated with assets (like loans), is medium or long-term, and collection is by the originator or an agency. In securitisation, only part of the credit risk may be absorbed by the originator.

- Factoring vs. Bills Discounting: Factoring is sometimes called ‘Invoice factoring’, while bills discounting is known as “Invoice discounting”. The parties differ: client, factor, debtor in factoring; Drawer, Drawee, Payee in bills discounting. Factoring involves the management of book debts, whereas bills discounting is seen as borrowing from commercial banks. There is no specific Act for factoring, while the Negotiable Instrument Act applies to bills discounting. Under factoring, the factor purchases the trade debt and becomes a holder for value, while in discounting, the financier acts as an agent, not the owner. Discounting is an advance against bills, while factoring is an outright purchase of trade debts. Discounting is always made with recourse to the client, whereas factoring can be without recourse. Factoring is broader, including sales ledger administration, credit risk assumption, debt recovery, and consultancy, while discounting focuses mainly on financing. Factoring typically provides a credit facility of around 80% of the invoice value, whereas instruments like forfeiting (related to export bills) can provide up to 100% (less charges).

The sources provide an illustration (Illustration 18) evaluating a factoring proposal for a firm with annual credit sales of 360 lakhs and an average collection period of 30 days. The financial controller estimates bad debt losses at 2% of credit sales ( 7,20,000) and debtor administration costs at 1,40,000 annually. A factor offers to buy receivables, charging a 1% commission and an interest rate of 15% p.a. on the advance after withholding 10% as reserve. The average level of receivables is calculated as 30 lakhs (360 lakhs * 30/360 days). The factor’s commission is 1% of receivables = 30,000. Calculated annually, this is 3,60,000 (30,000 * 360/30 days). The reserve withheld is 10% of receivables = 3,00,000. The amount available for advance is 30,00,000 (receivables) – 3,30,000 (commission + reserve) = 26,70,000. Interest on the advance for 30 days at 15% p.a. is calculated as 33,375 ( 26,70,000 * 15% * 30/360 days). Calculated annually, this is ` 4,00,500 (33,375 * 360/30 days). Evaluation of the proposal:

- Savings (Benefits): Cost of Credit administration (1,40,000) + Cost of bad-debt losses ( 7,20,000) = Total Savings of ` 8,60,000.

- Costs: Factoring Commission (annual) (3,60,000) + Interest Charges (annual) ( 4,00,500) = Total Costs of ` 7,60,500.

- Net Benefits: Savings (8,60,000) – Costs ( 7,60,500) = 99,500. Since the net benefit is positive ( 99,500), the proposal is considered acceptable.

Factoring is discussed within the context of financial management as a source of finance, particularly as a short-term source, and as a method within the management of accounts receivables and working capital management.

In summary, factoring is a specialized financial service where institutions (factors) purchase a firm’s accounts receivable to provide immediate cash, manage sales ledgers, and potentially absorb credit risk, offering benefits like improved liquidity and reduced administration, though at a cost and potential perception of weakness.