Fixed Capital is a fundamental concept in financial management, representing the capital required for meeting the permanent or long-term purposes of a business concern. It is distinct from working capital, which is needed for short-term, temporary requirements.

Purpose and Nature

The primary purpose of Fixed Capital is to fund the capital expenditure of the business. It is used over a long period. This means it is the amount invested in various fixed or permanent assets that are necessary for the business to operate.

Key characteristics of Fixed Capital include:

- It is used to acquire the fixed assets of the business concern.

- It meets the capital expenditure of the business concern.

- It normally consists of a long period.

- Fixed capital expenditure is of a nonrecurring nature.

- It can be raised only with the help of long-term sources of finance.

Fixed assets themselves, which are acquired with fixed capital, are maintained over a long period. Finance managers are tasked with ensuring these assets yield reasonable returns proportionate to the investment.

Acquisition of Fixed Assets

Fixed Capital is specifically earmarked for the acquisition of fixed assets. The sources mention various examples of fixed assets, although not all are explicitly linked only to Fixed Capital funding in these excerpts. These include plant and machinery, land and building, furniture, and potentially intangible assets. Fixed assets appear in balance sheets and are subject to depreciation. The management of fixed assets is financed by long term funds.

Estimation of Fixed Capital Requirements

Estimating capital requirements is an initial and integral part of financial planning for both new and existing businesses. This process includes estimating Fixed Capital needs.

While the provided sources detail methods for estimating working capital requirements by forecasting individual current asset and liability components (like inventories, debtors, cash, creditors, etc.), the specific detailed methods for estimating Fixed Capital needs are less explicitly described in these excerpts. However, the sources indicate that the need for Fixed Capital is linked to capital expenditure plans and long-term investments.

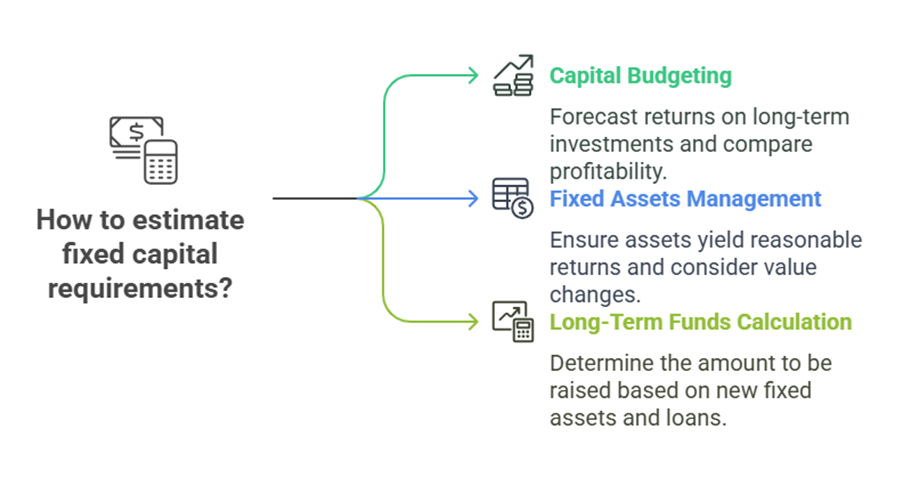

Capital budgeting is the process that forecasts returns on proposed long-term investments and compares the profitability of different investments and their cost of capital. It results in capital expenditure investment. This suggests that estimating Fixed Capital is tied to identifying, evaluating, and selecting these long-term projects and their associated asset costs. Decisions in capital budgeting affect a firm’s operations for many years [previous conversation].

One example shows the calculation of “Amount to be raised from Long Term Funds” based on the value of “New fixed assets” and existing long-term loans. Another example related to a project evaluation mentions an “additional investment” required for working capital at a later stage and a “Terminal value estimate” for fixed assets. This context suggests that estimating the capital needed for long-term projects (Fixed Capital) involves forecasting the initial investment in fixed assets and considering their future value or disposal.

Fixed assets management involves ensuring assets yield reasonable returns, and their long maintenance period exposes them to value changes. Capital budgeting techniques like payback period, internal rate of return, discounted cash flow, and net present value are relevant for evaluating these long-term investments.

Sources of Fixed Capital

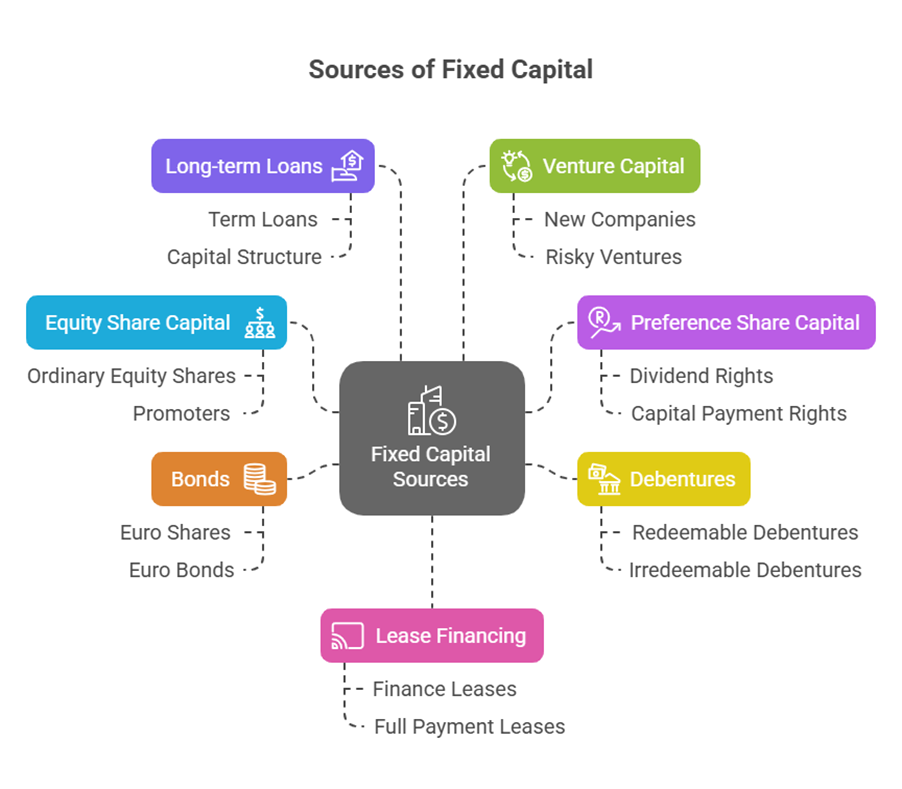

Because Fixed Capital is needed for the permanent, long-term requirements of the business, it can only be raised using long-term sources of finance. Long-term financing typically involves capital requirements for a period exceeding 5 years, often extending to 10, 15, or 20 years.

Examples of long-term sources suitable for financing Fixed Capital mentioned in the sources include:

- Equity Share Capital: This is a source of permanent capital and owners’ capital. Funds can be raised from promoters or the investing public by issuing ordinary equity shares. Equity shares are also listed as a long-term source.

- Preference Share Capital: Preference shares represent capital raised and are listed as a long-term source. They carry rights regarding receiving dividends and payment of capital.

- Debentures: Debentures are instruments for raising long-term capital with a fixed period of maturity. They are written instruments acknowledging a debt. Debentures are listed as a long-term source. Various types of debentures exist, including redeemable and irredeemable (perpetual). Irredeemable debentures are not redeemed by the issuer, and a firm may maintain a permanent part of debt capital this way.

- Bonds: A bond is a fixed income security created to raise funds. Bonds are also instruments for raising long-term capital and are listed as long-term sources (e.g., Euro shares/bonds).

- Long-term loans from financial institutions: Loans can be raised from financial institutions. Term loans are mentioned in capital structure compositions and weighted average cost of capital calculations.

- Venture Capital: Venture capital is a form of equity financing method used in relatively new companies, often for financing temporary working capital… like plant, building etc.. (Note: The source text here states “working capital like plant, building etc.”, which appears contradictory to the common understanding that plant and buildings are fixed assets and working capital finances current assets. The diagram in source links long-term sources to “Long-term”, which is consistent with financing fixed assets). Venture capital is a form of financing for new and risky ventures, providing long-term capital to enable growth.

- Lease Financing: Lease financing is mentioned as a long-term source of finance. It is a form of financing where the owner grants the right to another person to use an asset in return for periodic payments. Finance leases, a type of lease contract, are also called full payment lease, capital lease, or long term lease.

Other potential long-term sources or methods mentioned include public deposits (which can finance working capital but are also listed as a long-term source type), and debt securitisation.

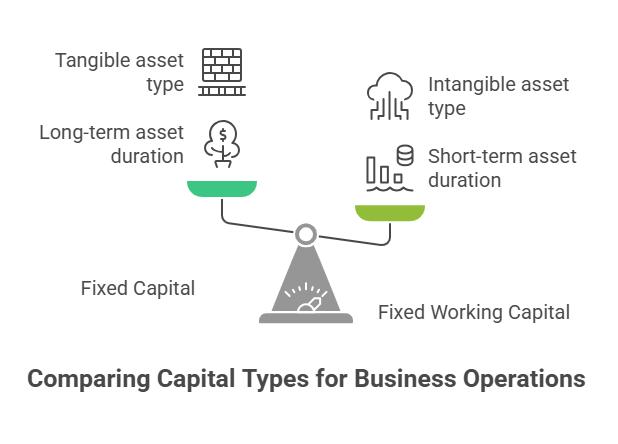

Fixed Capital vs. Working Capital

Fixed Capital is clearly distinguished from Working Capital. Working Capital is the amount of funds needed to finance current assets like stock, debtors, and cash [previous conversation]. It is for meeting short-term financial needs [previous conversation] or temporary working capital requirements.

However, there is also a concept of Permanent/Fixed working Capital. This refers to a minimum level of current assets that is continuously required by the enterprise to carry out normal business operations. For example, a firm needs to maintain minimum levels of stock and cash balance. This minimum level of current assets is called fixed working capital because this amount is permanently blocked in current assets. While containing the term “fixed”, this permanent working capital is distinct from the Fixed Capital invested in long-term fixed assets.

In summary, Fixed Capital is the long-term investment in a business’s permanent assets, crucial for its long-term operations and financed exclusively through long-term sources of funds. Its estimation is an integral part of overall financial planning, closely linked to capital budgeting decisions.