Funds Flow Analysis: An Overview

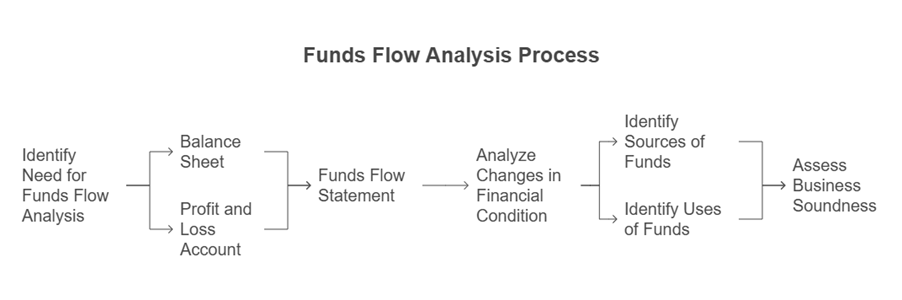

Funds Flow Analysis is a crucial tool in financial analysis and planning. While a Balance Sheet offers a static snapshot of a business’s assets and liabilities on a specific date, it does not illustrate the movement or flow of funds within the business. Businesses continuously experience the flow of funds from different sources and their investment in various avenues. The study and control of this funds flow process is a significant objective of Financial Management, aimed at assessing the soundness and solvency of a business, as well as its financing and investing activities over a given period.

The Profit and Loss Account also fails to depict the changes in a business’s financial condition between two dates. Therefore, there is a need for an additional statement that shows the changes that have occurred in assets, liabilities, and owners’ equity between the dates of two Balance Sheets. Such a statement is referred to as the Funds Flow Statement, also known as the Statement of Sources and Uses of Funds or the Statement of Changes in Financial Position.

The Funds Flow Statement serves as a technical device designed to analyze the changes in the financial condition of a business enterprise between two dates, as defined by Foulke. Anthony defines it as a statement that describes the sources from which additional funds were derived and the uses to which these sources were put.

Meaning and Concepts of “Fund”

The term “Funds” has varied meanings.

- In a Narrow Sense: Fund means only cash. A Funds Flow Statement prepared on this basis is termed a Cash Flow Statement, which accounts for only the inflow and outflow of cash.

- In a Broader Sense: The term “fund” refers to money value in whatever form it may exist. Here, funds encompass all financial resources, including men, materials, money, and machinery.

- In a Popular Sense: The term “funds” means Working Capital, specifically the excess of Current Assets over Current Liabilities. When funds move inward or outward, they create a flow or rotation of funds. In this context, “fund” refers to Net Working Capital. A statement prepared based on this definition is called a Funds Flow Statement.

The Funds Flow Statement provides a detailed analysis of changes in the distribution of resources between two Balance Sheet dates. It is a widely used tool by financial analysts, credit-granting institutions, and Finance Managers in their work. Generally, the Funds Flow Statement can present information that is either unavailable or not readily apparent from an analysis of other financial statements.

Significance and Advantages of Funds Flow Statement

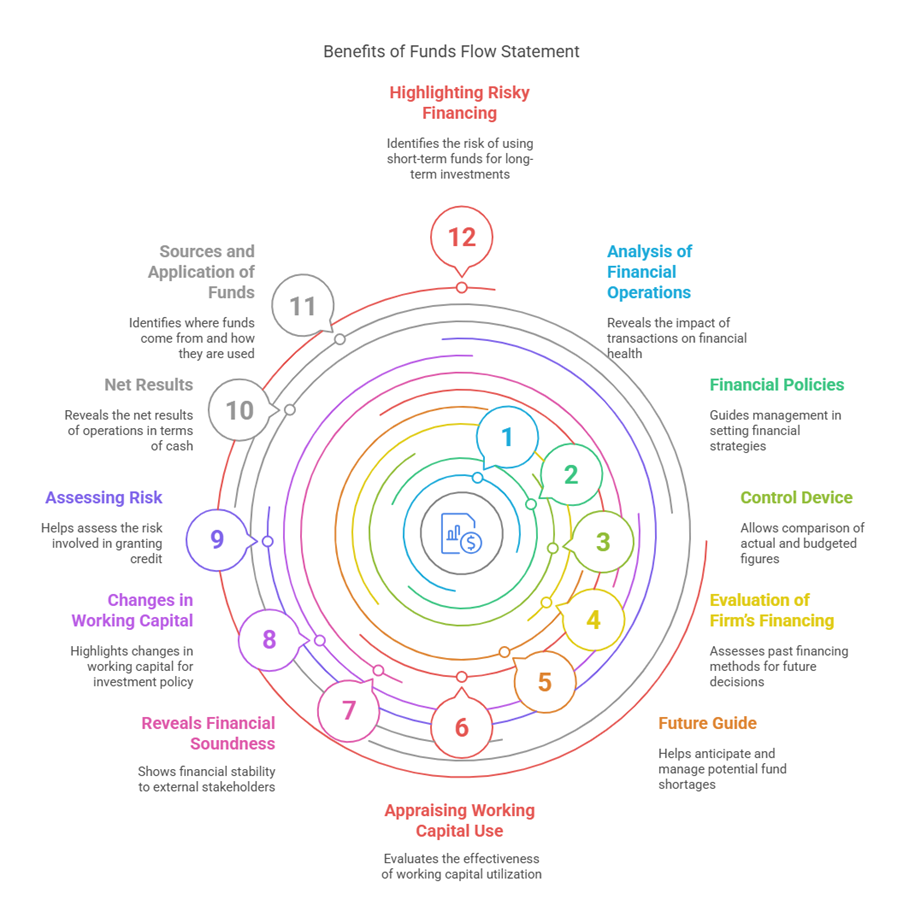

The Funds Flow Statement is considered a valuable tool in a financial manager’s analytical kit. It summarizes management decisions concerning the firm’s financing activities and investment policy.

The following are the key advantages or significance of preparing a Funds Flow Statement:

- Analysis of financial operations: It reveals the net effect of various transactions on the operational and financial position of the business. It helps determine the financial consequences of business operations and discloses the causes for changes in assets and liabilities between two points in time. It highlights the effect of these changes on the liquidity position of the company.

- Financial policies: It guides management in formulating financial policies, such as those related to dividends and reserves.

- Control device: It serves as a measure of control for management by allowing comparison of actual figures with budgeted or projected figures, enabling remedial action for deviations.

- Evaluation of firm’s financing: It assists in evaluating how the firm was financed by showing how funds were obtained from various sources and used in the past, allowing the financial manager to take corrective action based on this historical data.

- Acts as a future guide: It acts as a guide for the future for management, helping them anticipate potential problems related to fund shortages.

- Appraising the use of working capital: It helps management understand how effectively the working capital has been utilized.

- Reveals financial soundness: It reveals the financial soundness of the business to external stakeholders like creditors, banks, and financial institutions.

- Changes in working capital: It highlights the changes in working capital, which aids management in framing its investing policy.

- Assessing the degree of risk: It helps bankers, creditors, and financial institutions in assessing the degree of risk involved in granting credit to the business concern.

- Net results: It reveals the net results of operations during the year in terms of cash. (Note: While the source states “in terms of cash,” the primary focus of FFS is working capital).

- Sources and application of funds: It reveals the sources and application of funds.

- Highlighting risky financing: A major use is to identify whether the firm has used short-term sources of funds to finance long-term investments. This practice increases the risk of liquidity crunch, as long-term investments might not generate sufficient timely surplus to meet short-term liabilities, thus increasing credit and default risk.

Limitations of Funds Flow Statement Analysis

Despite its usefulness, the Funds Flow Statement has certain limitations:

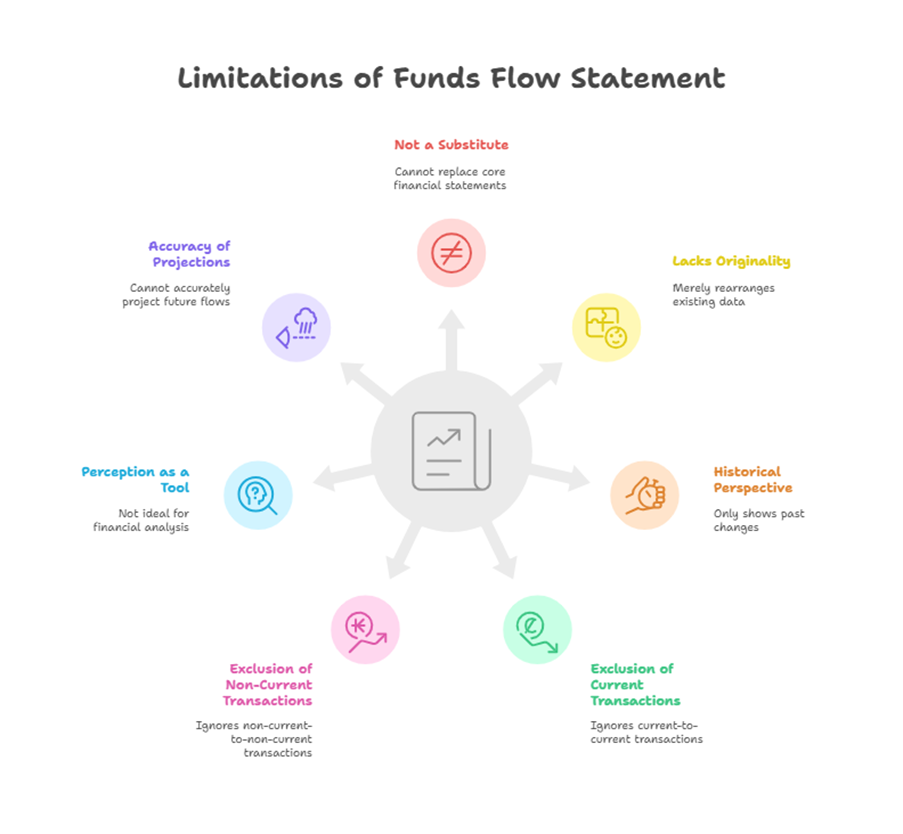

- Not a substitute: It is not a substitute for the Income Statement or the Balance Sheet. It provides only additional information regarding changes in Working Capital.

- Lacks originality: It is primarily a rearrangement of data already present in the account books.

- Historical perspective: It indicates only past changes and cannot reveal continuous fluctuations.

- Exclusion of current-to-current transactions: Transactions where both aspects are current (e.g., increase in one current asset and decrease in another) are not considered because they do not impact working capital.

- Exclusion of non-current-to-non-current transactions: Transactions where both aspects are non-current are also not included in the statement.

- Perception as a tool: Some Management Accountants are of the opinion that it is not an ideal tool for financial analysis.

- Accuracy of projections: Since it is historical in nature, projected funds flow statements cannot be prepared with high accuracy.

Preparation of Funds Flow Statement

Preparing and analyzing a Funds Flow Statement typically involves two main statements:

- Statement or Schedule of Changes in Working Capital

- Statement of Funds Flow

(I) Statement or Schedule of Changes in Working Capital: This statement shows whether the working capital has increased or decreased between two balance sheet dates. It is prepared by comparing the current assets and current liabilities of the two periods. However, it does not explain the reasons for this increase or decrease in working capital.

(II) Statement of Funds Flow (Statement of Sources and Applications of Funds): Also known as the statement of changes in financial position or where got, where gone statement. The purpose of this statement is to provide information about the enterprise’s investing and financing activities. The activities described can be categorized into two groups:

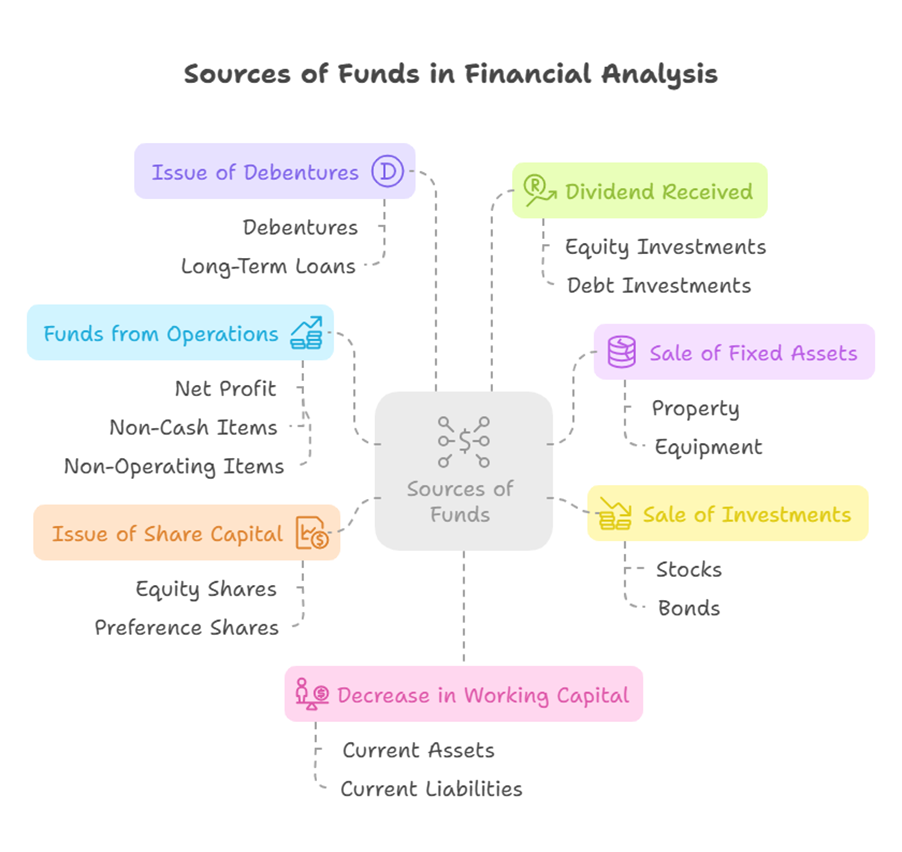

Sources of Funds (Activities that generate funds): These are activities that increase the total funds available. Examples include:

- Funds from Operations (calculated by adjusting Net Profit for non-cash and non-operating items).

- Sale of Fixed Assets.

- Sale of Investments.

- Issue of Share Capital (e.g., Equity Share Capital).

- Issue of Debentures or Long-Term Borrowings.

- Dividend Received.

- Decrease in Working Capital (This acts as a balancing figure if the total applications exceed the total sources listed above).

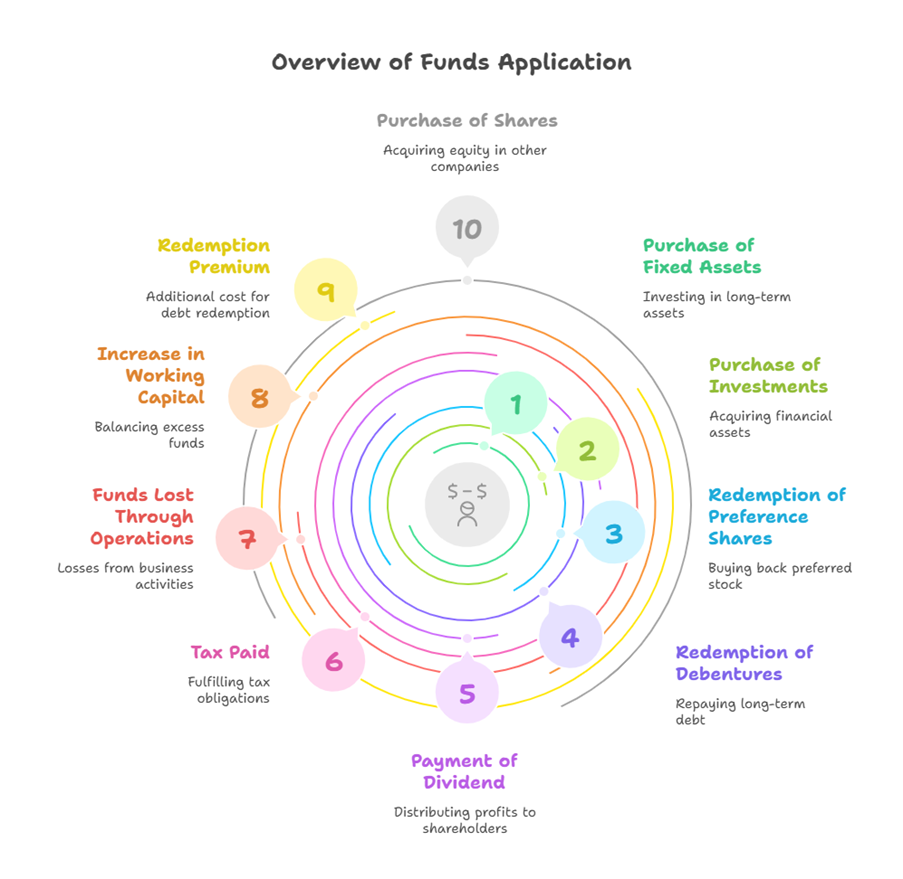

Application (Uses) of Funds (Activities that involve spending funds): These are activities that decrease the total funds available. Examples include:

- Purchase of Fixed Assets.

- Purchase of Investments.

- Redemption of Preference Shares.

- Redemption of Debentures or Repayment of Long-Term Borrowings.

- Payment of Dividend (Proposed Dividend, Interim Dividend, Preference Dividend).

- Tax Paid (unless specifically identified with financing or investing activities).

- Funds lost through business operations.

- Increase in Working Capital (This acts as a balancing figure if the total sources exceed the total applications listed above).

- Redemption Premium (on debentures).

- Purchase of shares.

If the total of funds received exceeds the total of funds applied, the difference represents excess funds, shown as an increase in working capital. Conversely, if the total of funds used exceeds the total of funds received, the difference is a shortage in fund, represented by a decrease in working capital.

Funds from Operations Calculation

Funds from Operations (FFO) represent the changes in working capital due to the operations of the business. It indicates the difference between the inflow of funds from revenue and the outflow of funds for expenses. The calculation typically starts with the Net Profit before tax and extraordinary items and adjusts for non-cash and non-operating items.

Adjustments typically include:

- Adding back non-cash expenses like Depreciation.

- Adding back non-operating losses or items that didn’t use working capital, such as Loss on sale of assets, Goodwill written off, Preliminary expenses written off, Premium on Redemption of Debentures.

- Adding back provisions like Provision for Tax and Provision for Dividend.

- Deducting non-operating gains or items that didn’t generate working capital, such as Profit on sale of assets, Dividend Received, Interest Income.

- Deducting items like Transfer to General Reserve.

- Interest Expense is also adjusted.

The resulting figure represents the Funds from Operations.

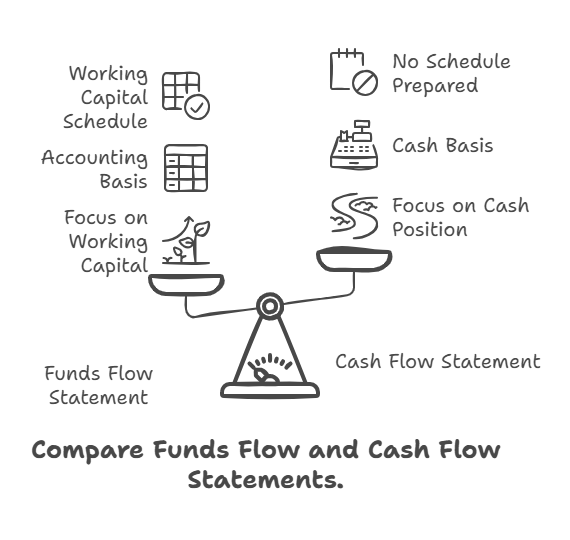

Differences between Funds Flow Statement and Cash Flow Statement

The sources highlight the key differences between a Funds Flow Statement (FFS) and a Cash Flow Statement (CFS):

| Feature | Funds Flow Statement | Cash Flow Statement |

| Focus | Reveals the change in working capital between two Balance Sheet dates. | Reveals the changes in cash position between two balance sheet dates. |

| Basis | Based on accounting (specifically the concept of working capital, which relies on accrual accounting). | Based on cash basis of accounting. |

| Working Capital Schedule | A schedule of changes in working capital is prepared. | No such schedule of changes in working capital is prepared. |

| Usefulness | More useful for planning intermediate and long-term financing. | More useful for short-term analysis and cash planning. |

| Scope | Deals with all components of working capital (current assets and current liabilities). | Deals only with cash and cash equivalents. |

| Result | Reveals sources and application of funds; the difference is the net increase or decrease in working capital. | Prepared by considering inflows and outflows from operating, investing, and financing activities; the net difference is the net increase or decrease in cash and cash equivalents. |

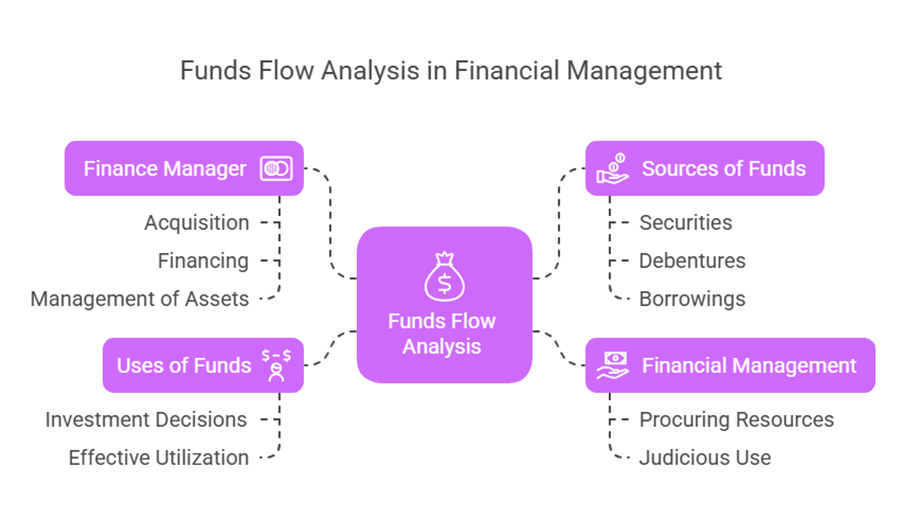

Funds Flow Analysis in Financial Management

Funds Flow Analysis is recognized as one of the important methods or tools used in the analysis of financial statements. Financial Management broadly involves the process of procuring and judicious use of financial resources with the objective of maximizing the value of the firm. Finance managers are concerned with the acquisition, financing, and management of assets. Determining the sources of funds is a key responsibility of the finance manager, who must choose carefully from various options, including securities, debentures, and borrowings from institutions. Funds Flow Analysis helps in evaluating how these financing decisions have been made and how the procured funds have been utilized, particularly in investment decisions. It aids in understanding the interplay between sources and uses of funds over a period. The effective utilization of funds, ensuring they generate income exceeding their cost, is crucial for business success. Funds Flow Analysis contributes to this by providing insights into where funds have gone.