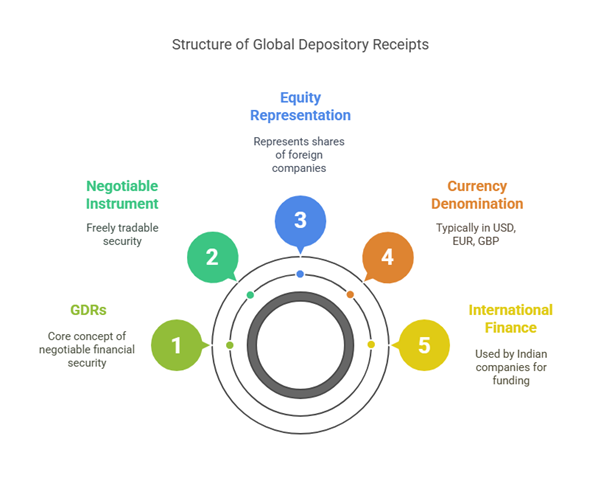

Global Depository Receipts (GDRs) are a type of negotiable financial security traded on a local stock exchange that represents a security, usually in the form of equity, issued by a foreign publicly listed company. They are certificates created by an Overseas Depository Bank outside India and issued to non-resident investors against the issue of ordinary shares. A GDR is essentially a negotiable certificate held in a bank of one country representing a specific number of shares of stock traded on the exchange of another country.

GDRs allow investors to hold shares in equity of other countries via a physical certificate. They are generally denominated in US dollars, although some can be denominated in Euro and Pound Sterling. In theory, a depository receipt could represent a debt instrument, but in practice, this rarely happens. GDRs are a type of negotiable instrument and can be traded freely like any other security.

In the Indian context, a GDR is an instrument issued abroad by an Indian company to raise funds in some foreign currency. They represent shares issued in the local currency. Indian companies primarily use GDRs as a source of international finance.

Purpose and Driving Forces

Companies issue GDRs to raise capital in foreign currency, typically dollars or Euros. Issuing DRs (including GDRs) functions as a means to increase global trade, which can boost volumes on local and foreign markets and enhance the exchange of information, technology, and regulatory procedures, as well as market transparency.

For a company, opting to issue a DR can lead to greater exposure and help raise capital in the world market. It also has the benefit of increasing the share’s liquidity while boosting the company’s prestige on its local market. Issuing depository receipts encourages an international shareholder base and provides expatriates living abroad with an easier opportunity to invest in their home countries. By issuing a DR, a company can encourage investment from abroad even if obstacles in their local market prevent foreign investors from entering directly.

Mechanism and Working

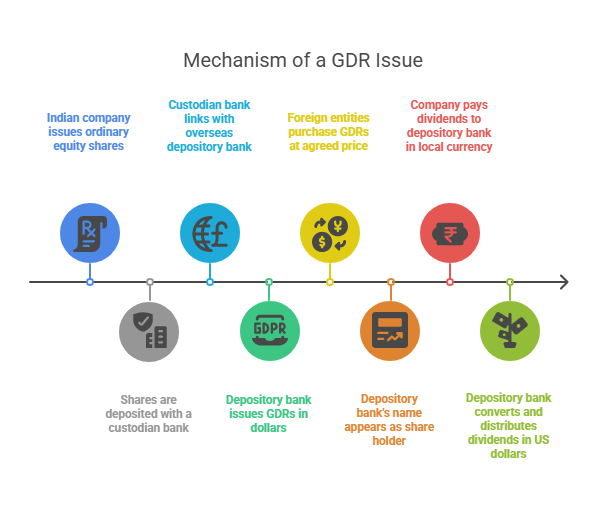

The mechanism of a GDR issue can be described in several steps:

- An Indian company issues ordinary equity shares.

- These shares are deposited with a custodian bank, usually a domestic bank.

- The custodian bank establishes a link with a depository bank overseas.

- The depository bank issues depository receipts (GDRs) in dollars.

- Funds are raised when foreign entities purchase these depository receipts at an agreed price.

- In the company’s books, the Depository Bank’s name appears as the holder of the shares.

- The issuing company pays dividends on such issues to the depository bank in local currency.

- The depository bank converts the dividends into US Dollars at the ruling exchange rate and distributes it among the GDR holders.

The depository bank has the right to issue one GDR certificate for a specific number of shares, such as 2 to 10 shares.

Characteristics of GDRs

GDRs possess several key characteristics:

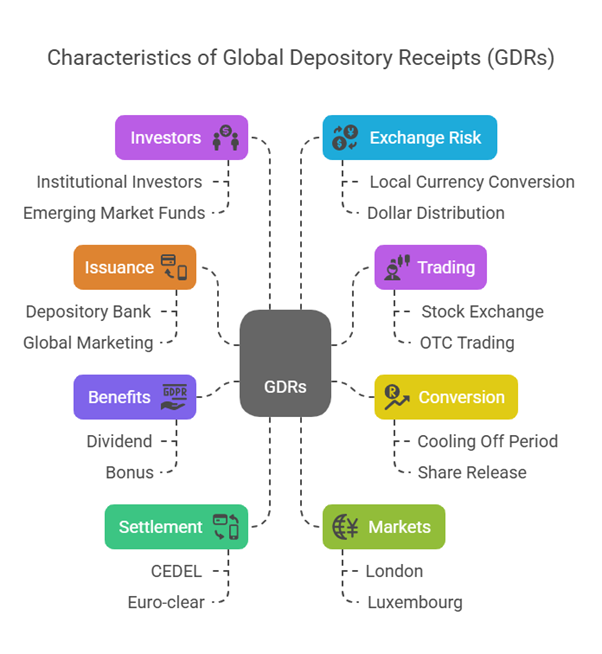

- Issued to Investors in More Than One Country: GDRs are marketed globally and can be issued to investors in multiple countries.

- Denomination: They may be denominated in any acceptable freely convertible currency, but are most commonly in US Dollars.

- Issuer: GDRs are issued to investors by the depository bank, not by the issuing company itself.

- Voting Rights: Holders of GDRs generally do not carry any voting rights. The voting rights accrue only to the depository bank.

- Value Derivation: The GDR derives its value through the price of the underlying shares and the current exchange rate.

- Security Status: They are described as unsecured securities in one source, not backed by any assets other than the value of the shares mentioned in the certificate.

- Tradability: GDRs are freely negotiable and can be traded freely in the international market either through a stock exchange, over the counter (OTC), or among Qualified International Buyers (QIB). Trading takes place between professional market makers on an OTC basis. They are also traded on the Exchange’s Electronic Trading Service, the International Order Book (IOB).

- Conversion (Fungibility): GDR holders typically have the option of converting GDRs into the number of shares it represents. This provision can usually be used only after a “Cooling off” period of 45 days from the date of issue. Upon cancellation, the overseas depository bank requests the domestic custodian bank to release the corresponding underlying shares to the non-resident investor.

- Corporate Benefits: GDR holders are entitled to all corporate benefits available to equity holders, such as dividend, bonus and rights, in the same proportion as their entitlement.

- Settlement: GDRs are settled through CEDEL & Euro-clear international book entry systems. More liquid IOB securities have central counterparty clearing.

- Markets: GDRs are mainly traded in European countries, particularly in London, and also commonly listed on European stock exchanges. Most Indian companies have their GDR issues listed on the Luxembourg Stock Exchange and the London Stock Exchange. They are marketed globally.

- Investors: GDRs are sold primarily to institutional investors. Demand is likely dominated by emerging market funds. Major demand is also in the UK, USA (Qualified Institutional Buyers), South East Asia (Hong Kong, Singapore), and to some extent continental Europe (principally France and Switzerland).

- Exchange Risk: The exchange risk is borne by the investors as dividend payment is made in local currency and converted into dollars by the depository for distribution.

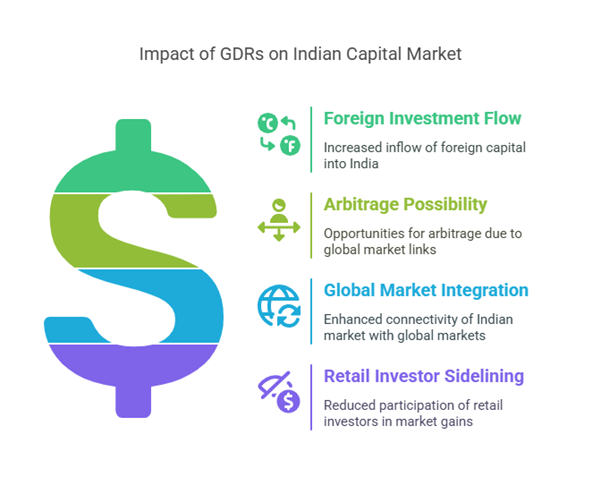

Impact on Indian Capital Market

The introduction of GDRs has had a notable impact on the Indian capital market:

- It has contributed to a considerable flow of foreign investment into India.

- There is an arbitrage possibility in GDR issues, which requires investors to keep updated with worldwide economic events and how the company’s GDRs are trading.

- The Indian stock market is now linked to the rest of the world.

- Indian retail investors have been sidelined, as GDRs and Foreign Institutional Investor placements, along with free pricing, mean retail investors can no longer expect easy money on heavily discounted rights/public issues.

Distinction from Other Instruments

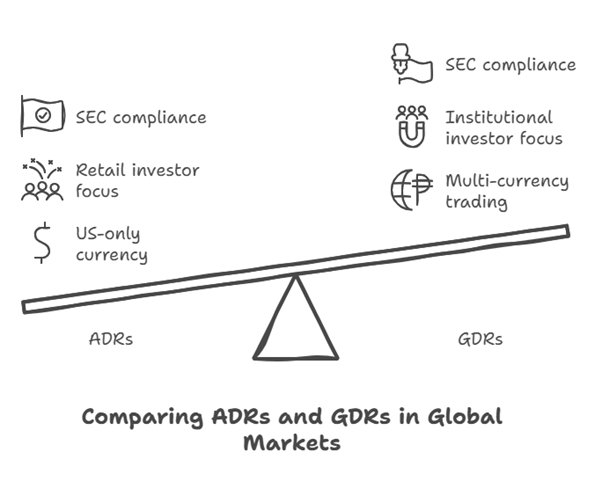

- ADRs vs. GDRs: American Depository Receipts (ADRs) are depository receipts specifically issued in the United States of America and must comply with stringent SEC provisions. ADRs are typically traded on US national stock exchanges (NYSE, AMEX, Nasdaq). GDRs are identical in structure to ADRs, but the key difference is they can be traded in more than one currency and within as well as outside the United States. While ADRs are used for funds raised through the retail market in the United States, in the case of GDR issues, the invitation to participate cannot be extended to retail US investors, implying they are primarily for institutional investors or QIBs. There is no essential difference between ADR and GDR from a legal point of view.

- IDRs vs. GDRs: Indian Depository Receipts (IDRs) are the Indian version for foreign companies. The foreign company deposits shares with an Indian Depository (SEBI registered custodian), which issues receipts to Indian investors. IDRs are issued to Indian residents like domestic shares are (public offer, residents bid). This contrasts with GDRs which are issued by Indian companies abroad to non-resident investors.

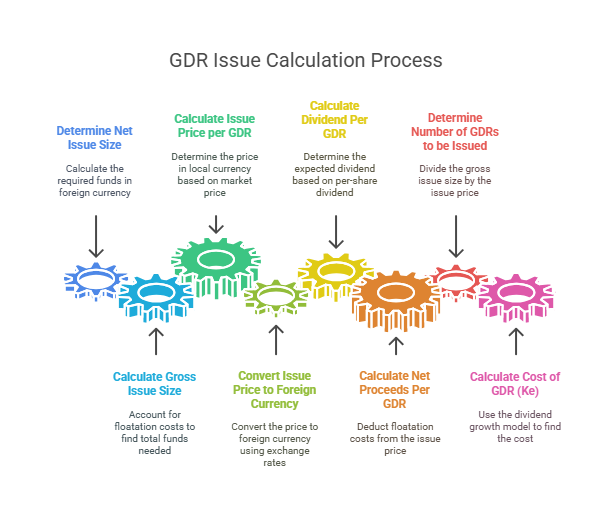

Illustration of GDR Issue Calculation

Sources and provide examples of calculating the number of GDRs to be issued and the cost of the GDR issue for a company raising funds for a project. The calculations involve:

- Determining the Net Issue Size required in foreign currency.

- Calculating the Gross Issue size by accounting for floatation costs.

- Calculating the Issue Price per GDR in the local currency based on the market price of the underlying share, the conversion ratio (shares per GDR), and any discount offered.

- Converting the Issue Price per GDR to the foreign currency using the expected exchange rate.

- Calculating the expected Dividend Per GDR based on the per-share dividend and the conversion ratio.

- Calculating the Net Proceeds Per GDR by deducting floatation costs from the issue price per GDR (in local currency).

- Determining the Number of GDRs to be Issued by dividing the Gross Issue size (in foreign currency) by the Issue Price per GDR (in foreign currency).

- Calculating the Cost of GDR (Ke) to the company, often using the dividend growth model formula: Ke = (D1 / P0) + g, where D1 is the expected dividend per GDR, P0 is the net proceeds per GDR, and g is the expected growth rate of dividends.