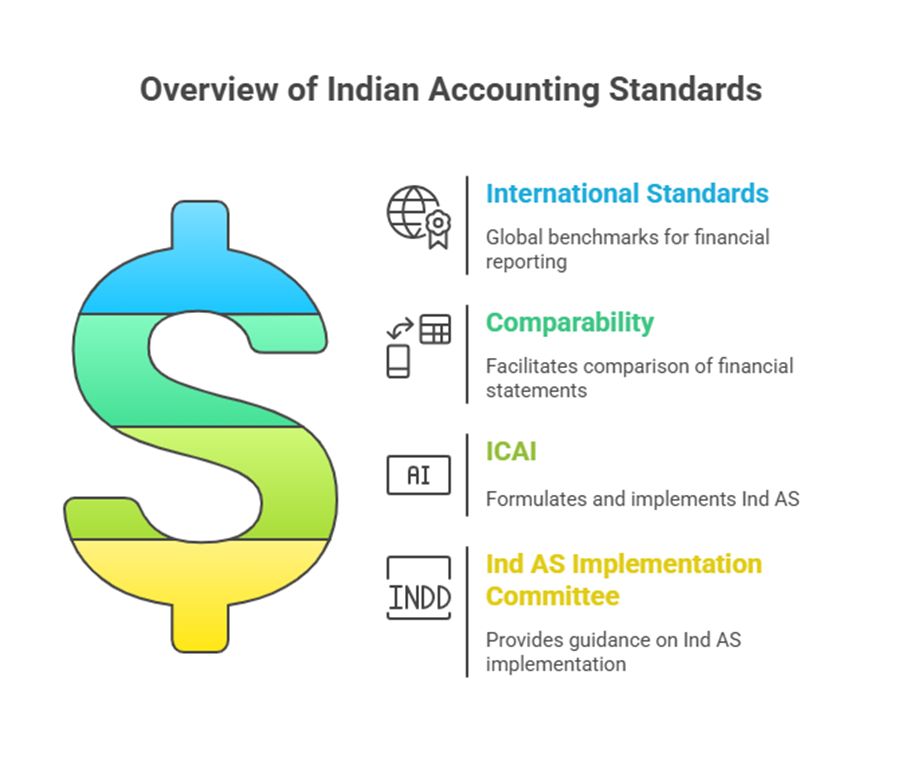

Indian Accounting Standards (Ind AS) represent a significant step towards converging Indian financial reporting practices with international standards. This convergence is driven by the need for comparability of financial statements on an international level, making it easier for users to compare the performance of entities from different countries. Ind AS are converged International Financial Reporting Standards (IFRS).

The Institute of Chartered Accountants of India (ICAI), established by an Act of Parliament, is an active formulator of these IFRS-converged Indian Accounting Standards and is responsible for their successful and proper implementation. To this end, the ICAI, through its Ind AS Implementation Committee, provides guidance to its members and other stakeholders.

Here is an overview of some of the key Indian Accounting Standards:

Ind AS 101, First-time Adoption of Indian Accounting Standards This standard is crucial as it prescribes the accounting principles and transition requirements for entities adopting Ind AS for the first time, moving from previous GAAP (Generally Accepted Accounting Principles) in India. The objective is to ensure that the first Ind AS financial statements are transparent, comparable, provide a suitable starting point for future Ind AS accounting, and that the cost of transition does not exceed the benefits. Conceptually, Ind AS accounting should be applied retrospectively at the time of transition. However, Ind AS 101 provides certain exemptions to ease this process. These include mandatory exceptions, where retrospective application is prohibited, and voluntary exemptions, where an entity may elect not to apply certain requirements retrospectively. Mandatory exceptions cover areas like estimates, derecognition of financial assets/liabilities, hedge accounting, non-controlling interests, classification/measurement of financial assets, impairment of financial assets, embedded derivatives, and government loans. Voluntary exemptions are provided where retrospective application could be difficult or result in undue cost. A key requirement of Ind AS 101 is the preparation and presentation of an opening Ind AS Balance Sheet at the date of transition. This balance sheet serves as the starting point for all subsequent Ind AS accounting. The same accounting policies, compliant with Ind AS effective at the end of the first reporting period, must be applied consistently in this opening balance sheet and throughout all periods presented. In the opening balance sheet, an entity must recognise all assets/liabilities required by Ind AS, not recognise items not permitted, reclassify items recognised differently under previous GAAP, and apply Ind AS measurement principles. Adjustments arising from this transition are recognised directly in retained earnings (or another equity category) at the transition date. Ind AS 101 does not provide exemptions from the presentation and disclosure requirements of other Ind ASs. It specifically requires disclosures that explain the effect of the transition from previous GAAP on the entity’s reported financial position, performance, and cash flows. This includes reconciliations of equity and total comprehensive income from previous GAAP to Ind AS at the date of transition and the end of the last previous GAAP annual period, explanations of material adjustments, disclosure of errors found, and explanations if specific exemptions were applied.

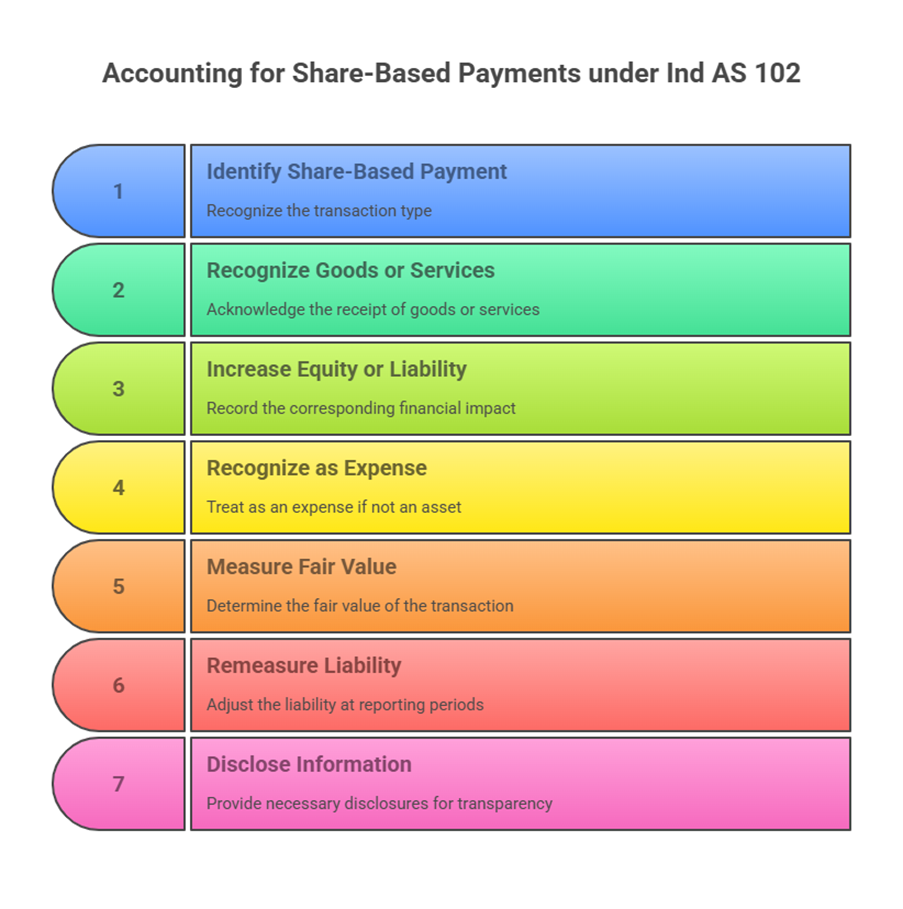

Ind AS 102, Share-based Payment This standard specifies the financial reporting for share-based payment transactions. An entity recognises the goods or services obtained in such a transaction and a corresponding increase in equity for equity-settled transactions or a liability for cash-settled transactions. If the goods or services do not qualify as assets, they are recognised as expenses. The standard sets out specific measurement and requirements for different types of share-based payment transactions. For cash-settled transactions, the liability is remeasured at fair value at the end of each reporting period and at settlement, with changes recognised in profit or loss. Disclosures are required to help users understand the nature/extent of arrangements, how fair value was determined, and the effect on profit/loss and financial position.

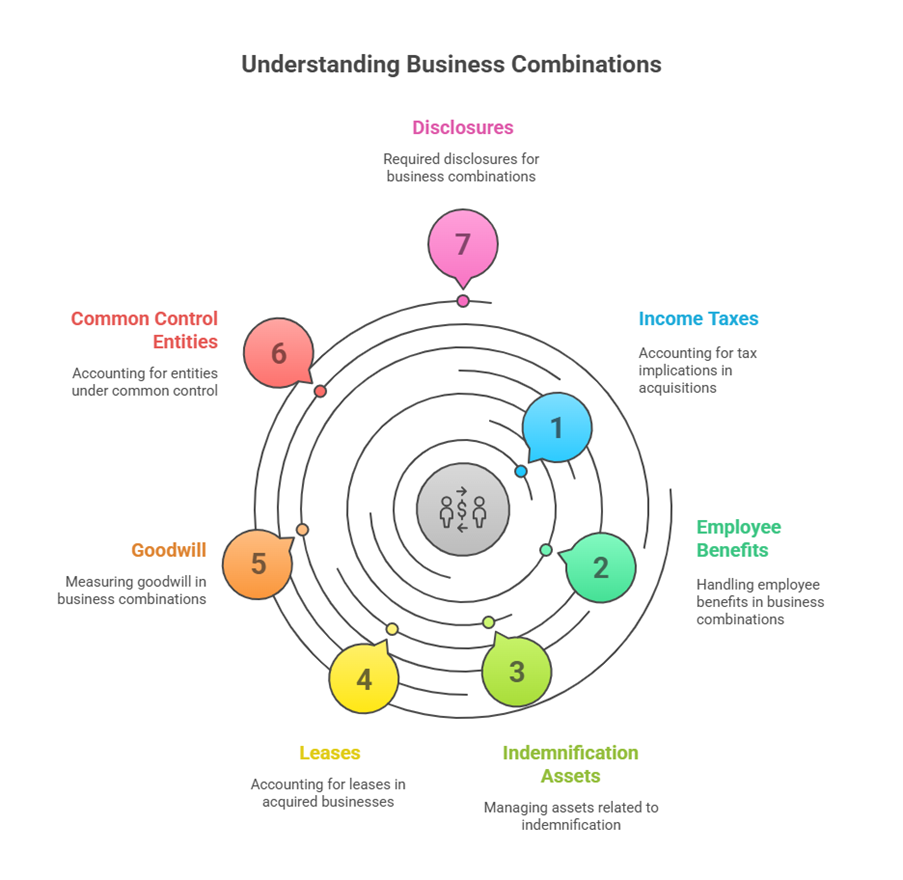

Ind AS 103, Business Combinations Ind AS 103 deals with the accounting for business combinations. A business combination occurs when an acquirer obtains control of one or more businesses. The standard provides guidance on various aspects, including the accounting for specific items like income taxes, employee benefits, indemnification assets, and leases in the acquired business. Goodwill is measured as the difference between the consideration transferred and the net acquisition-date amounts of the acquiree’s identifiable assets and liabilities. The standard also addresses business combinations of entities under common control, where assets and liabilities are typically recognised at carrying amounts. Disclosures are required for each business combination during the reporting period.

Ind AS 104, Insurance Contracts This standard specifies the financial reporting for entities that issue insurance contracts. It applies to insurance contracts issued, reinsurance contracts held, and financial instruments with discretionary participation features. The standard allows limited improvements to accounting and permits some exceptions from other Ind AS requirements. It allows insurers to change accounting policies only if the change enhances relevance and reliability. Disclosures are required to help users understand amounts arising from insurance contracts and related risks.

Ind AS 105, Non-current Assets Held for Sale and Discontinued Operations Ind AS 105 prescribes the accounting for assets classified as held for sale and the presentation/disclosure of discontinued operations. Assets meeting the criteria to be classified as held for sale are measured at the lower of their carrying amount and fair value less costs to sell, and depreciation ceases on such assets. These assets, and the results of discontinued operations, must be presented separately in the financial statements.

Ind AS 106, Exploration for and Evaluation of Mineral Resources This standard specifies financial reporting for the exploration for and evaluation of mineral resources. It permits entities to develop accounting policies for exploration and evaluation assets using guidance from Ind AS 8. A key requirement is the impairment testing of these assets when facts and circumstances suggest the carrying amount may exceed the recoverable amount. Impairment measurement follows Ind AS 36. Disclosures must identify and explain amounts arising from these activities, treating exploration and evaluation assets as a separate class.

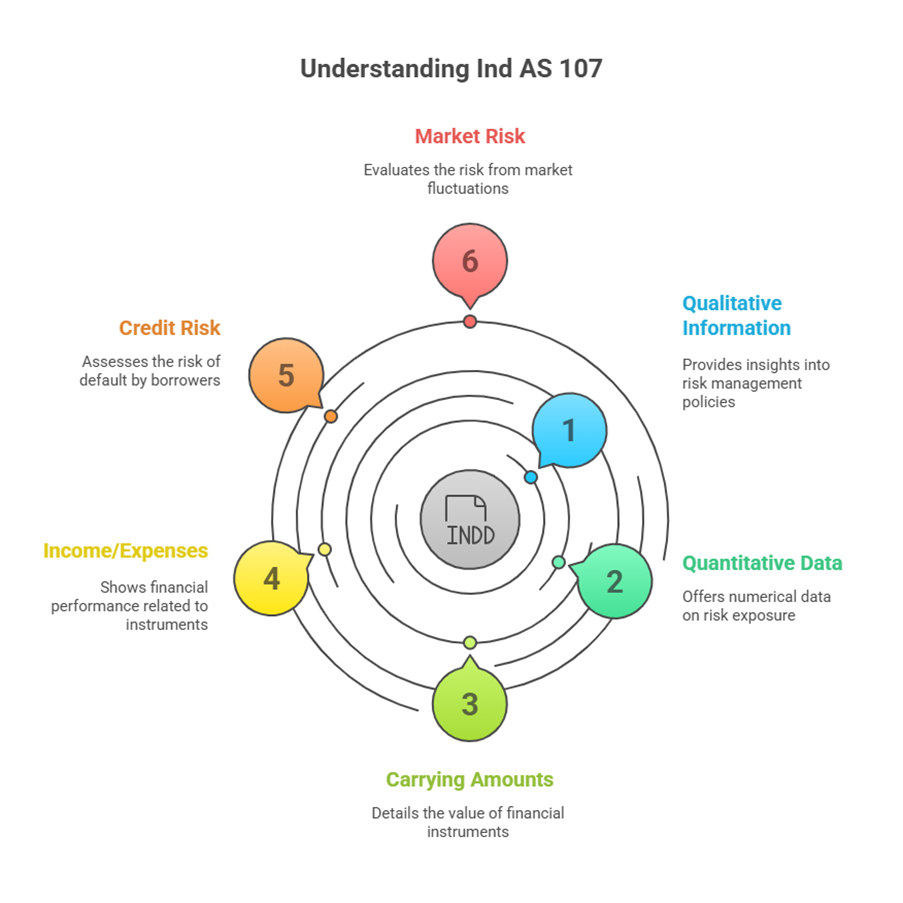

Ind AS 107, Financial Instruments: Disclosures Ind AS 107 requires entities to provide disclosures that help users evaluate the significance of financial instruments and the nature and extent of risks arising from them. It applies to all entities. Disclosures include both qualitative information about risk management policies and quantitative data about risk exposure. The standard complements the recognition, measurement, and presentation principles in Ind AS 32 and Ind AS 109. It requires detailed disclosures about carrying amounts of financial instruments, income/expenses from financial instruments, and risks such as credit risk and market risk.

Ind AS 108, Operating Segments This standard requires entities to disclose information that enables users to evaluate the nature and financial effects of their business activities and economic environments. It mandates reporting financial and descriptive information about reportable segments, which are operating segments or aggregations meeting specific criteria.

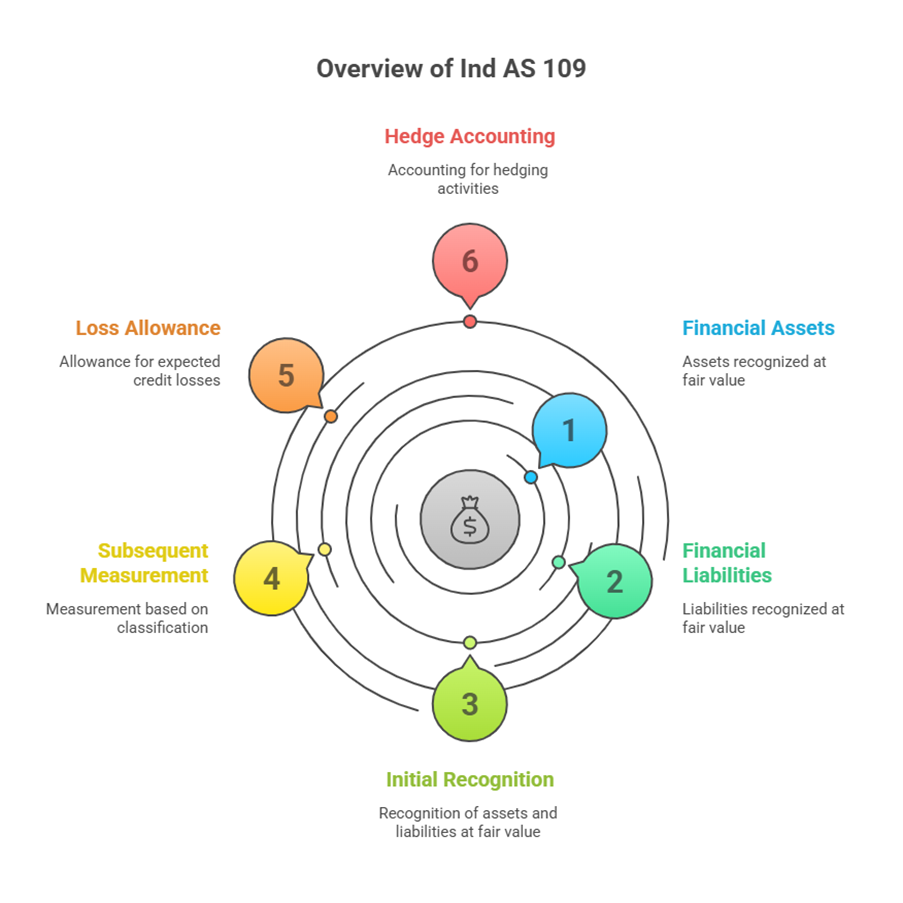

Ind AS 109, Financial Instruments Ind AS 109 establishes principles for the financial reporting of financial assets and financial liabilities, aiming to provide relevant and useful information about amounts, timing, and uncertainty of future cash flows. It applies to various financial instruments with specified scope exclusions. Financial assets and liabilities are initially recognised at fair value. Subsequent measurement depends on their classification. The standard requires recognising a loss allowance for expected credit losses on certain financial assets and covers requirements for hedge accounting.

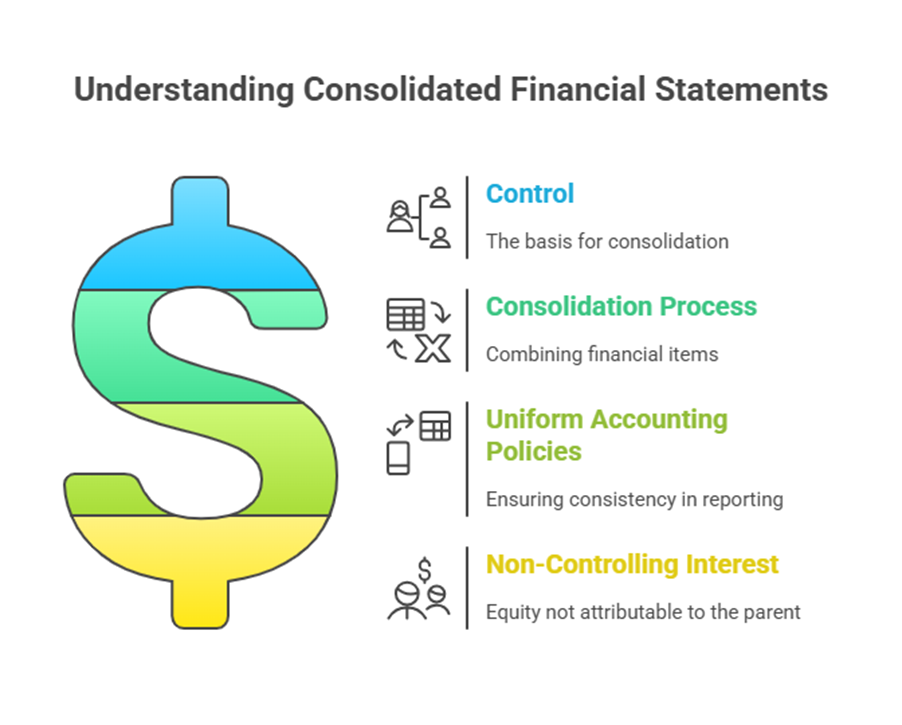

Ind AS 110, Consolidated Financial Statements This standard sets principles for the presentation and preparation of consolidated financial statements (CFS) when an entity controls one or more other entities. CFS present the financial position, performance, and cash flows of a parent and its subsidiaries as those of a single economic entity. Control is the basis for consolidation. Consolidated financial statements combine like items, eliminate the parent’s investment and subsidiary equity, and eliminate intragroup balances and transactions. Uniform accounting policies are required. The standard also deals with non-controlling interest (NCI), which is the equity in a subsidiary not attributable to the parent.

Ind AS 111, Joint Arrangements Ind AS 111 establishes principles for accounting for joint arrangements. For a joint venture, a joint venturer must recognise its interest as an investment and account for it using the equity method unless exempted. For a joint operation, a venturer recognises its direct share of assets, liabilities, revenue, and expenses.

Ind AS 112, Disclosure of Interests in Other Entities This standard requires disclosures that allow users to evaluate the nature and risks associated with an entity’s interests in other entities (subsidiaries, joint arrangements, associates, unconsolidated structured entities) and their effects on the financial statements. It mandates specific disclosures for each type of interest.

Ind AS 113, Fair Value Measurement Ind AS 113 provides guidance on measuring fair value when another standard requires or permits it. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The standard does not apply to certain items like share-based payments, leases, or measurements similar to fair value but not fair value (e.g., NRV, value in use). It requires disclosures about valuation techniques and inputs used for fair value measurements.

Ind AS 114, Regulatory Deferral Accounts This standard permits entities conducting rate-regulated activities to continue recognising amounts that qualify as regulatory deferral account balances, provided they did so under previous GAAP. If applied, entities must present separate line items in the balance sheet for total debit and credit regulatory deferral account balances. Disclosures are required to enable users to assess the nature and risks of rate regulation and its effects.

Ind AS 115, Revenue from Contracts with Customers Ind AS 115 establishes principles for reporting information about the nature, amount, timing, and uncertainty of revenue and cash flows arising from contracts with customers. The core principle is that an entity recognises revenue to depict the transfer of promised goods or services to customers. The standard outlines a five-step model for revenue recognition. It requires presentation of contracts in the balance sheet as contract assets, contract liabilities, or receivables.

Ind AS 116, Leases This standard sets out principles for the recognition, measurement, presentation, and disclosure of leases. For lessees, it requires the recognition of a right-of-use asset and a lease liability at the commencement date, unless the entity elects for recognition exemption for short-term or low-value leases. For lessors, it requires classifying leases as either finance leases (transferring substantially all risks and rewards of ownership) or operating leases. The standard requires specific disclosures for both lessees and lessors.

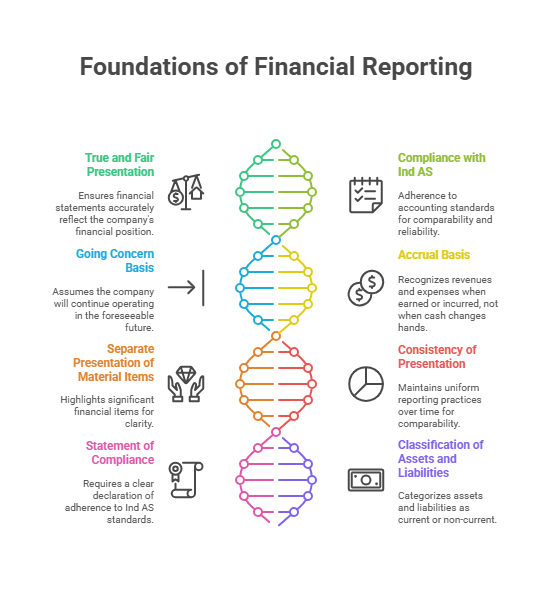

Ind AS 1, Presentation of Financial Statements Ind AS 1 prescribes the basis for presenting general purpose financial statements to ensure comparability. It sets overall requirements, structure, and minimum content. A complete set of financial statements includes a balance sheet, statement of profit and loss, statement of changes in equity, statement of cash flows, notes, and comparative information. Key features include true and fair presentation, compliance with Ind AS, going concern basis, accrual basis (except cash flows), separate presentation of material items, and consistency of presentation. An explicit and unreserved statement of compliance with Ind AS is required if the financial statements meet all Ind AS requirements. The standard provides line items to be presented and requires assets and liabilities to be generally classified as current or non-current.

Ind AS 2, Inventories Ind AS 2 prescribes the accounting treatment for inventories, including determining cost, recognition as expense, and write-downs to net realisable value (NRV). Inventories are defined as assets held for sale, in production, or materials for production. Inventories are measured at the lower of cost and NRV. Permitted cost formulas are FIFO or weighted average cost.

Ind AS 7, Statement of Cash Flows This standard requires providing information about historical changes in cash and cash equivalents by classifying cash flows from operating, investing, and financing activities. It defines cash and cash equivalents. The statement reports cash flows and reconciles beginning and ending cash and cash equivalents.

Ind AS 8, Accounting Policies, Changes in Accounting Estimates and Errors Ind AS 8 provides criteria for selecting and changing accounting policies and the accounting/disclosure for changes in policies, estimates, and corrections of errors. It aims to enhance the relevance, reliability, and comparability of financial statements. Accounting policies are followed as per applicable Ind AS or developed using judgment if no specific standard exists. Changes in accounting policy are generally applied retrospectively. Changes in accounting estimates are recognised prospectively. Prior period errors are corrected by retrospective restatement.

Ind AS 10, Events after the Reporting Period This standard guides the accounting for events occurring between the reporting period end and the date financial statements are approved. Adjusting events provide evidence of conditions existing at the reporting date and require financial statement adjustments. Non-adjusting events are indicative of conditions arising after the reporting period and are disclosed if material. Dividends declared after the reporting period are not recognised as a liability at the reporting date.

Ind AS 12, Income Taxes Ind AS 12 prescribes the accounting for income taxes. It is based on the balance sheet approach, requiring recognition of the tax consequences of differences between the carrying amounts of assets/liabilities and their tax bases. It deals with current and deferred tax, including deferred tax assets from unused tax losses/credits.

Ind AS 16, Property, Plant and Equipment Ind AS 16 prescribes the accounting for Property, Plant and Equipment (PPE). PPE is initially recognised at cost. Subsequent measurement can be under the cost model or the revaluation model. The standard also covers depreciation, impairment (referencing Ind AS 36), and derecognition.

Ind AS 19, Employee Benefits This standard prescribes accounting and disclosure for employee benefits. It requires recognising a liability when an employee has provided service for future benefits and an expense when the economic benefit of the service is consumed. It covers various types of employee benefits, including short-term and long-term benefits.

Ind AS 20, Accounting for Government Grants and Disclosure of Government Assistance Ind AS 20 provides accounting for government grants and assistance. Grants are not recognised until there is reasonable assurance of compliance with conditions and receipt. Grants related to assets can be presented as deferred income or deducted from the asset. Grants related to income are presented in profit or loss. Repayments are treated as changes in accounting estimates.

Ind AS 21, The Effects of Changes in Foreign Exchange Rates This standard prescribes how to include foreign currency transactions and foreign operations in financial statements. It addresses the recognition of exchange differences, which are generally recognised in profit or loss for monetary items, but in other comprehensive income for the net investment in a foreign operation in consolidated statements.

Ind AS 24, Related Party Disclosures Ind AS 24 ensures disclosure of information about related party relationships, transactions, and outstanding balances to highlight potential effects on financial statements. It defines a related party and requires specific disclosures about the nature and amount of transactions and balances, unless prohibited by law (e.g., bank confidentiality).

Ind AS 27, Separate Financial Statements This standard prescribes accounting and disclosure for investments in subsidiaries, joint ventures, and associates when an entity presents separate financial statements. In separate financial statements, these investments are accounted for either at cost or in accordance with Ind AS 109. Dividends from these investments are recognised in profit or loss when the right to receive is established.

Ind AS 28, Investments in Associates and Joint Ventures Ind AS 28 sets out requirements for applying the equity method when accounting for investments in associates (where the investor has significant influence) and joint ventures (unless exempted). Under the equity method, the investment is initially recognised at cost and subsequently adjusted for the investor’s share of the investee’s profit/loss and other comprehensive income. Distributions received reduce the investment carrying amount. Goodwill is included in the investment carrying amount and not amortised.

Ind AS 29, Financial Reporting in Hyperinflationary Economies This standard applies to entities whose functional currency is the currency of a hyperinflationary economy. Its objective is to ensure that financial statements are reported in a way that addresses the loss of purchasing power. It requires restating financial statements so that all amounts are stated in terms of the measuring unit current at the end of the reporting period. A gain or loss on the net monetary position is recognised in profit or loss.

Ind AS 32, Financial Instruments: Presentation Ind AS 32 establishes principles for presenting financial instruments as financial liabilities or equity instruments and for offsetting them. It provides definitions for financial instrument, financial asset, financial liability, and equity instrument. It also addresses the accounting for compound financial instruments (splitting liability and equity components) and treasury shares (deducted from equity). Offsetting of financial assets and liabilities is permitted only under specific conditions (legally enforceable right and intention to settle net or simultaneously).

Ind AS 33, Earnings per Share Ind AS 33 prescribes principles for the determination and presentation of Earnings per Share (EPS) to enhance comparability. It applies to companies that have issued ordinary shares and disclose EPS. The standard focuses on the denominator of the EPS calculation (the number of shares). It requires calculating and presenting both basic EPS and diluted EPS. Basic EPS is profit/loss attributable to ordinary equity holders divided by the weighted average number of ordinary shares outstanding. Diluted EPS adjusts for the effect of dilutive potential ordinary shares.

Ind AS 34, Interim Financial Reporting Ind AS 34 prescribes the minimum content of an interim financial report and principles for recognition/measurement in interim financial statements. An interim financial report can contain a complete set of financial statements or, at a minimum, condensed financial statements and selected explanatory notes. Minimum components include condensed balance sheet, profit/loss, changes in equity, cash flows, and selected notes. Entities must present basic and diluted EPS in the interim profit/loss statement if applicable. Accounting policies should generally be the same as in the annual statements.

Ind AS 36, Impairment of Assets Ind AS 36 prescribes procedures to ensure assets are carried at no more than their recoverable amount (the higher of fair value less costs of disposal and value in use). An asset is impaired if its carrying amount exceeds its recoverable amount. The standard requires assessing for impairment indications at the end of each reporting period and recognising an impairment loss if necessary. An impairment loss recognised for goodwill shall not be reversed in a subsequent period.

Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets Ind AS 37 ensures appropriate recognition, measurement, and disclosure for provisions, contingent liabilities, and contingent assets. A provision is recognised when there is a present obligation from a past event, payment is probable, and the amount can be reliably estimated. Contingent liabilities and contingent assets are generally not recognised. The standard provides specific guidance for onerous contracts and restructuring provisions.

Ind AS 38, Intangible Assets Ind AS 38 prescribes accounting for intangible assets not covered by other standards. An intangible asset is recognised if specific criteria are met. It is initially measured at cost. Subsequent measurement can be under the cost model or revaluation model. Intangible assets are amortised over their useful lives unless they have an indefinite useful life.

Ind AS 40, Investment Property Ind AS 40 prescribes accounting for investment property (property held to earn rentals or for capital appreciation). Investment property is initially measured at cost. After initial recognition, under the required cost model, it is subsequently measured in accordance with other standards like Ind AS 105 (if held for sale), Ind AS 116 (if right-of-use asset not held for sale), or Ind AS 16 (cost model). Disclosure of fair value is required even under the cost model. Transfers to or from investment property occur only on a change in use.

Ind AS 41, Agriculture Ind AS 41 prescribes accounting for agricultural activity. Biological assets (living animals or plants) are generally measured at fair value less costs to sell, with changes in fair value recognised in profit or loss. Agricultural produce harvested from biological assets is measured at fair value less costs to sell at the point of harvest.

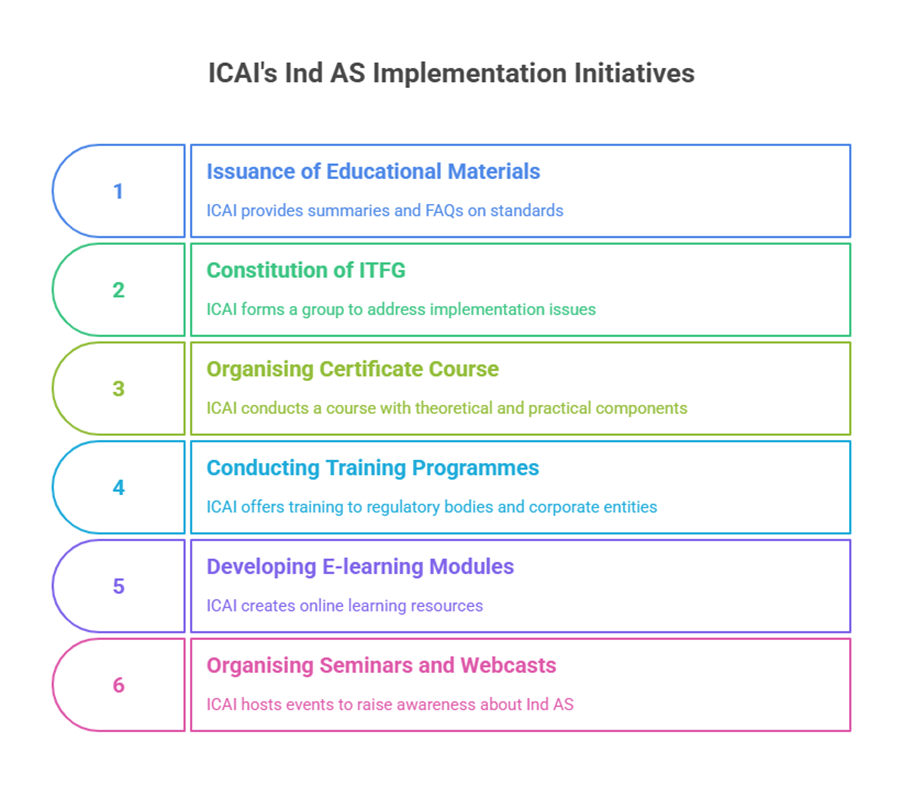

Ind AS Implementation Initiatives The ICAI is actively involved in initiatives to facilitate the implementation of Ind AS. These include:

- Issuance of Educational Materials covering summaries of standards and Frequently Asked Questions (FAQs). Educational materials on numerous standards have been issued.

- Constitution of the Ind AS Technical Facilitation Group (ITFG) to address implementation-related issues in a timely manner by issuing clarification bulletins. As of the publication date, 23 ITFG Clarification bulletins addressing 162 issues had been brought out.

- Organising an extensive Certificate Course on Ind AS. This course provides theoretical aspects and case studies and includes quarterly examinations.

- Conducting in-house training programmes on Ind AS for regulatory bodies (like C&AG, IRDAI, CBDT), other government departments, and corporate entities.

- Developing e-learning modules, and organising seminars, awareness programmes, and webcasts on Ind AS.

- Awareness programmes cover fundamental standards, consolidation, business combinations, financial instruments, revenue recognition, first-time adoption, and key differences between Ind AS and previous Accounting Standards (AS).

These initiatives demonstrate ICAI’s commitment to assisting stakeholders in understanding and applying Ind AS correctly, reflecting the spirit in which they were formulated.

List of Applicable Indian Accounting Standards The Quick Referencer includes a list of applicable Indian Accounting Standards. These are:

- Ind AS 101, First-time Adoption of Indian Accounting Standards

- Ind AS 102, Share-based Payment

- Ind AS 103, Business Combinations

- Ind AS 104, Insurance Contracts

- Ind AS 105, Non-current Assets Held for Sale and Discontinued Operations

- Ind AS 106, Exploration for and Evaluation of Mineral Resources

- Ind AS 107, Financial Instruments: Disclosures

- Ind AS 108, Operating Segments

- Ind AS 109, Financial Instruments

- Ind AS 110, Consolidated Financial Statements

- Ind AS 111, Joint Arrangements

- Ind AS 112, Disclosure of Interest in Other Entities

- Ind AS 113, Fair Value Measurement

- Ind AS 114, Regulatory Deferral Account

- Ind AS 115, Revenue from Contracts with Customers

- Ind AS 116, Leases

- Ind AS 1, Presentation of Financial Statements

- Ind AS 2, Inventories

- Ind AS 7, Statement of Cash Flows

- Ind AS 8, Accounting Policies, Changes in Accounting Estimates and Errors

- Ind AS 10, Events after the Reporting Period

- Ind AS 12, Income Taxes

- Ind AS 16, Property, Plant and Equipment

- Ind AS 19, Employee Benefits

- Ind AS 20, Accounting for Government Grants and Disclosure of Government Assistance

- Ind AS 21, The Effects of Changes in Foreign Exchange Rates

- Ind AS 23, Borrowing Costs

- Ind AS 24, Related Party Disclosures

- Ind AS 27, Separate Financial Statements

- Ind AS 28, Investments in Associates and Joint Ventures

- Ind AS 29, Financial Reporting in Hyperinflationary Economies

- Ind AS 32, Financial Instruments: Presentation

- Ind AS 33, Earnings per Share

- Ind AS 34, Interim Financial Reporting

- Ind AS 36, Impairment of Assets

- Ind AS 37, Provisions, Contingent Liabilities and Contingent Assets

- Ind AS 38, Intangible Assets

- Ind AS 40, Investment Property

- Ind AS 41, Agriculture

In summary, Ind ASs are a set of accounting standards converged with IFRS, implemented in India to enhance the quality and comparability of financial reporting. The ICAI plays a vital role in both their formulation and implementation, offering extensive resources and guidance to stakeholders. The standards cover a wide range of accounting topics, from fundamental principles of presentation and measurement to specific areas like financial instruments, business combinations, leases, and industry-specific activities.