The Indian Government Accounting Standard (IGAS) 1 concerning Disclosure Requirements relating to Guarantees given by Governments.

The notification announces the issuance of the Indian Government Accounting Standard (IGAS) 1. This standard focuses specifically on Disclosure Requirements relating to the form of accounts of the Union, States and Union Territory Governments (with legislature) concerning guarantees given by these governmental bodies.

Legal Basis and Authority

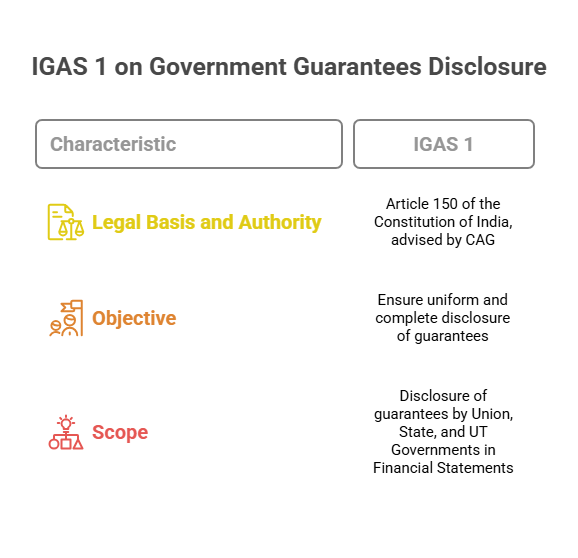

The power to issue this standard is drawn from exercise of the powers conferred by Article 150 of the Constitution of India. This Article relates to the form of accounts of the Union and of the States. The standard is issued on the advice of the Comptroller and Auditor General (CAG) of India. This highlights the role of the CAG in advising the President on the form of accounts, making this standard part of the prescribed accounting framework for Indian governments. The Hindi preamble also mentions the standard being issued under the authority of Article 150 of the Constitution and on the advice of the CAG, stating it aims to provide a comprehensive form of accounts.

Objective of IGAS 1

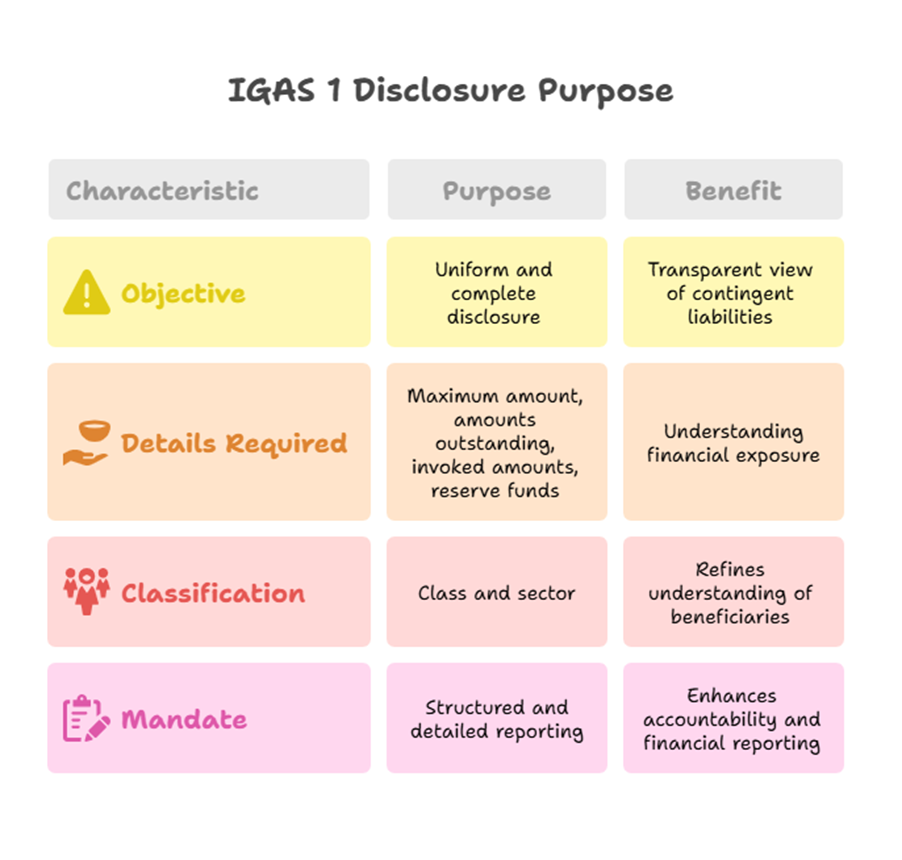

The objective of this Standard is explicitly stated. It is “to set out disclosure requirements in respect of guarantees given by the Union, the State Governments and Union Territory Governments (with legislature) in their respective Financial Statements to ensure uniform and complete disclosure of such Guarantees”. This underscores the standard’s purpose: to bring consistency and comprehensiveness to how governments report the guarantees they have issued in their official financial documents.

Scope of IGAS 1

The scope of this Standard is defined as requiring disclosure of information about guarantees given by the Union Government, the State Governments and Union Territory Governments (with legislature) in their Financial Statements. It clarifies that the Standard shall not be complied with for statements prepared for purposes other than the Financial Statements of these governments. The Standard also states that the Authority responsible for preparing and presenting the Financial Statements shall apply this Standard.

Definitions of Key Terms

The Standard provides specific definitions for several key terms used within it:

- Authority in the context of this Standard: This refers to the authority responsible for preparing the Financial Statements of the Government.

- Government in this Standard: This term refers to the Union Government, the State Governments and Union Territory Governments (with legislature).

- Automatic Debt Mechanism: This is defined as the arrangement whereby the Government’s cash balance on a specified date, or on the occurrence of specified events, is used to meet certain obligations arising out of a guarantee given by it. This implies a pre-arranged system for payment if the guarantee is invoked, directly linked to government funds.

- Financial Statements: This refers to the Annual Finance Accounts of the Government.

- Guarantee: This is defined as an accessary contract, meaning a contract related to another primary contract. It is one by which the promisor undertakes to be answerable to the promisee for the debt, default or miscarriage of another person, whose primary liability to the promisee must exist or be contemplated. In simpler terms, it’s a commitment by the government to cover the obligations of a third party if that party fails to meet them.

- Performance Guarantee: This type of guarantee is given to secure performance of an obligation.

- Structured Payment Arrangement: This is defined as the arrangement whereby the Government agrees to transfer funds to the designated account in case the beneficiary entity fails to ensure availability of adequate funds for servicing the debts, as per stipulations. This is similar to an Automatic Debt Mechanism but might involve a broader arrangement for funding the debt service.

Disclosure Requirements

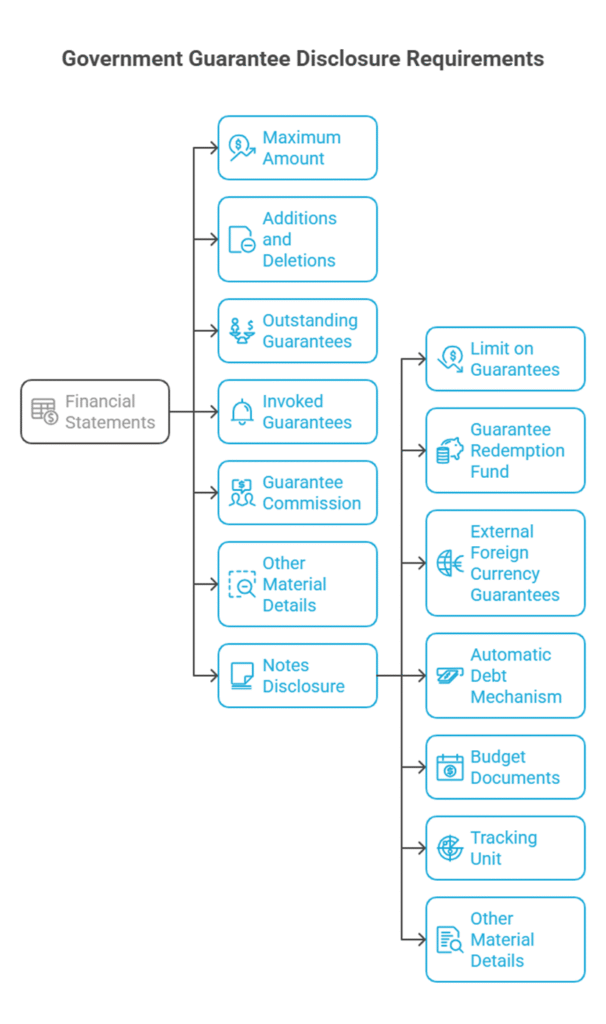

The Standard specifies that the Financial Statements of the Union Government, the State Governments, and the Union Territory Governments (with legislature) shall disclose the following details concerning class and sector of Guarantees in the format specified in paragraph M. The disclosures required include:

- Maximum amount for which Guarantees have been given during the year.

- Additions and deletions (other than invoked) during the year.

- Guarantees outstanding at the beginning and end of the year.

- Amount of Guarantees invoked and discharged or not discharged during the year.

- Details of Guarantee commission or fee and its realisation.

- Other material details.

Furthermore, the Financial Statements shall also disclose the following details in the notes:

- Limit, if any, fixed within which the Government may give Guarantee. This indicates any statutory or internal limits on the total value of guarantees a government can issue.

- Whether a Guarantee Redemption or Reserve Fund exists, and its details, including disclosure of balance available in the Fund at the beginning of the year, any payments made and balance at the end of the year. This is important for assessing the government’s provision for potential guarantee payouts.

- Details of subsisting external foreign currency guarantees in terms of Indian Rupees on the date of Financial Statements. This highlights foreign currency exposure arising from guarantees.

- Details concerning Automatic Debt Mechanism and Structured Payment Arrangement, if any.

- Whether the budget documents of the Government contain details of Guarantees. This links the financial reporting to the budget process.

- Details of the tracking unit or designated authority for Guarantees in the Government. This points to internal government processes for managing guarantees.

- Other material details.

The Hindi section also mentions that information about guarantees should be presented in the financial statements, including the total amount of guarantees, amounts added/deleted, outstanding balances, invoked amounts, commission details, and other important details. It also lists categories for disclosure similar to the English text, emphasizing disclosure in the notes, budget documents, and tracking mechanisms.

Data Collation and Tracking

The standard suggests how information for disclosure is gathered. In order to prepare a database, details for all guarantees annually sanctioned, annulled and outstanding, and tracking information for Guarantees is usually collated by the Ministry or Department of Finance in the respective Governments. The Financial Statements should disclose the tracking unit or designated authority for Guarantees or any concerned authority in charge of this responsibility.

Regarding tracking, the standard notes that when Guarantees are invoked and payments made, the payment is treated as loan to the beneficiary on whose behalf the Guarantee was given. Recoveries are also tracked. The expenditure, loan and recoveries are distinctly classified in the Financial Statements. If, in due course, the whole or part of the loan amount is finally held to be irrecoverable, it is adjusted in the manner specified.

The Hindi text also touches upon tracking, stating that the information regarding guarantees and recoveries is maintained.

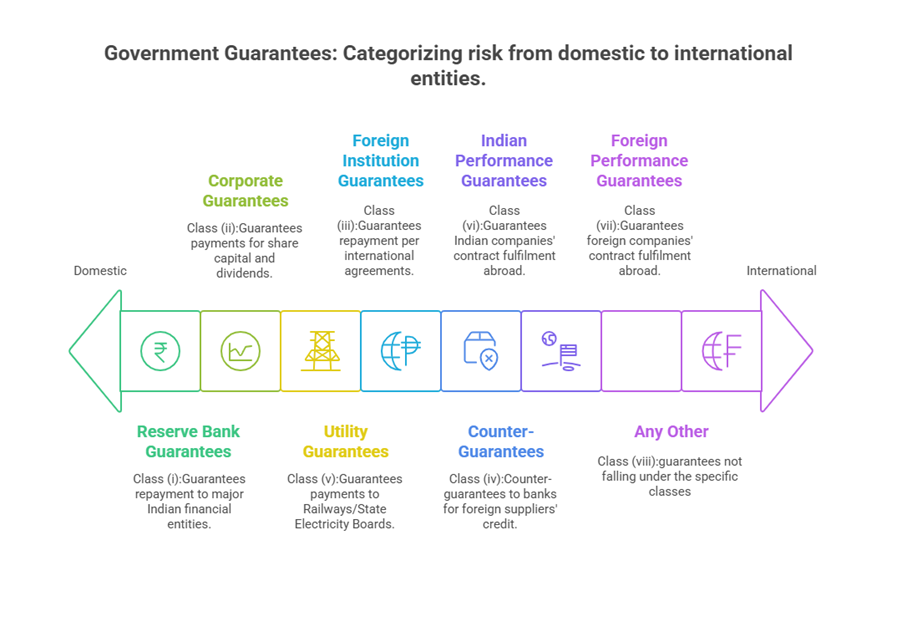

Categorization of Guarantees (Class and Sector)

To provide structured disclosure, the standard categorizes guarantees by Class and Sector. The classes of guarantees are listed as follows:

- Class (i): Guarantees given to the Reserve Bank of India, other banks and financial institutions for repayment of principal and payment of interest. This class includes guarantees for principal and interest payments on loans from major financial entities.

- Class (ii): Guarantees given to Corporations, companies, co-operative societies and banks for payment of share capital, payment of minimum annual dividend, payment against arrears of payment relating to bonds or loan debentures issued or raised by such entities. This covers guarantees related to capital structure, dividend payments, and bond/debenture obligations of various corporate and cooperative bodies.

- Class (iii): Guarantees given in pursuance of agreements entered into by the Government of India with international financial institutions, foreign lending agencies, foreign contractors, foreign suppliers and foreign consultants towards repayment of principal, payment of interest or commitment charges on loans and for payment against supplies of material or rendition of services rendered. This class deals with guarantees given specifically in the context of international borrowings, foreign contracts, and supplies.

- Class (iv): Counter-guarantees to banks in consideration of the banks having issued letters of credit to foreign suppliers for supplies made or services rendered. This is a specific type of guarantee where the government guarantees a bank that has itself issued a letter of credit for a foreign supplier.

- Class (v): Guarantees given to Railways/State Electricity Boards and other entities for due and punctual payment of dues by companies or corporations. This covers guarantees for payments owed to essential service providers like Railways and Electricity Boards.

- Class (vi): Performance guarantees given for fulfilment of contracts or projects awarded to Indian companies or corporations in foreign countries. These guarantees ensure that Indian entities undertaking work abroad fulfil their contractual obligations.

- Class (vii): Performance guarantees given for fulfilment of contracts or projects awarded to foreign companies or corporations in foreign countries. Similar to Class (vi), but for foreign entities working abroad.

- Class (viii): Any other. This serves as a residual category for guarantees not falling under the specific classes above.

The Sectors for which guarantees are disclosed are listed as:

- (i) Power

- (ii) Cooperative

- (iii) Irrigation

- (iv) Roads and Transport

- (v) State Financial Corporations

- (vi) Urban Development and Housing

- (vii) Other Infrastructure

- (viii) Any other

The Hindi section also lists similar categories of guarantees, including those for repayment of principal/interest for loans from banks and financial institutions, payment of share capital/dividends, guarantees for bonds/debentures, guarantees given under agreements with international bodies or foreign entities, counter-guarantees to banks, guarantees for dues to Railways/Electricity Boards, and performance guarantees for contracts abroad. The sectors listed in the Hindi text are also consistent, covering areas like Irrigation, Power, Transport, State Financial Corporations, Urban Development, etc..

Effective Date

This Indian Government Accounting Standard (IGAS) 1 became effective for class-wise disclosures in the Financial Statements of the Union Government and the State/UT Governments covering periods beginning on or after 1-4-2010. For sector-wise disclosures, the effective date is the same, covering periods beginning on or after 1-4-2010. This means the standard was applicable for the financial year 2010-2011 onwards.

Formats for Disclosure

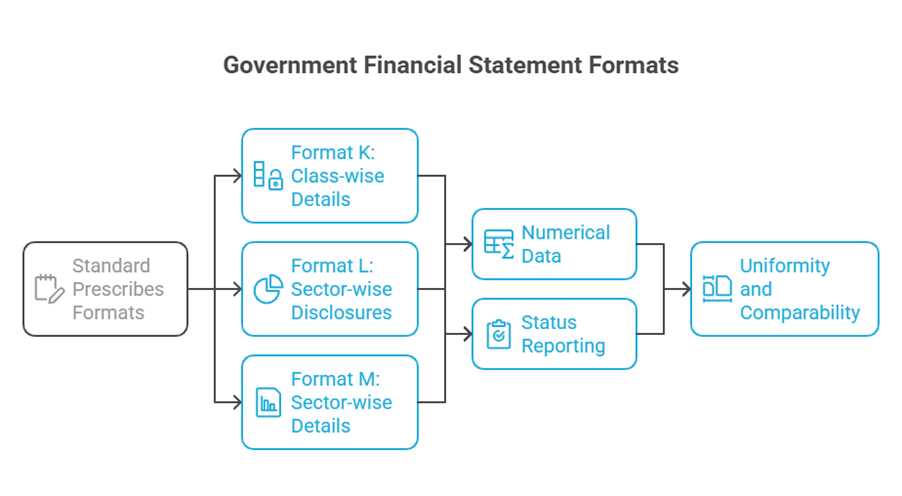

The Standard prescribes specific formats for both class-wise and sector-wise disclosures in the Financial Statements. These formats are crucial for ensuring uniformity and comparability across government financial statements.

Format K provides a table for Class-wise details for Guarantees. The columns in this table are:

- Column 1: Class (No. of Guarantees within bracket)

- Column 2: Maximum amount guaranteed during the year (Rs.)

- Column 3: Outstanding at the beginning of the year (Rs.)

- Column 4: Additions during the year (Rs.)

- Column 5: Deletions (other than invoked) during the year (Rs.)

- Column 6: Invoked during the year (Rs.)

- Column 7: Discharged / Not Discharged

- Column 8: Outstanding at the end of the year (Rs.)

- Column 9: Guarantee Commission or fee (Rs.) Receivable

- Column 10: Guarantee Commission or fee (Rs.) Received

- Column 11: Other material details

This format requires reporting numerical data (amounts, counts) and status (Discharged/Not Discharged) for each class of guarantee across the financial year.

Format L and Format M provide similar detailed tables, but Format L is for Sector-wise disclosures for each Class for Guarantees, and Format M is for Sector-wise details for Guarantees. The columns in Format L and M are identical to Format K, allowing for the same detailed breakdown of guarantees first by class and then by the sector they relate to, or directly by sector. This structured approach allows users of the financial statements to understand the distribution of guarantee liabilities across different types of beneficiaries and economic activities. The Hindi section also shows similar tabular formats for presenting guarantee information class-wise and sector-wise.

The Hindi introduction mentions that the rules for the format of accounts provided through this notification should be followed by the Union, State, and Union Territory Governments. It further states that this standard (IGAS-1) aims to clarify the form of accounts for government guarantees.

Purpose of Disclosure

While the objective is uniform and complete disclosure, the underlying purpose is to provide a transparent view of the government’s contingent liabilities arising from guarantees. Guarantees represent potential future obligations that could require government expenditure if the primary debtor defaults. By requiring detailed disclosure, IGAS 1 helps users of government financial statements assess the magnitude, nature, and potential risk associated with these off-balance sheet commitments. The details required, such as the maximum amount guaranteed, amounts outstanding, invoked amounts, and the existence of reserve funds, are all relevant for understanding the financial exposure. The classification by class and sector further refines this understanding by showing which types of entities or activities are the primary beneficiaries of government guarantees.

In essence, IGAS 1 mandates a structured and detailed reporting mechanism for government guarantees, transforming these potential liabilities into transparent information within the Financial Statements and their notes. This enhances the accountability and financial reporting quality of the Union, State, and Union Territory Governments in India.