Loan financing is presented as an important mode of finance raised by a company. Among the various types of loan financing, a significant source of debt financing for corporates is the syndicated loan.

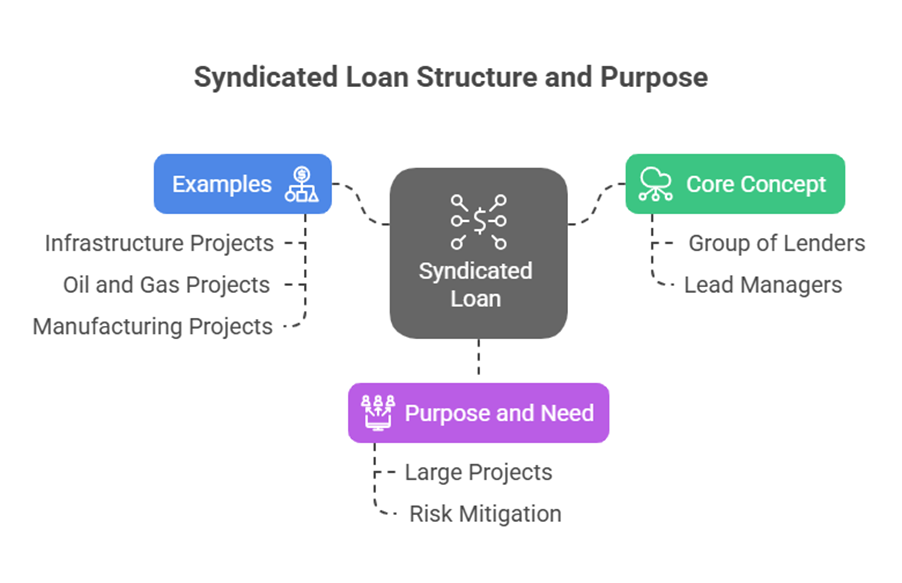

Core Concept and Definition

A syndicated loan is essentially a loan that is availed from a group of lenders. This group of lenders constitutes a ‘Syndicate’ to offer the loan facility. Syndicated bank loans are described as one of the ways of raising large loans from banks for companies with good credit ratings. This structure involves a number of other banks participating in the loan arrangement. It is arranged by one or more lead managers (banks).

In simpler terms, Loan Syndication is a process where a single large loan for a borrower is provided by multiple lenders acting together.

Purpose and Need

The primary need for loan syndication arises when a project is unusually large or complex, potentially exceeding the capacity of a single lender. This can happen if the amount of the loan required is too large for one institution to provide alone, or if the risks involved are too high for a single entity to bear entirely. Additionally, the collateral for the loan might be spread across different locations, or the specific uses of the capital may require specialized expertise to understand and manage, necessitating the involvement of multiple lenders with different areas of focus or capacity.

Syndicated loans provide funding for large-scale, capital-intensive projects. Examples given include infrastructure projects, oil and gas projects, and manufacturing projects. Banks participate in these transactions not only to provide the necessary large funding but also to ensure risk mitigation and manage large exposure.

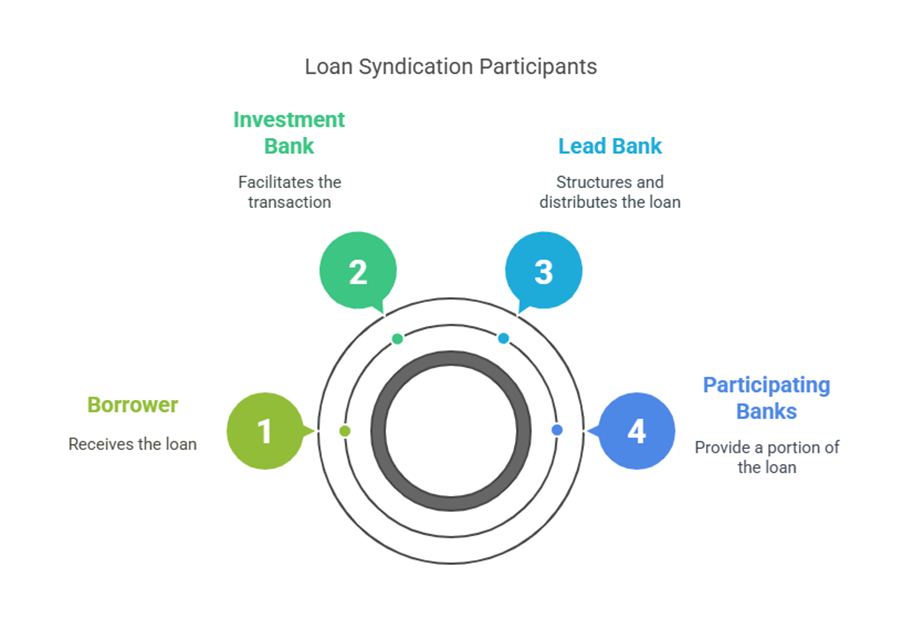

Key Participants

According to the sources, the main parties involved in a loan syndication are:

- Borrower: The company or entity receiving the loan.

- Investment Bank: Acts as a facilitator in the loan transaction.

- Lead Bank (or Lead Manager/Arranger): This entity is responsible for structuring the loan transaction. One, two, or even three banks may act as lead managers and distribute the loan among themselves and other participating banks.

- Participating Banks: These are the other lenders who lend some part of the total loan amount. The group of commercial banks, Government Funding Institutions, International banks, and Non-banking Finance Companies (NBFCs) etc., can form the ‘Syndicate’.

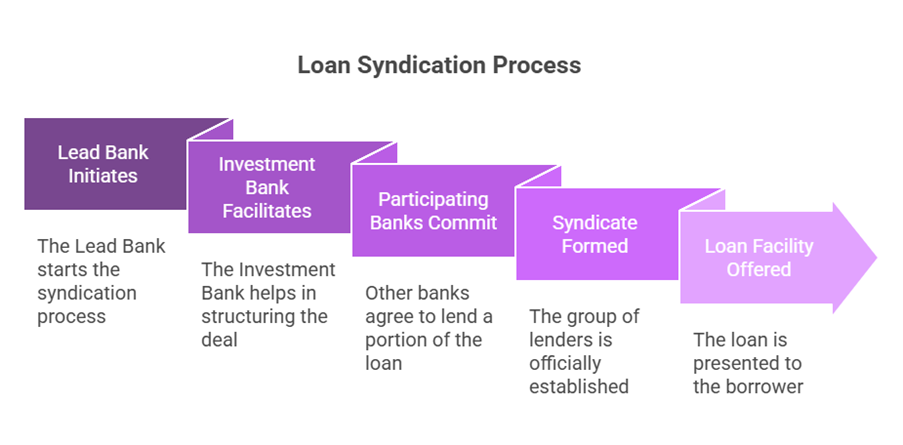

Process and Mechanism

The process involves a financial institution bringing other lenders into the deal when a project’s size or complexity exceeds its individual capacity. The Lead Bank is responsible for structuring the transaction. The investment bank facilitates the process. Participating banks commit to lending a portion of the total loan amount.

Loan syndications involve a large amount of coordination and negotiation among the various parties. Once the syndicate is formed, the loan facility is offered to the borrower.

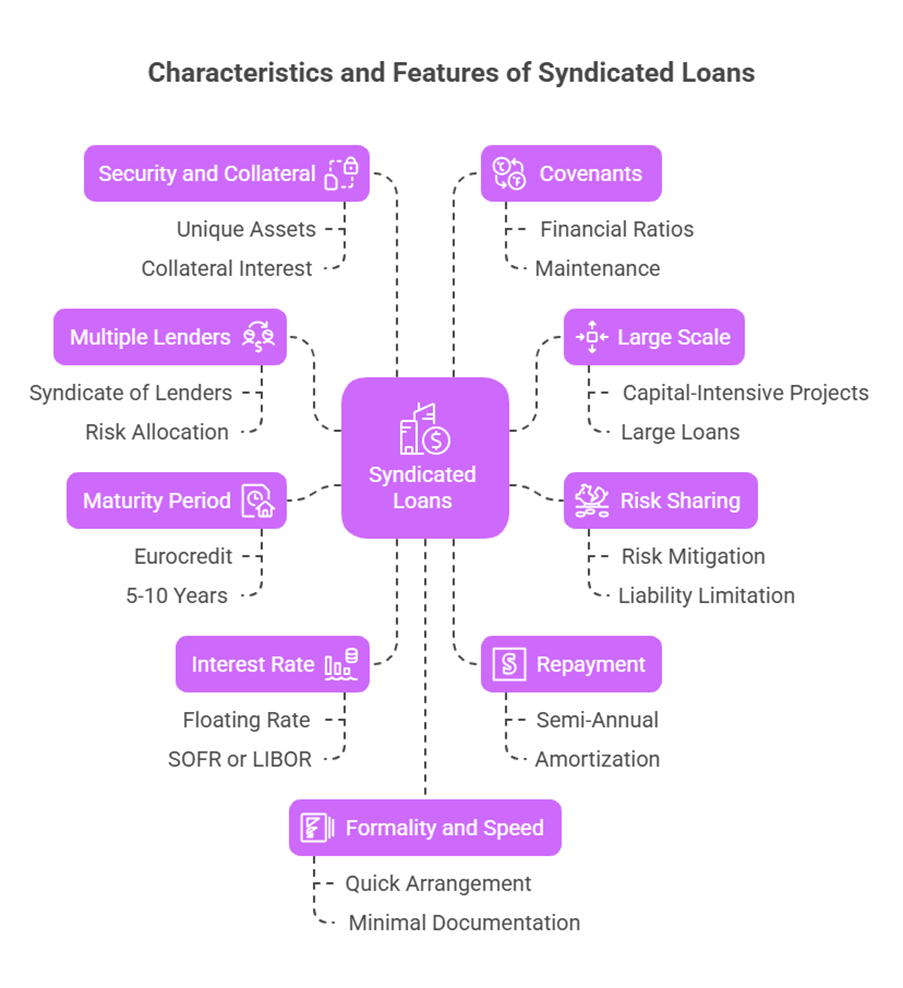

Characteristics and Features

Syndicated loans have several defining characteristics:

- Multiple Lenders: The defining feature is the involvement of a group or syndicate of lenders.

- Large Scale: They are used for large-scale, capital-intensive projects and represent large loans.

- Risk Sharing: By involving multiple lenders, the risk is allocated among different companies. This limits the liability of each lender to its share of the loan interest. This also helps banks with risk mitigation and managing large exposures.

- Maturity Period: While short-term finance like Commercial Paper typically has a maturity of less than one year, syndicated bank loans usually have a longer maturity. A typical Eurocredit, which is a form of syndicated credit, can have a maturity between five and 10 years. Another source mentions the maturity of syndicated bank loans can be for a duration of 5 to 10 years.

- Interest Rate: Interest rates on syndicated loans are generally floating rate. The interest rate is typically set with reference to an index, such as SOFR or LIBOR, plus a spread. This spread depends upon the credit rating of the borrower. Interest rates might be reset periodically (e.g., every three or six months with reference to LIBOR).

- Repayment: Amortization is often structured in semi annual instalments.

- Security and Collateral: While not explicitly detailed for all syndicated loans, it’s mentioned that each lender in a syndication might have a collateral interest in a unique or specialized asset from the borrower, such as a piece of equipment.

- Covenants: Lending institutions may lay down certain covenants for the borrower, such as the maintenance of key financial ratios.

- Formality and Speed: One source states that syndicated bank loans can be arranged in reasonably short time and with few formalities. Another, when discussing Euro notes (a type of Euro note that is distinct from syndicated bank credit and Eurobonds), mentions minimal documentation formalities unlike in the case of syndicated credits or bond issues. This might seem contradictory to the note about large amounts of coordination and negotiation. However, “few formalities” or “minimal documentation formalities” could be relative comparisons (e.g., compared to a public bond issue) or refer to specific aspects of the process, while the overall coordination among the syndicate members remains complex.

- Cost/Fees: Loan syndication fees can be expensive, ranging from 5% to 10% of the loan principal.

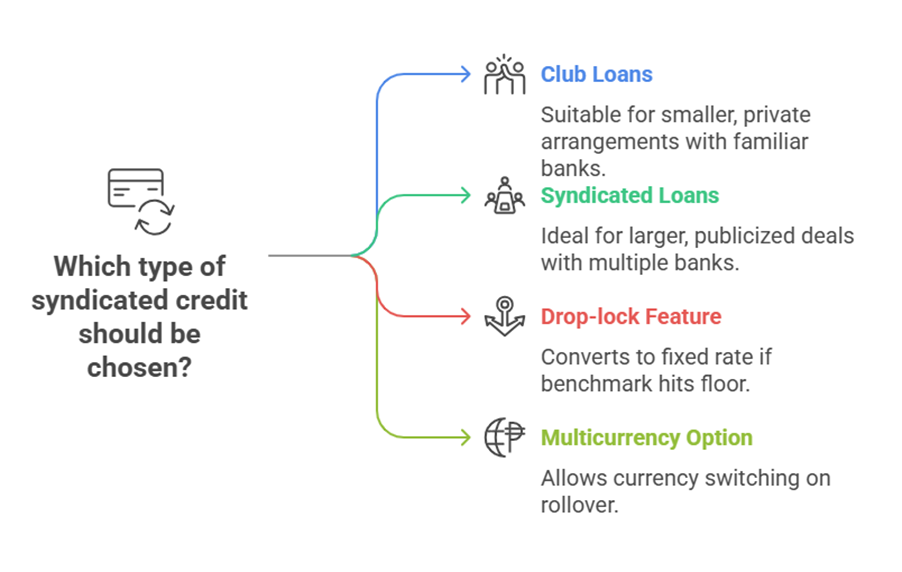

Types of Syndicated Credits

Within the broader category of syndicated credits, sources mention a distinction:

- Club Loans: This is a private arrangement between the lending banks and a borrower. They are typically used when the loan amounts are relatively small and the parties involved are familiar with each other. Unlike larger syndicated deals, club loans are conventionally not publicized in the financial press, and an information memorandum is not compiled.

- Syndicated Loans (in contrast to Club Loans): These represent the more formal, often larger and publicized arrangements involving lead managers and a syndicate of participating banks, as described above.

Potential Options within Syndicated Credits

Syndicated credits can be structured to include various options:

- Drop-lock feature: This option converts the floating rate loan into a fixed rate loan if a specified benchmark index hits a certain floor level.

- Multicurrency option: This allows the borrower to switch the currency in which the loan is denominated on a rollover date.

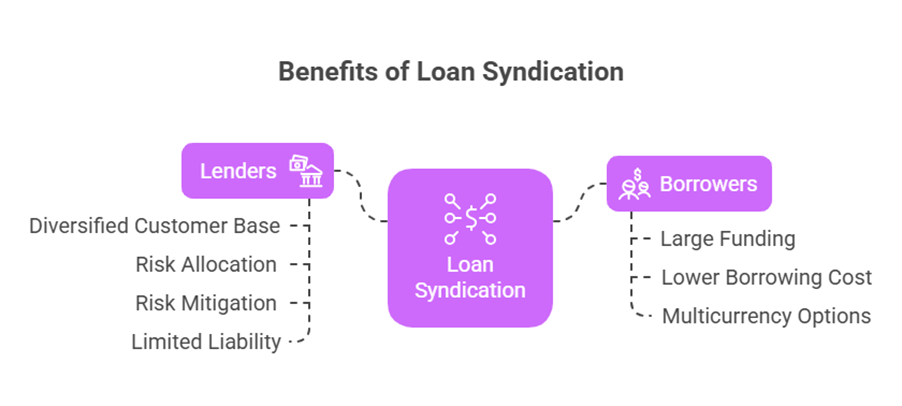

Benefits

Loan syndication offers benefits for both borrowers and lenders:

- For Borrowers:

- Large funding is possible as funding is sourced from multiple providers. This allows financing for projects that a single lender could not support.

- The total cost of borrowing is stated as being less. This might refer to the overall cost compared to arranging multiple individual loans, despite potentially high upfront fees.

- Access to multicurrency options and drop-lock features may be available.

- For Lenders:

- Diversified customer base.

- Risk allocation among different companies (spreading the risk).

- Risk mitigation and management of large exposure are key reasons banks participate.

- Liability is limited to their share of the loan interest.

In summary, Loan Syndication is a crucial mechanism for financing large and complex corporate projects by pooling funds and sharing risk among a group of lenders. While involving significant coordination and potentially high fees, it provides access to substantial capital and offers benefits to both borrowers and participating financial institutions.