Mutual Funds are a significant part of the financial services sector, particularly in India, offering a way for individuals to invest in capital markets. A mutual fund is structured as a trust that pools the savings of many investors who share a common financial goal. The money collected is then invested by professional money managers in various securities, such as stocks, bonds, and other instruments, according to the scheme’s stated investment objectives. Any income earned or capital appreciation realized from these investments is shared among the unit holders in proportion to the units they own. This makes mutual funds a suitable investment vehicle for both common individuals with small savings and High Net-worth Individuals (HNIs), providing access to a diversified, professionally managed portfolio at a relatively low cost.

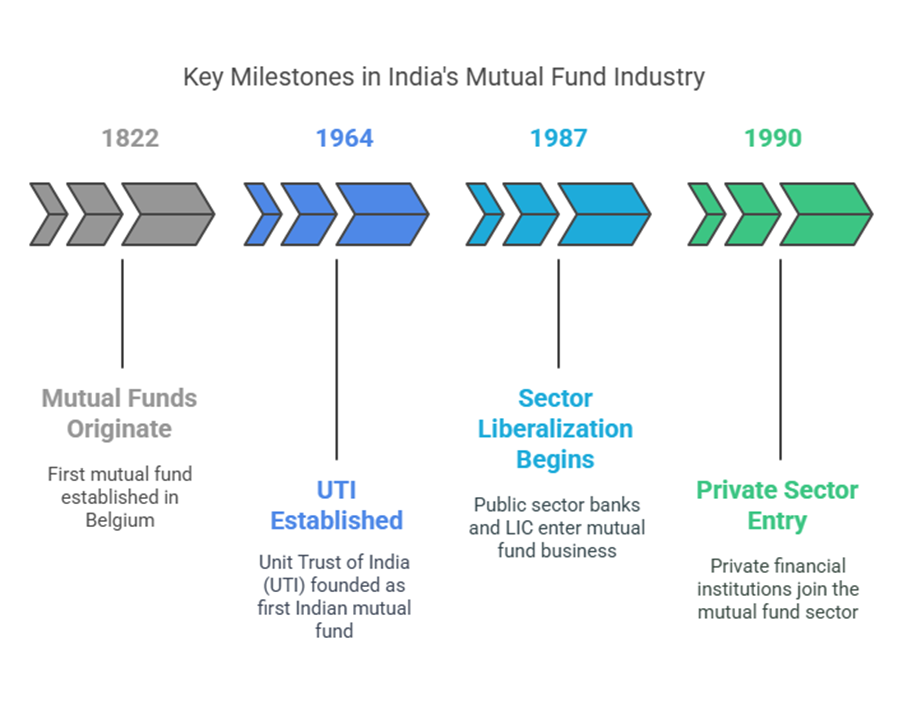

The concept of mutual funds originated in Belgium in 1822. In India, the first mutual fund, Unit Trust of India (UTI), was established in 1964 as a public sector institution by the central government. UTI held a monopoly in the mutual fund sector until 1987. After 1987, public sector commercial banks and the Life Insurance Corporation of India (LIC) also entered the mutual fund business, followed by private sector financial institutions from 1990 onwards.

The structure of the mutual fund sector in India involves SEBI overseeing the Mutual Fund Association, which includes entities like the Sponsor, Board of Trustee, Custodian, and the Investor. SEBI (Securities Exchange Board of India) is the primary regulatory body, under whose regulations mutual funds must be registered and operate. SEBI regulations stipulate that mutual funds must be formed as trusts and managed by a separate Asset Management Company (AMC) overseen by a board of trustees. The assets of a scheme are held by the Custodian. AMCs manage the investments and handle day-to-day operations, requiring a minimum net worth. Distributors also play a role by bringing investors to schemes and earning commission.

Mutual funds are classified in several ways based on their characteristics:

- By Ownership:

- Public Sector MFs: Sponsored by public sector companies or banks. Examples include UTI, SBI, Canara Bank, Punjab National Bank, and General Insurance Corporation.

- Private Sector MFs: Sponsored by private sector companies. Examples include Kothari Pioneer mutual fund, Twentieth century mutual fund, ICKI mutual fund, Morgan Stanly mutual fund, Taurus mutual fund, and CRB mutual fund. There are also Foreign Mutual Funds sponsored by foreign companies operating in India.

- By Scheme of Operation (Functional Classification):

- Open-Ended Mutual Funds: Units can be bought and sold on an ongoing basis at a price determined by the fund’s Net Asset Value (NAV). They have no fixed maturity period, no ceiling on investment amount, and investors can sell units back to the fund at any time. These funds need to maintain a portion of their capital in liquid assets to facilitate repurchases.

- Closed-Ended Mutual Funds: Have a fixed maturity period, typically ranging from two to 15 years. Units are generally not repurchased or redeemed by the fund before maturity. After the initial offering period, investors cannot buy units directly from the fund. Liquidity is usually provided by listing units on the stock exchange.

- Interval Funds: Combine features of both open-ended and closed-ended funds. They are not required to be listed and have in-built redemption windows, allowing fresh unit issues during specified intervals at NAV-based prices.

- By Portfolio Basis:

- Growth Generated Mutual Funds: Invest in highly growth-oriented equity shares, aiming for high returns with growth potential.

- Income Generated Mutual Funds: Focus on providing regular income to investors.

- Balanced Mutual Funds: Combine investments in company securities and government bonds, aiming for moderate returns with safety options. They typically maintain a mix of equity and debt instruments.

- Other Portfolio types include Equity Funds (primarily stocks), Debt Funds (income securities like bonds), and various Special Funds like Index Funds (track market indexes), International Funds (invest globally), Offshore Funds (located outside India, invest in India), Sector Funds (specialize in a particular industry/sector), Money Market Funds (invest in short-term instruments like Treasury Bills, Commercial Papers, Certificate of Deposits, aiming for capital preservation, liquidity, and moderate income), Fund of Funds (invest in other mutual fund schemes), Gold Funds (track gold performance, often ETFs), Quant Funds (use data-driven stock selection), Diversified Equity Funds (hold a wide array of stocks, reducing concentration risk), Flexi cap Funds (invest across market caps without restriction), Multicap Funds (mandated minimum investment in large, mid, and small cap stocks), Contra Funds (invest in undervalued companies), Dividend Yield Funds (invest in high dividend yield stocks), Cash Funds (short-dated debt/money market instruments for low volatility, high liquidity), and Fixed Maturity Plans (FMPs – closed-ended, invest in debt/money market instruments for a fixed period).

- By Location Point of View: Domestic Mutual Fund (mobilizes savings from a particular country), Global Mutual Fund (invests in markets worldwide), Regional Mutual Fund (focuses on a particular region or country, also called offshore), and Sector Mutual Fund (specializes in an industry).

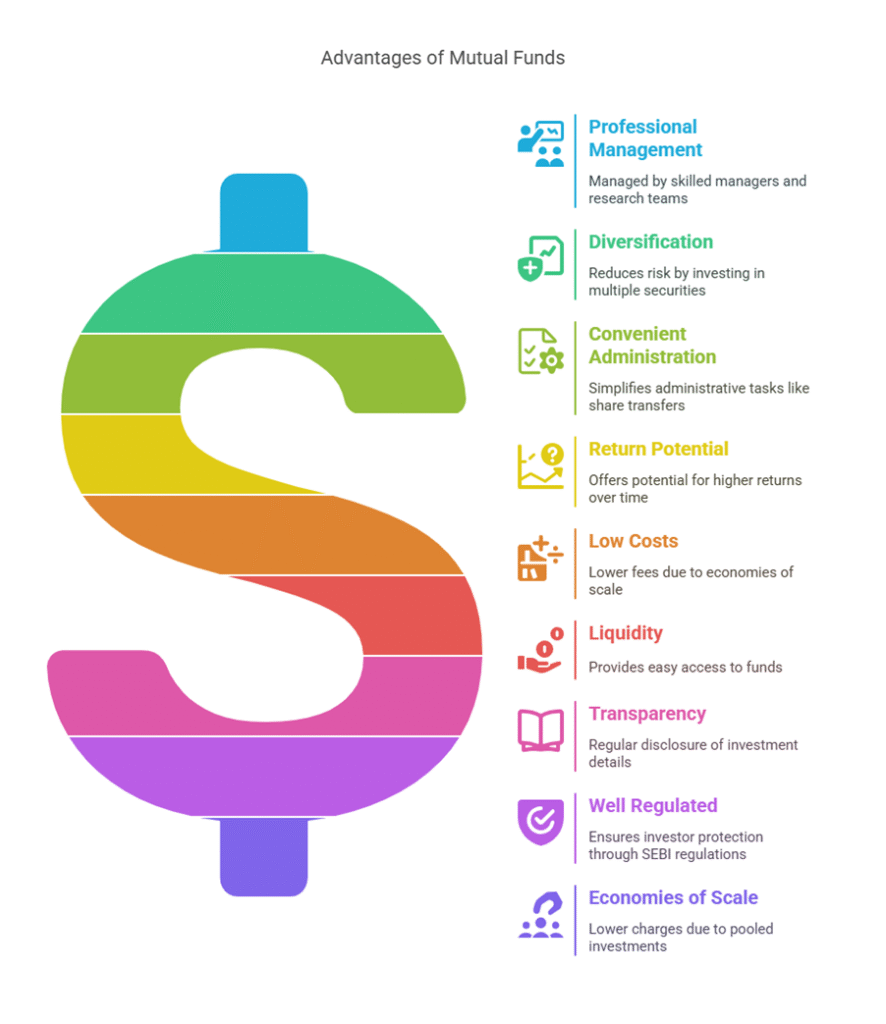

Mutual Funds offer several advantages:

- Professional Management: Funds are managed by skilled and experienced managers supported by research teams.

- Diversification: Investing in many securities across industries reduces concentration risk.

- Convenient Administration: Reduces administrative burdens like share transfer issues, saving time.

- Return Potential: Can potentially offer higher returns over medium to long terms compared to other avenues.

- Low Costs: Brokerage and other fees are relatively lower than direct market investment due to economies of scale.

- Liquidity: Open-ended funds offer liquidity through direct sale/repurchase, while closed-ended funds may be listed on stock exchanges or offer periodic repurchase facilities.

- Transparency: Mutual fund companies regularly disclose investment values, portfolio holdings, asset allocation, strategy, and outlook.

- Well Regulated: In India, they are highly regulated by SEBI, ensuring investor protection.

- Economies of Scale: Pooled money from numerous investors allows for lower charges compared to direct investment.

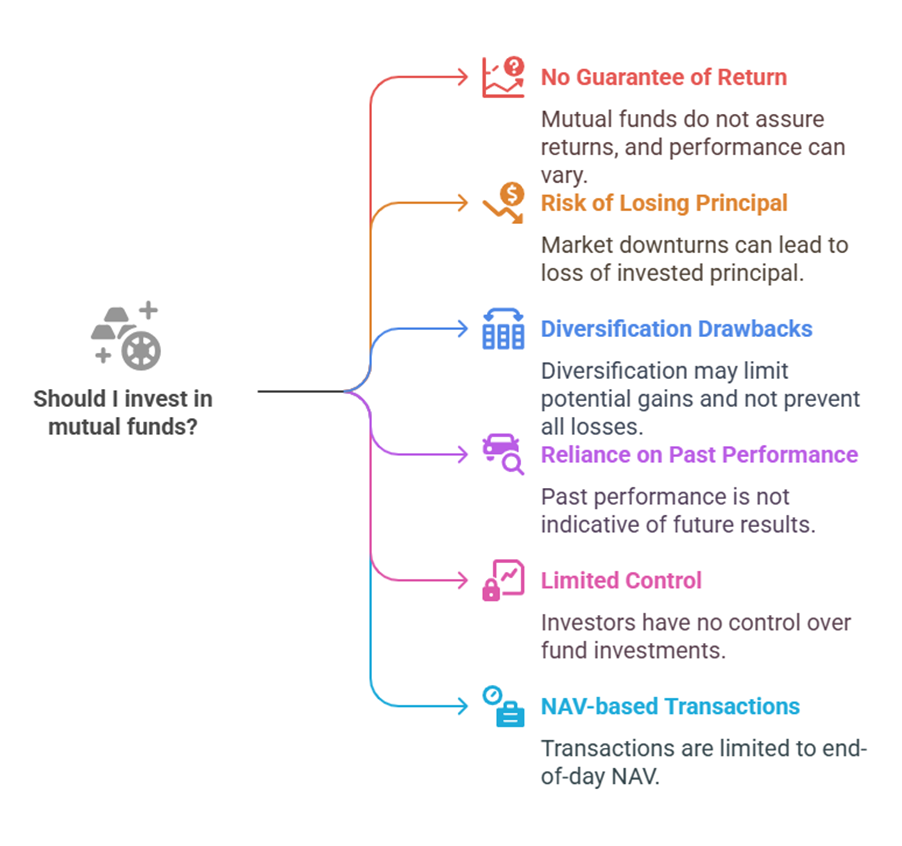

However, mutual funds also have potential drawbacks:

- No Guarantee of Return: Not all funds perform well, and there is no assurance of returns.

- Risk of Losing Principal: In significant market downturns, investors may lose their principal in the short term.

- Diversification Drawbacks: While reducing risk, diversification might limit potential gains compared to a single high-performing stock. It doesn’t protect against all losses during market turmoil.

- Reliance on Past Performance: Using past performance to select a fund does not guarantee future returns.

- Limited Control: Investors have no say in the specific securities the fund invests in.

- NAV-based Transactions: Open-ended funds typically cannot be bought or sold during the trading day but only at the end of the day based on the declared NAV.

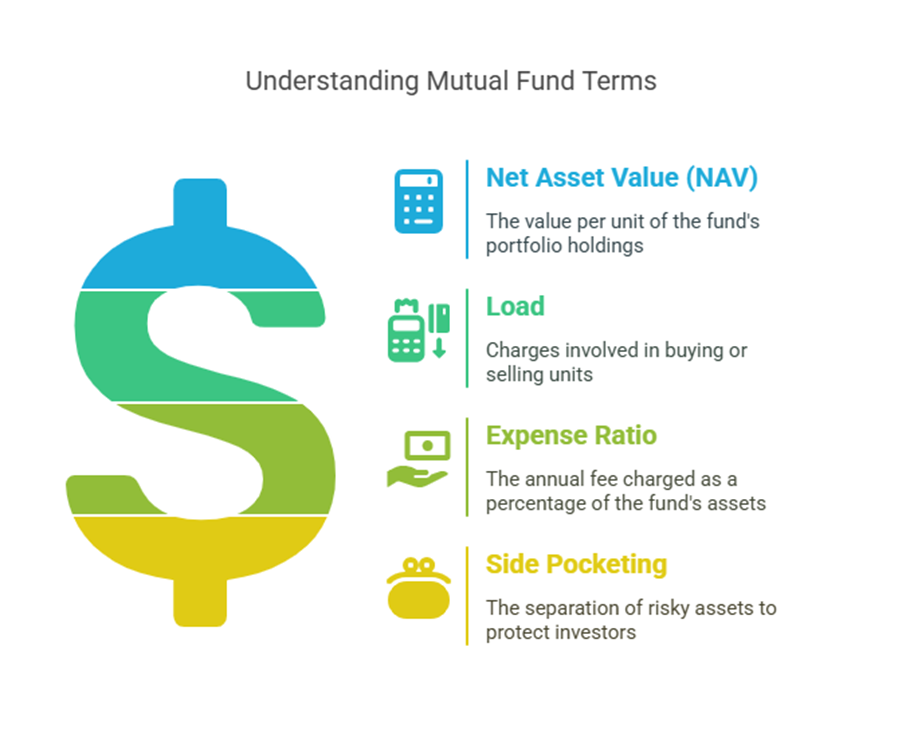

Key terms associated with mutual funds include:

- Net Asset Value (NAV): The value per unit of the fund’s portfolio holdings. It is calculated by dividing the net assets value of the fund by the number of outstanding units. Net assets value is the market value of investments plus receivables and accrued income, minus liabilities and accrued expenses. NAV is disclosed daily for most schemes. The price at which units are bought or sold by investors is often based on NAV.

- Load: Charges involved in buying or selling units. Front-end load is charged at the time of purchase, while back-end load is charged at the time of redemption.

- Expense Ratio: The annual fee charged as a percentage of the fund’s assets to cover operating expenses. A high expense ratio can negatively impact a fund’s performance.

- Side Pocketing: The separation of risky or doubtful assets from other investments to protect investors’ money linked to stressed assets and avoid distress selling.

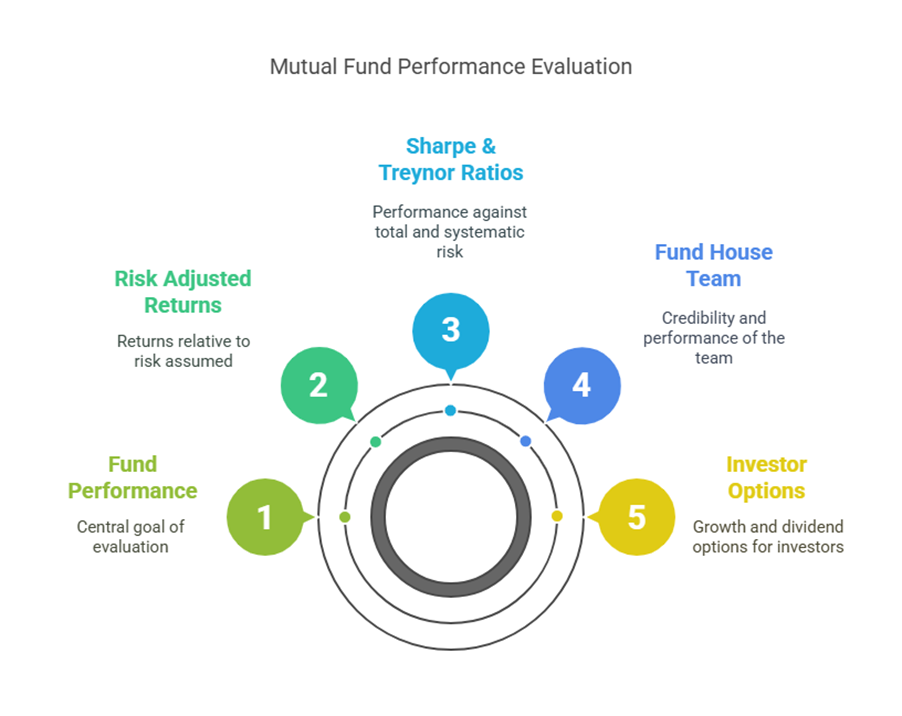

Evaluating mutual fund performance involves both quantitative and qualitative parameters. Quantitative measures include:

- Risk Adjusted Returns: Evaluating returns relative to the risk assumed.

- Benchmark Returns (Alpha): Measuring how well a fund performs compared to a benchmark index. Alpha is the excess return above the benchmark.

- Sharpe Ratio: Measures a fund’s performance based on total risk (systematic and unsystematic), calculated as the portfolio return in excess of the risk-free rate divided by the standard deviation.

- Treynor Ratio: Measures a fund’s performance against systematic risk (Beta), calculated as the portfolio return in excess of the risk-free rate divided by the portfolio Beta.

Qualitative evaluation factors include the credibility and performance of the fund house team, who handle investment decisions and administrative tasks like redemption and providing information.

Fund managers are responsible for ensuring good fund performance, selecting securities, and continuously monitoring the portfolio. They also ensure compliance with regulations from bodies like SEBI and AMFI. Foreign Institutional Investors (FIIs), which are large foreign groups, also invest in mutual funds and the equity market, influencing market sentiment.

Mutual funds also offer different options to investors, such as the Growth option where profits are reinvested, ideal for long-term goals, and the Dividend option (including dividend pay-out), where realized profits are distributed periodically, suitable for investors seeking regular income.

Overall, mutual funds provide a structured and regulated way for investors, particularly small ones, to participate in capital markets, offering potential benefits like diversification and professional management, though they come with inherent market risks and no guaranteed returns.