Introduction to Financial Institutions

In today’s financial services marketplace, a financial institution exists primarily to provide a wide variety of deposit, lending, and investment products to individuals, businesses, or both. They are defined as intermediaries that mobilize savings and facilitate the allocation of funds in an efficient manner. Financial institutions are business organisations that act as mobilisers of savings and as purveyors of credit or finance, also providing various financial services to the community.

Financial institutions can be classified into banking institutions and non-banking institutions. Banking institutions are creators of credit, participating in the economy’s payment system and providing transaction services, with their deposit liabilities forming a major part of the national money supply. Non-banking financial institutions, conversely, act as mere purveyors of credit and do not create credit.

They can also be classified as financial intermediaries and non-financial intermediaries. Financial intermediaries stand between savers and investors, lending money and mobilizing savings, with liabilities towards ultimate savers and assets from investors or borrowers.

Types of Financial Institutions Covered in the Sources

The sources discuss various types of financial institutions, highlighting their roles and characteristics:

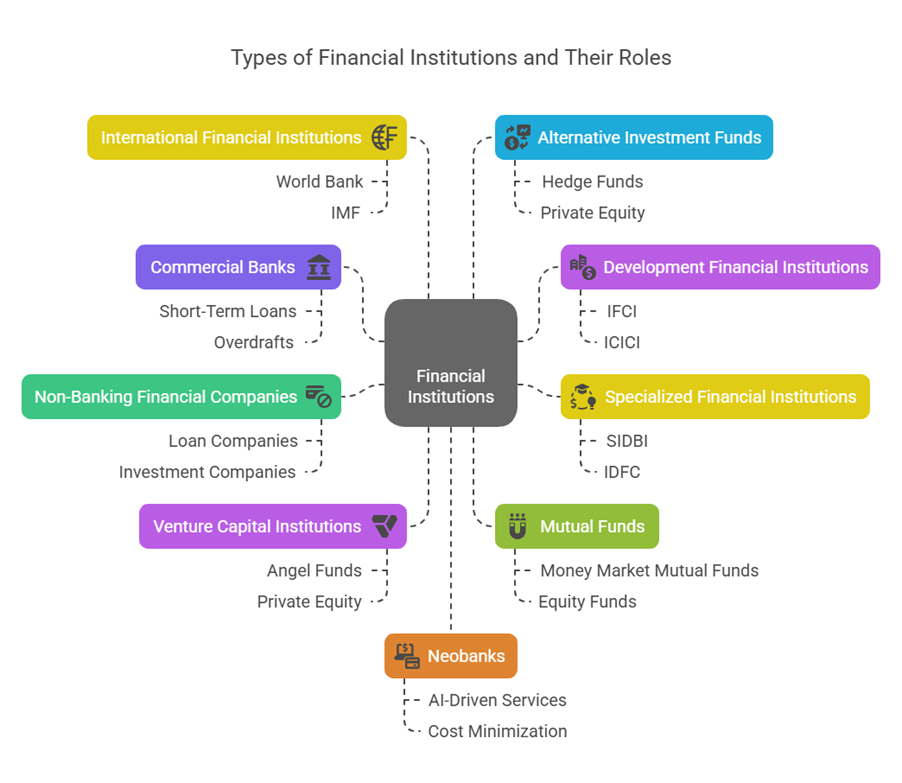

- Commercial Banks:

- Normally provide short-term finance, repayable within a year.

- Their major finance includes short-term advances, used to meet working capital requirements. This is described as a cheap source of finance.

- Traditionally served businesses, but currently, large banks offer deposit accounts, lending, and financial advice to both individuals and businesses.

- While their primary role is catering to short-term requirements, they have started taking interest in long-term financing.

- Specific facilities provided include Short Term Loans, Overdrafts/Cash Credit (allowing withdrawals up to a limit), Clean Overdrafts (for financially sound parties with good reputation), and Advances against goods (using pledge or hypothecation).

- Commercial banks are banking institutions and are considered “creators” of credit.

- They receive deposits from the public at varying rates and periods, which are then invested and lent.

- They can issue Certificates of Deposit (CDs).

- Commercial banks, including Foreign Banks, are participants in the Call Money Market.

- Scheduled banks can act as Issuing and Paying Agents (IPA) for Commercial Paper (CP).

- They provide working capital finance, Line of Credit, Letter of Credit, and Bank Guarantees.

- Development Financial Institutions (DFIs):

- Established nationwide and state-wise by the government to provide long-term financial assistance to industrial concerns.

- They play a key role in industrial development.

- Examples include IFCI, ICICI, IDBI, SFC (State Financial Corporations), EXIM Bank, IRBI, NABARD, UTI, LIC, GIC.

- Some have been converted into banks or privatized (e.g., IFCI, ICICI, IDBI).

- They were set up to meet the medium and long-term requirements of industry, trade, and agriculture. They are classified as term-finance institutions.

- Functions include granting loans and advances for establishing, expanding, diversifying, and modernizing industries. They can guarantee loans raised by industrial concerns and subscribe to or underwrite the issue of shares and debentures. They also provide consultancy, merchant banking, technical, legal, marketing, and administrative assistance.

- State Financial Corporations (SFCs) were established to meet the financial needs of small and medium-sized enterprises, which were initially outside IFCI’s purview.

- All India Financial Institutions are permitted participants in the Call Money Market and are allowed to issue Commercial Paper.

- LIC and GIC also provide short-term loans to manufacturing companies.

- Specialized Financial Institutions:

- Established by the government to provide financial and non-financial assistance to various specific industrial sectors in India.

- Examples include SCICI (Shipping Credit), IL&FS (Infrastructure Leasing), TDICI (Technology Development), RCTFC (Risk Capital and Technology Finance), TFCI (Tourism Finance), SIDBI (Small Industries Development Bank of India), and IDFC (Infrastructure Development Finance Company).

- SIDBI is mentioned as managing the Fund of Funds for Start-ups (FFS), which provides capital to SEBI-registered Alternative Investment Funds (AIFs) that invest in start-ups.

- Non-Banking Financial Companies (NBFCs):

- Considered non-banking financial institutions, meaning they act as purveyors of credit but do not create credit.

- Defined as financial institutions or non-banking institutions that receive deposits or lend.

- Types include loan companies, investment companies, hire purchase finance companies, equipment leasing companies, and mutual benefit finance companies.

- NBFCs are categorized by liabilities (deposit/non-deposit), size (systemically important/other), and activity.

- Specific types mentioned are Asset Finance Company (AFC), Investment Company (IC), Loan Company (LC), Infrastructure Finance Company (IFC), Systemically Important Core Investment Company (CIC-ND-SI), Infrastructure Debt Fund (IDF-NBFC), Micro Finance Institution (NBFC-MFI), Mortgage Guarantee Companies (MGC), and Non-Operative Financial Holding Company (NOFHC).

- Key differences from banks include not accepting demand deposits, not being part of the payment and settlement system (cannot issue cheques drawn on themselves), and the absence of Deposit Insurance and Credit Guarantee Corporation facility for depositors.

- NBFCs require registration with the RBI. Those registered with RBI can trade in Government securities.

- Other non-bank financial intermediaries are mentioned as part of the unorganized money market segment, including Indigenous Bankers (IBs), Chit Funds, and Nidhis. Indigenous bankers receive deposits and give loans but are unsupervised and unregulated, with their significance declining. Chit funds and Nidhis operate like mutual benefit schemes for members. Chit funds are popular in Kerala and Tamil Nadu, with RBI having no control over their lending.

- Venture Capital Institutions/Funds:

- Presented as a new type of financial intermediary emerging in India during the 1980s.

- They provide long-term financial assistance to projects establishing new products, inventions, ideas, and technology.

- Venture capital finance is suitable for risk-oriented businesses with huge investment that provide results after 5 to 7 years.

- It refers to financing new high-risk ventures promoted by qualified entrepreneurs who lack experience and funds.

- Venture Capital Financing is listed as a Fee Based Financial Service.

- Venture Capital is also listed under the umbrella of Alternative Investment Funds (AIFs). Angel Funds, a type of AIF, invest in venture capital undertakings meeting specific criteria regarding incorporation age and turnover.

- IDBI’s VCF provides funding for the commercial application of indigenous technology.

- SIDBI manages the Fund of Funds for Start-ups (FFS) which provides capital to SEBI-registered AIFs, including potentially venture capital funds, for investment in start-ups.

- Mutual Funds:

- Act as financial intermediaries helping to mobilize savings and supply funds to the capital market.

- A scheme for Money Market Mutual Funds (MMMFs) was introduced by RBI in 1992 to provide a short-term avenue for individual investors. Banks, public financial institutions, and private sector institutions can set up MMMFs, which are now under SEBI regulations.

- They mobilize significant resources.

- Foreign Institutional Investors (FIIs) invest in mutual funds.

- Mutual funds are listed as a Fee Based Financial Service.

- The sources discuss their classification, types of schemes, advantages, drawbacks, terms, and evaluation.

- Various entities are involved in mutual fund operations.

- Mutual funds can invest in short-term deposits of Scheduled Commercial Banks.

- There are restrictions and conditions on investments made by mutual funds.

- International Financial Institutions (IFIs):

- Financial institutions established by more than one country, subject to international law, with owners/shareholders generally being national governments.

- They play the role of a facilitator and intermediary in international finance.

- Examples include the World Bank/International Bank for Reconstruction and Development (IBRD), the International Finance Corporation (IFC), the Asian Development Bank (ADB), and the International Monetary Fund (IMF).

- The World Bank helps countries reconstruct economies and assists developing countries with economic growth.

- The IMF promotes international financial stability and monetary cooperation, facilitates international trade, employment, sustainable growth, and poverty reduction.

- Other regional financial institutions like the Bank of International Settlement (BIS) are also mentioned. National Development Banks (NDBs) are also listed in this context.

- Alternative Investment Funds (AIFs):

- Mentioned as a type of institution that includes Angels, Venture Capital, Private Equity, and Hedge Funds.

- AIFs registered with SEBI receive capital from the Fund of Funds for Start-ups managed by SIDBI, for investment in start-ups. Hedge funds are mentioned separately as a type of AIF and FIIs invest in them.

- Neobanks:

- Described as a type of direct bank operating exclusively online without traditional physical branches.

- They leverage technologies like AI and machine learning for personalized services and cost minimization. Benefits are listed. These represent a newer form of banking institution.

Other institutions and roles mentioned in the sources include:

- Fee Based Financial Service Providers: Including Venture Capital Financing, Factoring & Forfeiting, Leasing, Underwriting, Credit Rating Agencies, among others. Factoring institutions and Leasing companies are also listed among Financial Intermediaries or New Financial Institutions in other contexts. Credit Rating Agencies like CRISIL, ICRA, CARE, and India Ratings and Research provide credit reports, sector studies, and advisory services.

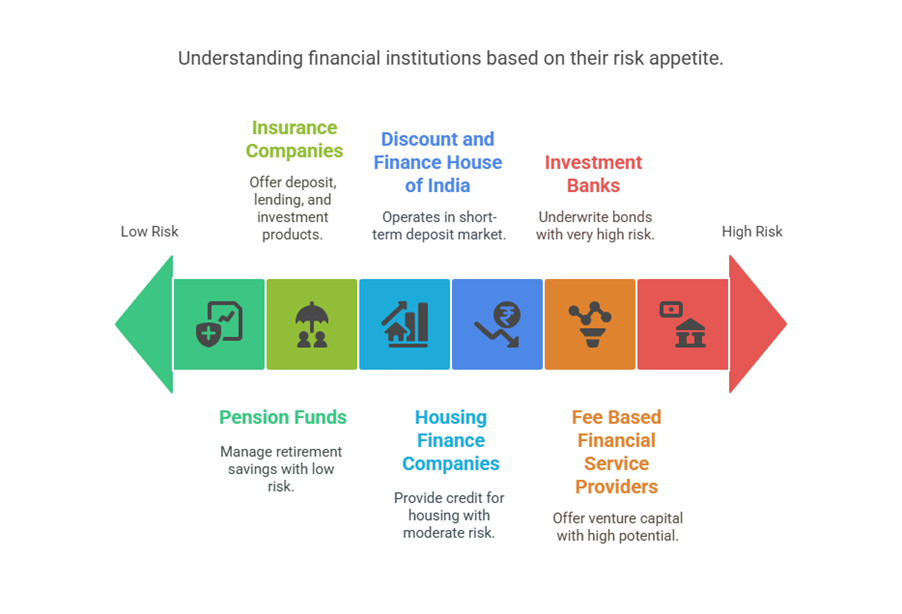

- Insurance Companies: Provide deposit, lending, and investment products. They operate in life and general insurance, with pension business being specialized life assurance. The sector is regulated by the IRDA.

- Pension Funds: Serve as primary vehicles for retirement benefits and savings, managing assets and paying benefits to retirees. Some are insured by life insurance companies.

- Investment Banks: Involved in underwriting bonds created through securitization.

- Housing Finance Companies (HFCs): Are major institutional purveyors of credit among non-banking institutions. The National Housing Bank provides refinancing.

- Discount and Finance House of India (DFHI): Enhanced activity in the Call Money Market and Short-term Deposit Market.

These institutions, operating within the Indian Financial System which includes financial markets, intermediaries, and instruments, facilitate the flow of funds and resource mobilization, sometimes through innovative ways. They collectively form the structure through which businesses can procure capital for short, medium, and long-term needs.