Financial markets are dynamic environments where new instruments are constantly introduced and evolved to meet the diverse needs of investors and businesses. These “new financial instruments” play a significant role in resource mobilization and risk management, reflecting an increasing sophistication in financial transactions driven by factors like globalization and technological advancements.

Within the Money Market, several instruments are highlighted as relatively new or gaining prominence, supplementing traditional tools like call money and treasury bills.

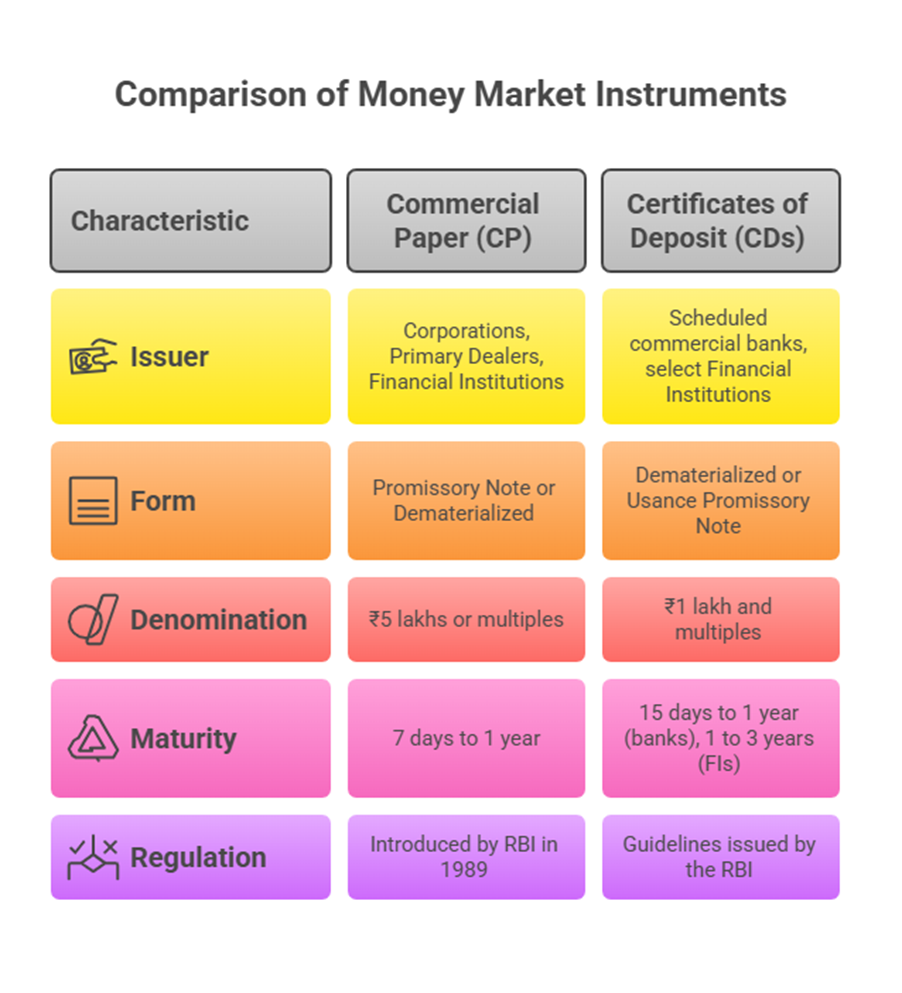

- Commercial Paper (CP) is frequently mentioned as a key new money market instrument. It is an unsecured short-term debt paper, typically issued in the form of a promissory note (often a Usance Promissory Note due to stamp duty advantages in India) or dematerialized form. Introduced by the Reserve Bank of India (RBI) in 1989, CP aimed to enable highly-rated corporate borrowers to diversify their sources of short-term borrowings and provide investors with an additional instrument. Besides corporations, Primary Dealers and All India Financial Institutions are also allowed to issue CPs. CPs are issued in denominations of ₹5 lakhs or multiples thereof for maturities between a minimum of 7 days and a maximum of up to one year from the date of issue. Issuers must appoint a scheduled bank as an Issuing and Paying Agent (IPA). Generally issued on a discount basis, the interest rate is often linked to the yield on the one-year government bond.

- Certificates of Deposit (CDs) are also noted as negotiable money market instruments. They are issued in dematerialized form or as a Usance Promissory Note for funds deposited at a bank or other eligible financial institution for a specified time. Guidelines for CDs are issued by the RBI. Scheduled commercial banks (excluding certain types) and select all-India Financial Institutions permitted by RBI can issue CDs. CDs have a minimum deposit of ₹1 lakh and multiples thereof. The maturity period for banks is not less than 15 days and not more than 1 year. For financial institutions, it should not be less than 1 year and exceed 3 years. CDs, along with other instruments, facilitate different short-term borrowings for borrowers to collect funds as needed.

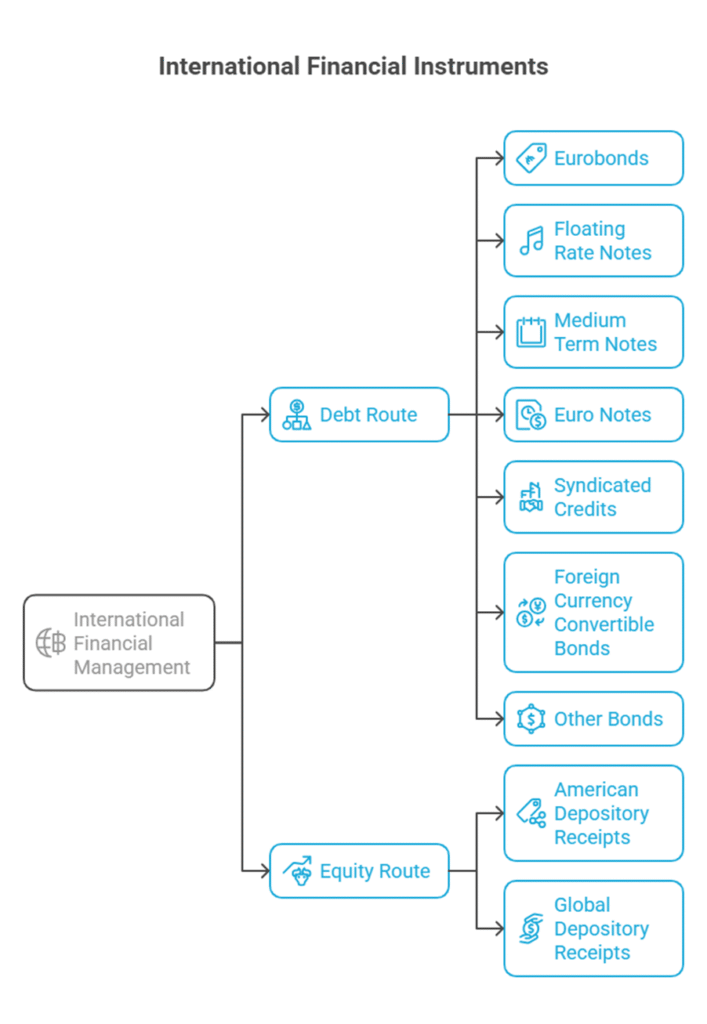

In the realm of International Financial Management, a variety of instruments have emerged to facilitate cross-border finance. These can broadly be categorized under the Debt Route and Equity Route for obtaining foreign currency financing.

- Under the Debt Route:

- Eurobonds are bonds denominated in a currency other than that of the country in which they are issued. Examples include a Yen-denominated bond in the UK or a US dollar bond in France. London is a significant market for Eurobonds. They can be fixed-rate bonds (straights) or Floating Rate Notes (FRN).

- Floating Rate Notes (FRN) have maturity periods varying from 5-7 years and varying coupon rates, often pegged to another security or re-fixed periodically, commonly referenced to LIBOR. They provide cheaper money than foreign loans and can help issuers hedge against interest rate volatility. Types include Flip-Flop FRNs, Mismatch FRNs, and Mini-Max FRNs. ECBs can also be in the form of floating rate notes.

- Medium Term Notes (MTNs) programs allow an issuer to issue Euro notes with different maturities (over one year) for frequent financing needs. This allows flexibility in timing and features while streamlining documentation. MTNs are essentially fixed-rate funding arrangements.

- Euro Notes are a concept distinct from syndicated bank credit and Eurobonds in structure and maturity. They are short-term instruments, priced usually a few basis points over LIBOR, and involve minimal documentation. Euro Commercial Paper (ECP) is a type of Euro note, being a short-term unsecured promissory note, usually designated in US Dollars with maturities up to one year. Note Issuance Facilities (NIFs) are medium-term commitments enabling borrowers to issue short-term paper.

- Syndicated Credits are bank loans (typically floating rate, fixed maturity) arranged by lead manager banks with participation from others. A typical Eurocredit might have a 5-10 year maturity, semi-annual amortization, and interest rates referenced to LIBOR. They can be structured with options like a drop-lock feature or a multicurrency option.

- Foreign Currency Convertible Bonds (FCCBs) are quasi-debt securities, tradable, issued in a foreign currency, which are convertible into Depository Receipts or local shares at a fixed price after a lock-in period. They carry a fixed interest rate (often low by Indian standards) and the option for conversion into a fixed number of equity shares, usually with a premium element. Interest and redemption (if not converted) are typically payable in dollars. FCCBs can include Call (issuer’s right to convert) or Put (investor’s right to sell back) options.

- Other bonds mentioned include Global bonds (qualify for trading in multiple markets), Easy Exit Bonds (provide liquidity via redemption/buy back), Option Bonds (interest payable on maturity or periodically, redemption premium offered), Secured Premium Notes (SPNs) (debt with detachable warrant, convertible to equity), and IFC Masala Bonds (rupee-denominated bonds offered by International Finance Corporation, an arm of the World Bank). ECBs also include securitised instruments like fixed rate bonds.

- Under the Equity Route:

- American Depository Receipts (ADRs) are negotiable instruments, denominated in dollars, issued by a US Depository Bank representing ownership of shares in a non-US company. They allow non-US companies to list and access both institutional and retail markets in the US.

- Global Depository Receipts (GDRs) are also listed alongside Commercial Papers and Securitization of Debt as New Financial Instruments.

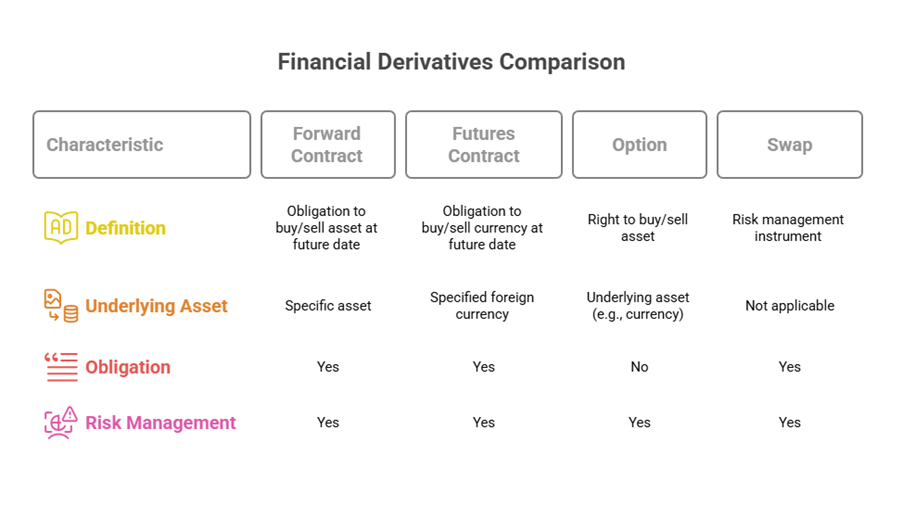

Financial Derivatives represent another class of instruments, primarily used for risk management. Their value is derived from one or more underlying financial assets.

- Basic derivatives include Forwards, Futures, Options, and Swaps.

- A Forward Contract is a simple derivative obliging parties to buy/sell a specific asset at a specific price on a future date. Foreign exchange forwards are mentioned.

- Futures Contracts are obligations (not rights) to buy/sell a specified foreign currency in the present for settlement at a future date. Hedging using Futures is a noted application.

- An Option is the right (not obligation) to buy or sell an underlying asset (like foreign currency) at a certain price on or before a specified date. They provide a hedge against risks. Types include Interest Rate Options and Foreign Currency Options.

- Swaps are also derivative instruments used for risk management.

- Other derivatives mentioned include Credit Derivatives, Real Options, Commodity Derivatives, Weather Derivatives, and Electricity Derivatives. A Forward Rate Agreement (FRA) is a specific interest rate derivative contract guaranteeing a future interest rate. Interest Rate Derivatives also include Interest Rate Futures and Options, Caps, Floors, and Collars. Transaction risk can be hedged using derivatives like Forwards, futures, options, swaps.

Beyond these categories, other specialized or contemporary financial instruments and concepts are discussed:

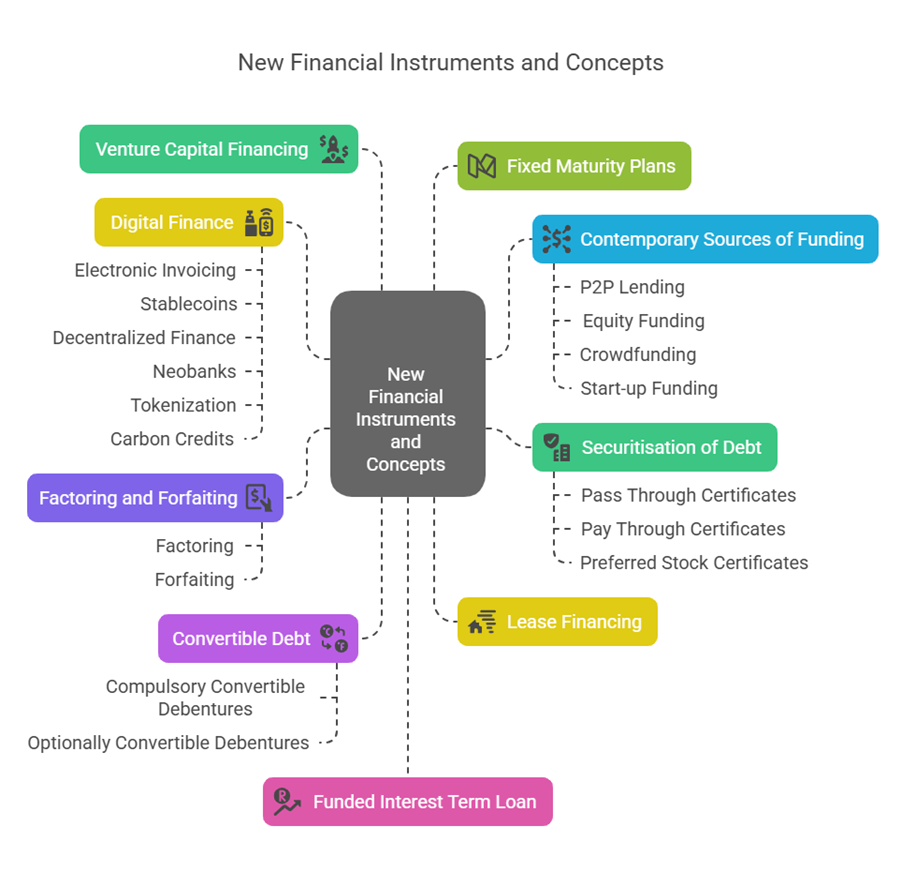

- Securitisation of Debt is listed as a new financial instrument and a topic for discussion. It involves converting assets into marketable securities. Specific certificates mentioned in securitisation include Pass Through Certificates, Pay Through Certificates, and Preferred Stock Certificates.

- Factoring and Forfaiting are services related to the management of accounts receivables. Factoring is the sale of accounts receivable to a factor. Forfaiting involves an exporter relinquishing rights to a future receivable for immediate cash at a discount, passing collection risks to the forfeiter.

- Lease Financing is presented as a source of finance, involving different types of lease agreements.

- Venture Capital Financing is discussed as a type of financing.

- Convertible Debt is listed as another source of finance. This includes instruments like Compulsory Convertible Debentures (CCD) and Optionally Convertible Debentures (OCD), which are hybrid securities.

- Fixed Maturity Plans (FMPs) are closed-ended mutual funds investing in instruments like CDs, CPs, Money Market Instruments, and Non-Convertible Debentures over a fixed period.

- Funded Interest Term Loan (FITL) is an RBI-regulated mechanism to fund unrealized interest in borrowable accounts.

- Contemporary sources of funding include P2P lending, Equity funding, Crowdfunding (raising money from a large number of people), and Start-up funding. The Government of India has initiatives like the SIDBI Fund of Funds Scheme to catalyse funding for start-ups via Alternative Investment Funds (AIFs).

- Within Digital Finance, new concepts and instruments are emerging, such as Electronic Invoicing, Stablecoins (cryptocurrencies attempting to maintain price stability), Decentralized Finance (DeFi), Neobanks (online-only banks), and Tokenization. Trading in Carbon Credits is also mentioned as a creative source of funding.

The introduction of these new instruments reflects the evolving landscape of financial management, providing diverse options for raising funds and managing financial risks. While they offer benefits like increased liquidity [factoring] and specialized risk hedging [derivatives], they also require careful understanding and management due to their specific features and associated risks. Financial institutions exist to provide access to a wide variety of these deposit, lending, and investment products.