Capital structure is a core area within financial management. It refers to the composition or make-up of a company’s capitalization. Essentially, it represents the specific mixture or mix of long-term debt and equity that a firm uses to finance its assets and meet its long-term investment requirements. The term “capital structure” is also defined as the mix of different sources of long-term funds employed by a firm. Deciding the suitable capital structure is considered an important decision of financial management because it is closely related to the value of the firm.

While sometimes used interchangeably with financial structure, the sources clarify that capital structure is only a part of financial structure. Financial structure refers to the entire liabilities side of the Balance Sheet, showing the pattern of total financing from both long-term and short-term sources. Capital structure, on the other hand, represents only the long-term sources of funds and excludes all short-term debt and current liabilities.

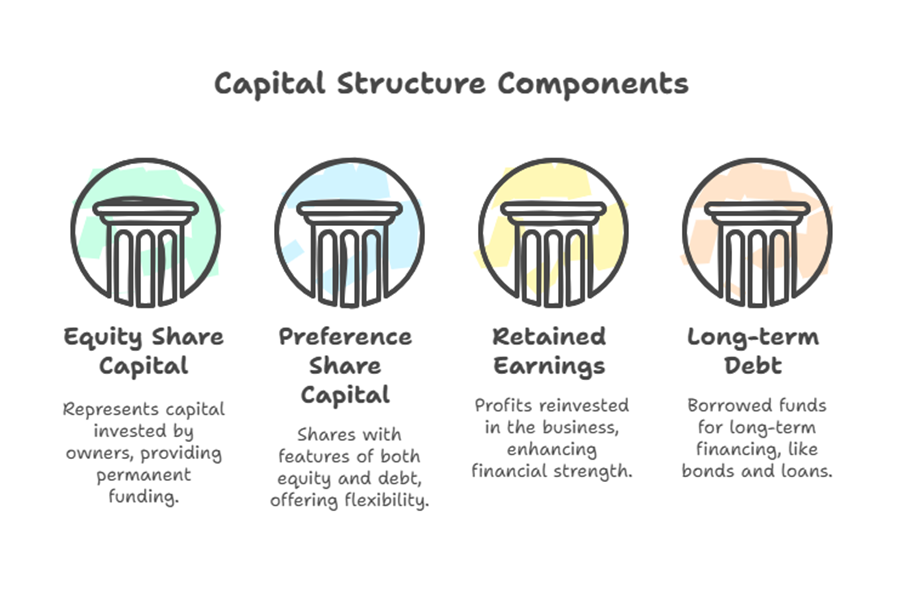

Components of Capital Structure

The long-term sources of funds that constitute a company’s capital structure are mobilized through owner’s funds and long-term debt. These components are reflected in the liabilities side of the balance sheet as long-term liabilities. The sources identify the following as key components:

Equity Share Capital / Common Stock Equity / Ownership Securities: This represents the capital invested by the owners. It is a source of permanent capital and includes ordinary equity shares. Equity capital is a basic source of finance for any firm, providing funds on a permanent basis and acting as a base for creating debt capacity.

Preference Share Capital / Preferred Stock / Ownership Securities: These are also part of owner’s funds or ownership securities. Preference shares have features of both equity and debt capital.

Retained Earnings / Reserves / Profit & Loss Account balance: These are profits retained in the business rather than distributed as dividends. They are considered a component of owner’s funds. Notably, one source states that “capitalization… does not include reserve and surplus”, while others explicitly include “reserves” or “retained earnings” when defining capital structure, indicating a distinction between the term “capitalization” as par value and “capital structure” as the mix of long-term resources.

Debentures / Bonds / Long-term Debt / Loans from Financial Institutions / Creditorship securities: These represent borrowed funds that are long-term in nature. Debentures and bonds are instruments for raising long-term capital. Long-term debt is a form of borrowed funds.

These components, particularly equity share capital, preference share capital, retained earnings, and long-term debt (such as debentures, bonds, and long-term loans), make up the mix that constitutes a firm’s capital structure used for permanent financing.

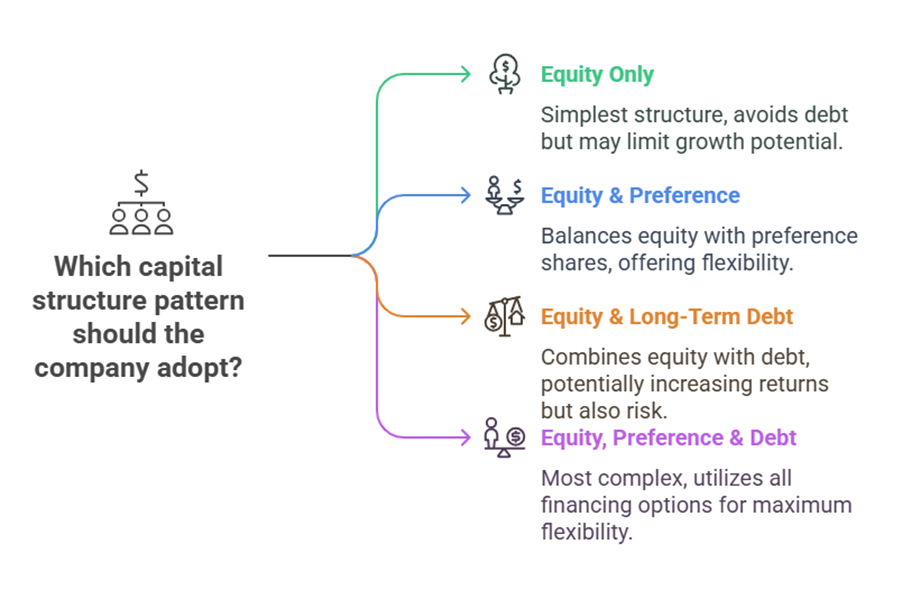

Fundamental Patterns of Capital Structure

Based on the combination of these long-term sources, the sources identify four fundamental patterns or forms of capital structure that a company may have:

Equity capital only (including Reserves and Surplus): In this pattern, the firm is financed solely by owner’s equity, which includes both the initial equity share capital and profits retained over time.

Equity and preference capital: This structure involves financing through a combination of equity shares and preference shares.

Equity and long-term debt: Here, the firm utilizes both equity shares and long-term borrowed funds like debentures, bonds, or long-term loans from financial institutions.

Equity shares, preference shares and debentures (or Equity, preference and long-term debt): This is the most complex of the fundamental patterns, involving all three main types of long-term finance: equity shares, preference shares, and long-term debt instruments like debentures.

These patterns represent different combinations of the major long-term financing sources available to a company.

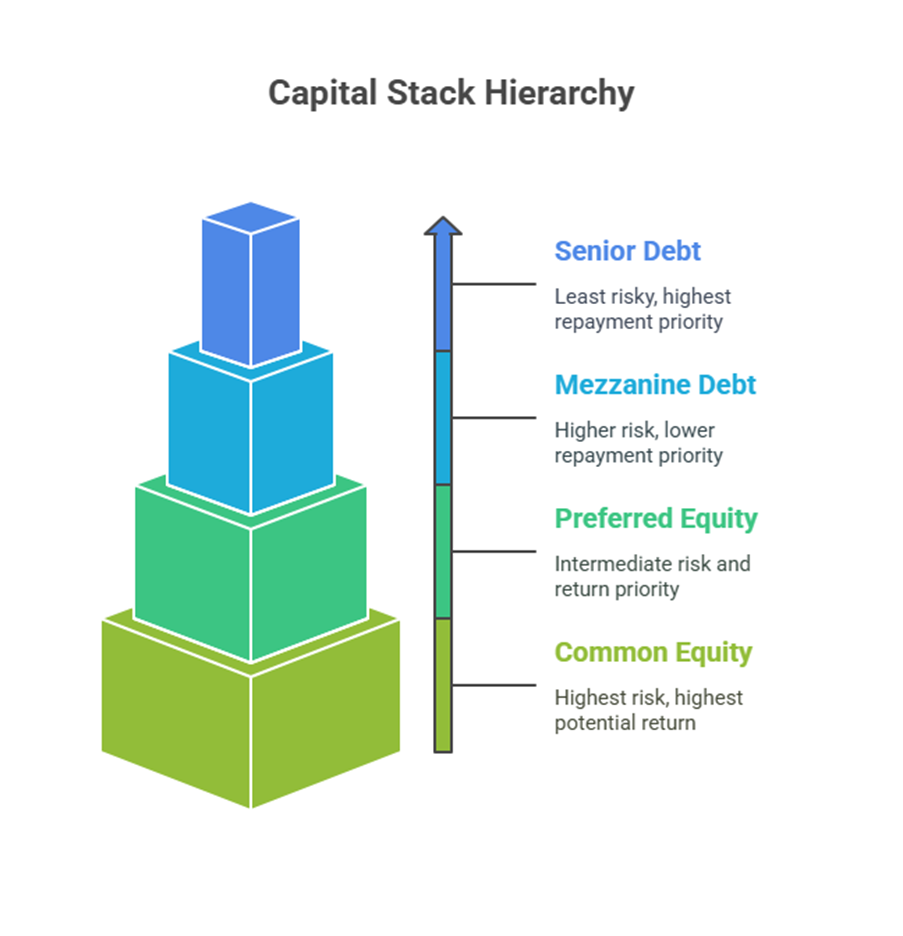

The Capital Stack

The concept of the “capital stack” provides a visual representation (like a pyramid) of the organization and hierarchy of the capital contributed to finance a venture or deal. Each level of the stack represents a different source of capital (both debt and equity) and indicates the priority of payouts and returns, as well as the associated risk and potential return. The levels, from bottom to top (least risky/return to most risky/return), are typically:

Senior Debt: Located at the base of the stack, this is the least risky position and has the highest priority for repayment in case of default or bankruptcy.

Mezzanine Debt / Junior Debt: Positioned above senior debt, it has a lower priority for repayment and consequently higher risk and potential return.

Preferred Equity: This is above mezzanine debt and below common equity, reflecting its intermediate priority.

Common Equity: At the top of the stack, common equity represents the highest risk position but also has the highest potential for return.

Understanding the capital stack helps illustrate the different levels of risk and reward associated with various components of the capital structure.

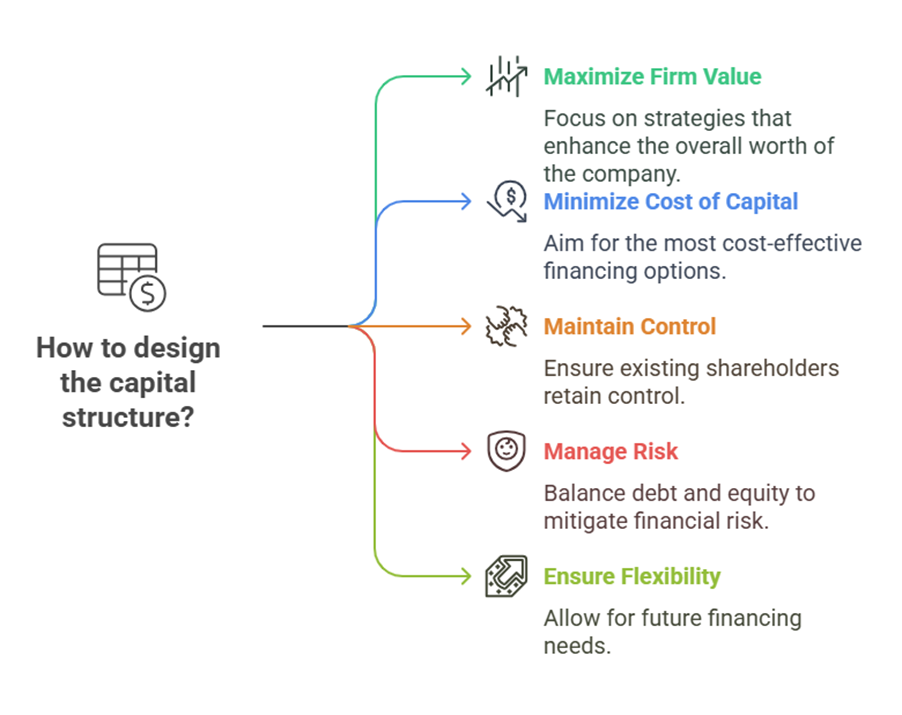

Designing the Capital Structure

Financial managers plan the appropriate mix of different securities in the total capitalization. The process of deciding the forms, actual requirements, and relative proportions of financing in total capitalization is known as the capital structure decision.

The objective of designing a capital structure is typically to maximize the value of the firm and minimize the overall cost of capital. While practically difficult to achieve simultaneously with other objectives like control and risk management, maximizing firm value is a prime objective.

Factors influencing this decision include:

Control: Designing the structure so that existing shareholders maintain control.

Risk: Managing financial risk, which increases with more debt. Reliance is often placed more on common equity than excessive debt.

Cost: Aiming for a pattern that minimizes the cost of capital structure. Debt capital is often cheaper than equity, partly due to the tax deductibility of interest.

Flexibility: Ensuring the structure allows for future financing needs.

Nature of the business: Businesses with long operating periods may prefer more equity.

Size of the company: Large firms might manage finances internally, while smaller ones might need external finance.

Financial Leverage or Trading on Equity: The use of fixed interest/dividend bearing finance (debt and preference shares) along with equity can magnify EPS if the firm’s return exceeds the cost of debt.

Tools like EBIT-EPS-MPS analysis and Indifference Point analysis help evaluate different capital structures and the effect of leverage on earnings per share (EPS) and market price per share (MPS) to guide the selection of financing patterns.

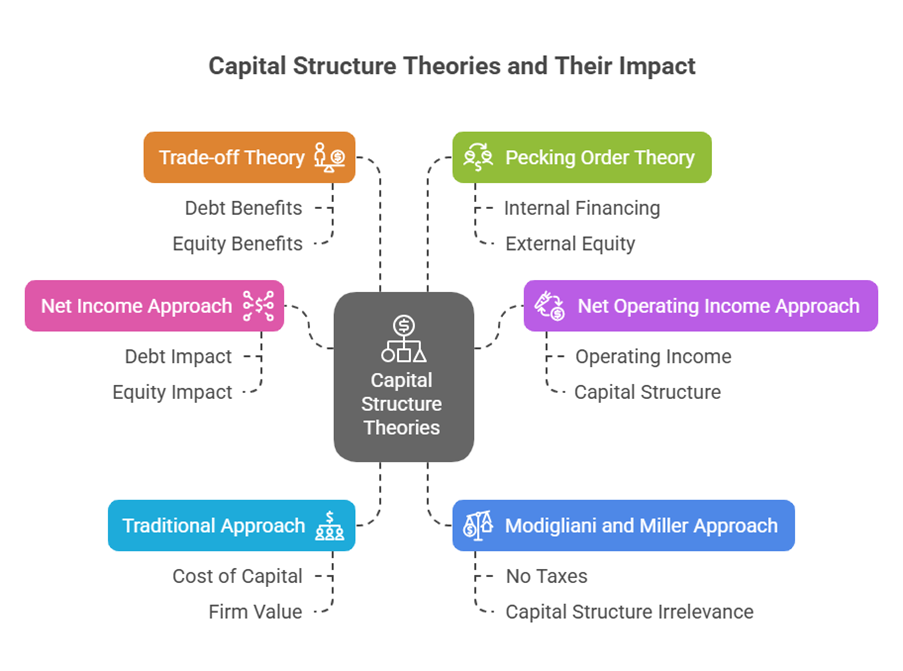

Capital Structure Theories

Various theories explore the relationship between capital structure, the cost of capital, and the value of the firm. These theories offer different perspectives on whether an optimal capital structure exists that can maximize firm value. The main theories mentioned are:

Net Income (NI) Approach

Net Operating Income (NOI) Approach

Traditional Approach

Modigliani and Miller (MM) Approach / Hypothesis

Trade-off Theory

Pecking Order Theory

These theories analyse how the mix of debt and equity might impact a firm’s value and cost of capital under different assumptions. For instance, the Traditional View suggests that there is an optimum capital structure where the overall cost of capital is minimized, while the Modigliani-Miller hypothesis, in the absence of taxes, argues that capital structure decisions are irrelevant to firm value. The Pecking Order theory suggests that managers prefer internal financing first, then debt, and external equity as a last resort, based on information asymmetry.

In conclusion, the patterns of capital structure represent the different combinations of long-term funding sources used by a company, primarily equity, preference shares, retained earnings, and long-term debt. The choice among these patterns is a significant financial decision aimed at optimizing firm value and minimizing capital cost, guided by various factors and theoretical frameworks.