Securitization is a process of converting illiquid assets into marketable securities. It is a method of transforming assets of a lending institution into negotiable instruments for generating funds. In simpler terms, securitization is the means of turning illiquid assets into liquid assets to free up blocked capital. The process involves packaging receivables on debts against collateral assets like property, land, building, and other real estate, making them exchangeable financial instruments.

The Reserve Bank of India (RBI) defines securitization as transactions where credit risks in assets are redistributed by repackaging them into tradable securities. It involves the creation of financial instruments that represent an ownership interest in, or are secured by, a segregated income-producing asset or pool of assets.

In its widest sense, securitization implies every process that converts a business relation into a transaction. More specifically, it refers to the sale of assets generating cash flows from the originating institution to a specially created company (Special Purpose Vehicle). This second company then issues notes (often interest-bearing bonds) backed by the cash flows from the original assets.

Financial engineering techniques enable bonds to be created from any type of cash flow.

Origin and Growth

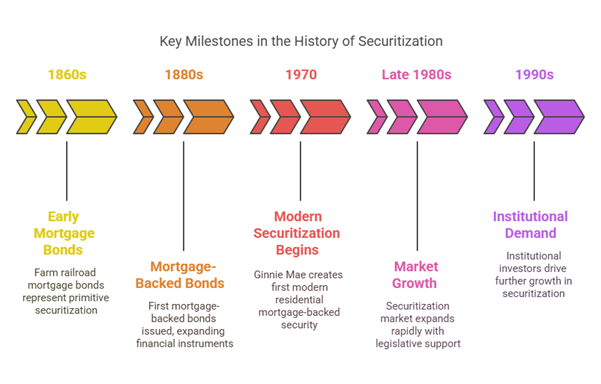

The concept of securitization, in its primitive form, dates back to farm railroad mortgage bonds in the 1860s and mortgage-backed bonds in the 1880s. However, the modern era of securitization began in 1970 with the creation of the first modern residential mortgage-backed security by the Government National Mortgage Association (Ginnie Mae or GNMA). This pooled mortgage loans and allowed them to be used as collateral for securities sold in the secondary market, aiming to channel investment capital for affordable housing.

The securitization market saw significant growth from the late 1980s and through the 1990s, aided by legislative changes (like the REMIC provisions in the US) and fuelled by increased demand from institutional investors.

Driving Forces and Benefits

A major driving force for securitization has been the need for banks to realize value from assets held on their balance sheet. Key benefits for a financial institution include:

- Funding the assets it owns.

- Balance sheet capital management.

- Risk management and credit risk transfer.

- Conversion of debt into securities.

- Conversion of non-liquid assets into liquid ones.

- Shifting assets from the balance sheet, allowing for off-balance sheet funding. This helps in better balance sheet management.

- Enhancing the borrower’s credit rating.

- Opening up new investment avenues.

- Securities are tied up in definite assets.

- In the case of non-recourse arrangements, the risk of default is shifted from the originator to the investor.

- Transferring the problem of asset-liability mismatch to investors.

Mechanism and Process

The process of securitization can be broadly described in several steps:

- Origination Function: The process begins with a borrower approaching a financial institution (the originator) for a loan, receiving debt in exchange for collateral.

- Creation of Pool of Assets: The originator identifies assets (like loans or receivables) from its balance sheet that generate cash flows. These assets are pooled together, often based on similar characteristics like interest rate, risk, maturity, and concentration units.

- Pooling Function / Transfer to SPV: The originator sells off its receivables or transfers the asset pool to a Special Purpose Vehicle (SPV). The SPV is an entity specifically created for this purpose, often in the form of a trust or company, and is designed to be bankruptcy remote from the originator. The originator transfers both legal and beneficial interest to the SPV. The originator may receive a lump sum amount, possibly at a discounted value.

- Securitization / Sale of Securitized Papers: The SPV transforms these receivables into marketable securities, such as Pay Through Certificates or Pass-Through Certificates. The SPV designs these instruments based on the nature of interest, risk, tenure, and the asset pool. These securities are then sold to investors in the capital market, often through merchant or investment banks acting as arrangers or structurers. The SPV finances the acquisition of the pooled assets by issuing these tradable, interest-bearing securities.

- Structuring and Credit Rating: The securities offered by the SPV are often structured into different tranches (slices) based on risk and return, such as junior, mezzanine, and senior tranches. The risk and return vary by tranche, with junior tranches bearing more risk and potentially higher return. Credit rating can be done before the sale of instruments to assess issuer risk.

- Administration of Assets / Servicing: The administration of the pooled assets is often subcontracted back to the originator. The servicer (typically the originator) collects principal and interest payments from the original borrowers and transfers them to the SPV or a trustee. A servicing fee is deducted.

- Repayment of Funds: The SPV repays funds to the investors in the form of interest and principal, generated from the pooled assets.

- Recourse: Unless specified otherwise, in case of default by the debtors, receivables may go back to the originator from the SPV in a recourse arrangement. However, assets can also be transferred without recourse, shifting the risk to the investor.

- Clean-up: When only a small amount of receivables remains outstanding, the originator may buy them back to close the transaction.

- Profit Distribution: At the end of the transaction, any remaining profit for the originator is paid out.

Participants

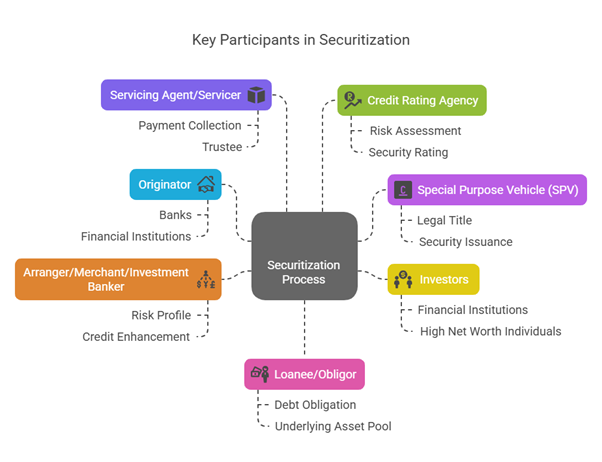

The main parties involved in securitization are:

- Originator: The entity that initiates the deal or owns the assets/receivables to be securitized. Examples include banks, financial institutions, or companies.

- Special Purpose Vehicle (SPV): Also called the issuer, this entity is created specifically to purchase the assets from the originator and issue securities to investors. It holds the legal title to the assets.

- Investors: Individuals or institutions who purchase the securities issued by the SPV. These can include financial institutions, insurance companies, pension funds, hedge funds, companies, and high net worth individuals.

- Arranger/Merchant/Investment Banker: A financial institution appointed by the originator to design the securitization structure, determine risk profiles, set up the SPV, and design credit enhancement/liquidity support. They may also be called a structurer.

- Servicing Agent/Servicer: The entity responsible for collecting payments from the original borrowers and passing them on to the SPV or trustee. Often, this is the originator.

- Credit Rating Agency: An agency that rates the securities issued by the SPV to assess their risk.

- Loanee/Obligor: The original borrower who owes the debt that forms the underlying asset pool.

Securitizable Assets

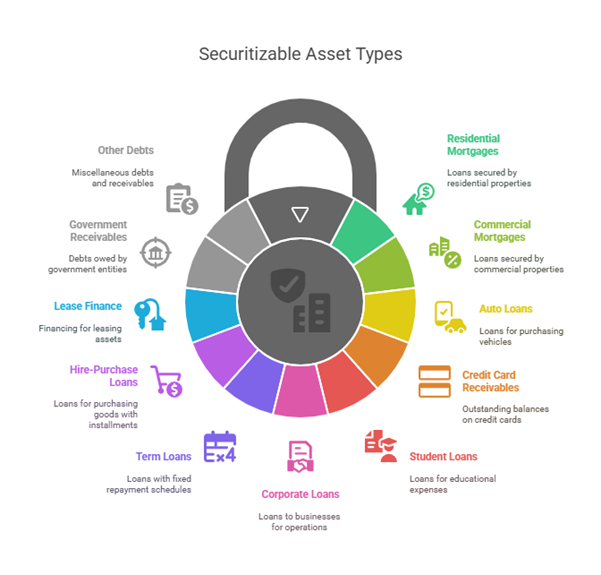

Any type of asset with a stable cash flow can potentially be structured into a reference portfolio for securitization. Common examples include:

- Residential Mortgages.

- Commercial Mortgages.

- Auto Loans.

- Credit Card Receivables.

- Student Loans.

- Corporate Loans.

- Term Loans to financially reputed companies.

- Hire-purchase loans.

- Lease Finance.

- Receivables from Government Departments.

- Other debts and receivables.

Securitization Instruments

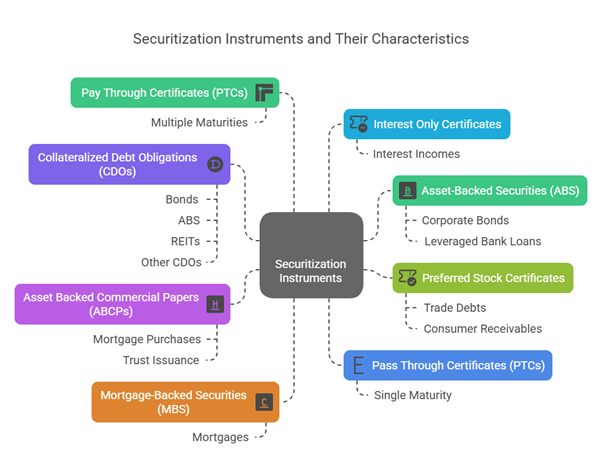

The securities issued by the SPV backed by the asset pool are known generally as Asset-Backed Securities (ABS). Transactions backed exclusively by mortgages are called Mortgage-Backed Securities (MBS). A variant is the Collateralized Debt Obligation (CDO). CDOs are backed by a pool of debt instruments like bonds, ABS, REITs, or other CDOs. CDOs can be further categorized based on the underlying assets, such as Collateralized Bond Obligations (CBOs) backed by corporate bonds, and Collateralized Loan Obligations (CLOs) backed by leveraged bank loans. CDOs are considered a type of credit derivative.

Other specific instruments issued by the SPV include:

- Pass Through Certificates (PTCs): These securities represent a direct claim of investors on the securitized assets. The originator transfers the entire cash receipts (interest and principal) from the assets to the SPV, which passes them on to the certificate holders at regular intervals. Pass-throughs have a single maturity structure matched to the life of the underlying assets.

- Pay Through Certificates (PTCs): These securities have multiple maturity structures. The SPV may temporarily reinvest the cash flows to bridge gaps between payment dates. The payments to investors depend on the cash flow from the backing assets.

- Preferred Stock Certificates: Issued by a subsidiary company against the trade debts and consumer receivables of its parent company. They are generally short-term and often backed by guarantees from highly rated merchant banks.

- Asset Backed Commercial Papers (ABCPs): Short-term instruments often used in the MBS structure, where the SPV purchases mortgages from various sources, pools them, and transfers them to a Trust which issues mortgage-backed certificates.

- Interest Only Certificates: Payments to investors are made solely from the interest incomes earned from the securitized assets.

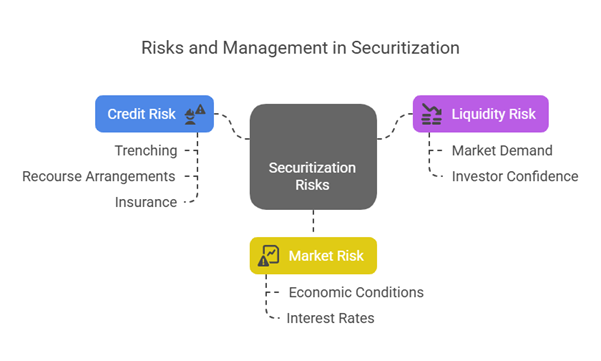

Risks in Securitization

Investors in securitization transactions are exposed to several risks:

- Credit Risk: The risk that the underlying obligors will default on their payments. This risk can be managed through trenching (splitting assets based on risk), recourse arrangements, or insurance.

- Liquidity Risk: The risk that the securities may not be easily saleable in the market.

- Market Risk: General market fluctuations that could affect the value of the securities.

Securitization itself acts as a tool for risk management, particularly by transferring default risk from the originator to the investor in non-recourse structures.

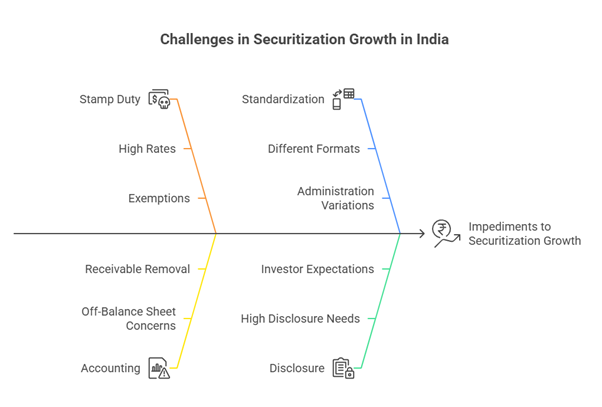

Problems and Challenges in India

Several problems impede the growth of securitization in India:

- Stamp Duty: High stamp duty rates on mortgage debt in some states act as an obstacle. Pass-through certificates are often exempted as they do not evidence debt.

- Accounting: Concerns exist regarding the accounting and reporting of securitized assets, especially when transferred without recourse. While intended to be off-balance sheet, removing receivables can pose problems.

- Lack of Standardization: Different originators use different formats for documentation and administration, hindering standardization.

- Securitization requires a high level of disclosure of information to various parties.

- Investors are primarily interested in high-quality asset-backed securities.

Despite challenges, the Government has taken steps like enacting the SARFAESI Act, 2002, to encourage securitization and manage Non-Performing Assets (NPAs). SEBI has also allowed Foreign Portfolio Investors (FPIs) to invest in securitized debt of unlisted companies.

Pricing

The price of a securitized instrument from an investor’s perspective is determined by discounting the expected future cash flows using a yield comparable to securities of similar credit quality and average life. This yield can be estimated using a yield curve for marketable securities, with adjustments for spread points based on the credit quality of the securitized instruments.