Security financing is a fundamental aspect of financial management, particularly relevant to a company’s financing decisions and capital structure. It involves the mobilization of finance through the issuance of securities, such as shares and debentures. These are also referred to as corporate securities.

Core Concept and Role At its core, security financing is a method companies use to raise funds from investors by offering them a stake in the company (ownership securities) or a claim on its assets and earnings (creditorship securities). This process plays a major role in determining the capital structure of a company, which is the mix of debt and equity it uses to finance its operations. Security financing is primarily associated with meeting the long-term financial needs of a business, such as investments in plant, machinery, land, buildings, and financing permanent working capital.

Characteristics of Security Finance Based on the sources, the key characteristics of security finance are:

- It represents a long-term source of finance.

- The instruments issued are also known as corporate securities.

- It includes both shares and debentures.

- It plays a significant role in deciding the capital structure of the company.

- The repayment of this type of finance is generally limited.

- It constitutes a major part of the company’s total capitalization.

Types of Security Finance Security finance is broadly classified into two main types:

- Ownership Securities: These are also called capital stock and are commonly known as shares. They represent ownership in the business concern. Shares are described as the most universal method for raising finance for businesses.

- Creditorship Securities: These are also known as debt capital or debt finance, meaning the finance is mobilized from creditors.

Elaboration on Ownership Securities (Shares)

Ownership securities, or shares, represent the ownership fund of the company and are permanent to the capital structure. A public limited company can raise funds from promoters or the investing public by issuing ordinary equity shares.

- Equity Shares:

- Characteristics: Equity shares are a source of permanent capital for a company. The holders of such shares are called equity shareholders or ordinary shareholders. Equity share capital provides a layer of security to other suppliers of funds, as lenders consider the debt-equity ratio to ensure it is comfortable enough to cover the debt.

- Types: Various types of equity shares exist, including New issues, Rights issues (offering new shares to existing shareholders pro rata), Bonus Shares, and Sweat Equity Shares. Sweat equity shares are issued by a company to its directors or employees at a discount or for consideration other than cash, for providing know-how, intellectual property rights, or value additions.

- Advantages: A key advantage of raising funds by issuing equity shares is that it is a permanent source of finance. Since these shares are generally not redeemable, the company does not have a liability for cash outflows associated with redemption. Once issued, equity shares are tradable, meaning investors can buy and sell them. The company is not responsible for cash outflows for investors who become shareholders by purchasing shares from existing shareholders.

- Preference Shares:

- Preference shares differ from equity shares as they grant holders specific rights regarding the receipt of dividends and the payment of capital, prioritizing them over common/equity shareholders. The dividend payment on preference shares is typically fixed. Preference shares possess features of both equity shares and debt capital.

- Types: Preference shares can be classified based on different features:

- Cumulative Preference Shares: Arrears of dividend accumulate if the dividend is not paid in a year, and the company must pay these arrears before paying any dividend on common/equity shares.

- Non-Cumulative Preference Shares: Arrears of dividend do not accumulate. If a dividend is not possible in a year, it is lost.

- Participating Preference Shares: These shares have additional rights, usually allowing them to participate in surplus profits after the regular dividend payment.

- Non-Participating Preference Shares: These are the usual type, where holders are not entitled to participate in surplus profits unless explicitly stated otherwise.

- Convertible Preference Shares: These include the right to convert the shares into equity shares after a specified period or at the option of the holder.

- Non-Convertible Preference Shares: These shares do not carry the option of conversion into equity shares.

- Redeemable Preference Shares: These shares can be repaid after a specified period or during the company’s lifetime.

Elaboration on Creditorship Securities (Debt)

Creditorship securities, or debt finance, involve obtaining funds from creditors. The main parts of creditorship securities are Debentures and Bonds.

- Debentures:

- Definition: A debenture is a document issued by a company under its seal acknowledging a debt. According to the Companies Act 1956, a debenture includes debenture stock, bonds, and any other securities of a company, regardless of whether they constitute a charge on the company’s assets. A debenture is essentially a document evidencing or acknowledging a debt.

- Characteristics: Debentures are instruments used for raising long-term capital with a fixed period of maturity. They normally carry a fixed rate of interest (coupon rate) payable periodically to the holders. Debenture holders are considered creditors of the company. Debentures are usually issued in different denominations and may carry different rates of interest. They are often issued based on a debenture trust deed that lists the terms and conditions. Debentures typically do not have voting rights. They can be redeemed during the life of the company.

- Types: Debentures can be classified based on various criteria, including issue and redemption conditions:

- Convertible Debentures: Give the holder the right to convert them into shares. This can be fully convertible or partially convertible.

- Non-Convertible Debentures: Cannot be converted into shares.

- Partly Convertible Debentures: Carry features of both convertible and non-convertible debentures.

- Bearer Debentures: Transferable like negotiable instruments, with interest paid to the bearer.

- Registered Debentures: Interest is payable to the person registered as the debenture holder.

- Mortgage Debentures: Secured by a charge on the company’s asset(s). This includes First Mortgage debentures (have a first claim on charged assets) and Second Mortgage debentures (have a claim after the first mortgage debentures).

- Naked or Simple Debentures: Unsecured.

- Redeemable Debentures: Can be repaid after a specific period or in installments during the lifetime of the company.

- Irredeemable or Perpetual Debentures: Cannot be redeemed during the company’s lifetime and are repayable only on the winding up of the company or the expiry of a long term.

- Zero Interest Fully Convertible Debentures (ZIFCD): These debentures do not carry any interest. They are compulsorily and automatically converted into new equity shares at a predetermined price after a specified period. From the company’s perspective, they are beneficial as no interest is paid.

- Bonds:

- Definition: A bond is a fixed income security created to raise funds. It is a negotiable certificate that entitles the holder to repayment of the principal sum plus interest. Bonds are debt securities issued by a company or government agency, where the investor lends money to the issuer, and the issuer promises to repay the loan amount on a specified maturity date.

- Types based on Call Feature:

- Callable Bonds: Have a call option giving the issuer the right to redeem the bond before maturity at a predetermined price (call price), generally at a premium.

- Puttable Bonds: Give the investor a put option, which is the right to sell the bond back to the company before maturity.

- Government Securities: Include bonds or dated securities issued by the central or state governments with an original maturity of one year or more. They acknowledge the government’s debt obligation and are considered risk-free gilt-edged instruments due to practically no risk of default. State governments issue State Development Loans (SDLs).

- Other Types of Bonds:

- Foreign Bonds: Bonds issued in a domestic capital market by a foreign entity, known by different names in various countries (e.g., Yankee Bonds in the US, Samurai Bonds in Tokyo, Bulldogs in the UK).

- Foreign Currency Convertible Bonds (FCCB): Issued in accordance with relevant schemes and subscribed by non-residents in foreign currency. They are convertible into ordinary shares of the issuing company. FCCBs are unsecured, carry a fixed interest rate, and have an option for conversion. Interest and redemption (if not converted) are typically paid in dollars. Interest rates are often low.

- Euro Bonds: Issued in the Eurocurrency market. Euro Convertible Bonds are a type of Euro bond that can be converted into Depository Receipts or local shares and may include Call or Put options. Euro-bonds with Equity Warrants carry a coupon rate and have detachable warrants, allowing fixed-income funds to invest for regular income while potentially benefiting from equity upside via warrants.

- Masala Bonds: Rupee-denominated bonds which serve as a source of debt financing for the public and private sector.

- Mortgage Bonds: Secured through a lien against the firm’s property.

- Subordinated Bonds: Have a lower priority than secured debts, debentures, and general creditors in the event of liquidation.

- Guaranteed Bonds: Obligations guaranteed by another entity.

- Perpetual Bonds: Also called perpetuities, they have no maturity date.

Methods Related to Issuing Securities

- Book Building: This is a process used by an issuer planning an offer to determine the price of securities. It involves nominating lead merchant banker(s) as ‘book runners’, specifying the number of securities and a price band (lowest as floor price, highest as cap price), appointing syndicate members to collect investor orders (bids), and entering these orders into an ‘electronic book’. The bidding process is similar to an open auction. The book remains open for a specified period (e.g., 3-7 days). After evaluating bids based on demand at various price levels, the book runners and issuer decide the final price at which the securities will be issued. Allocation is then made to successful bidders.

- Securitization of Debt/Assets: This is a process where illiquid and long-term assets, such as loans and receivables of financial institutions, are transformed into marketable securities. These assets, which generate cash flows, are sold to a Special Purpose Vehicle (SPV). The SPV then issues notes or bonds that are backed by the cash flows generated from the original assets. This process can address liquidity issues for companies without necessarily changing their debt-equity ratio significantly. Instruments issued by the SPV in securitization can include Pass Through Certificates, Pay Through Certificates, and Preferred Stock Certificates.

Other Instruments and Concepts Related to Security Financing

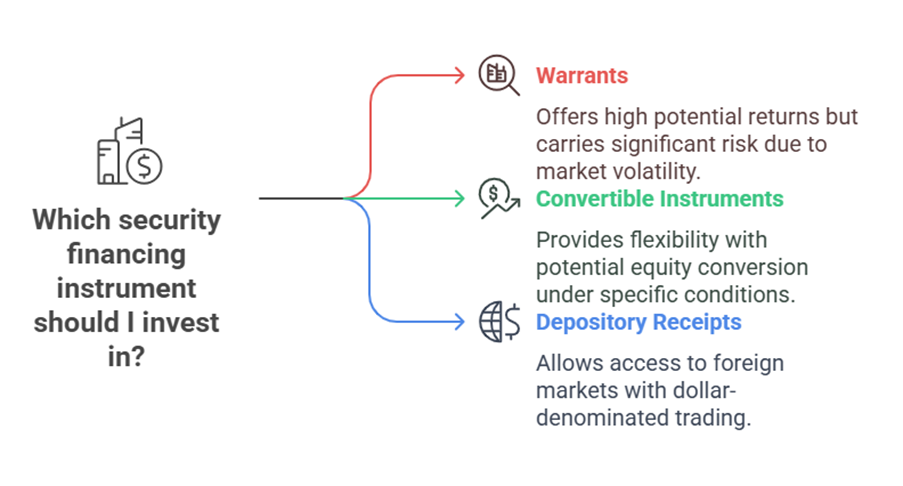

- Warrants: A security that grants the holder the right to buy the underlying stock of the issuing company at a fixed exercise price until a specified expiration date. Warrants associated with Euro-bonds are often detachable. Warrants can be highly risky but may offer high returns.

- Convertible Instruments: Include convertible debentures, partly convertible debentures, fully convertible debentures, Zero Interest Fully Convertible Debentures (ZIFCD), Foreign Currency Convertible Bonds (FCCBs), Euro Convertible Bonds, and Convertible Preference Shares. These instruments contain a feature allowing conversion into equity shares under specified conditions.

- Depository Receipts (ADRs/GDRs): Represent ownership of underlying shares of a foreign company and are traded in different markets. ADRs trade in the US and are dollar-denominated, allowing non-US companies access to the US market. GDRs trade in international markets.

Security financing is a critical component of financial management, directly impacting a firm’s long-term funding, capital structure, and financial health. Understanding the different types of securities and the processes for issuing them is essential for making informed financing decisions.