Financial management involves key decisions, including financing decisions, investment decisions, and dividend decisions. Investment decisions are concerned with the selection of assets where funds will be invested by a firm. These decisions can relate to long-term or short-term investments. Long-term investment decisions are related to investment in long-term assets or projects for generating future benefits and are popularly known as capital budgeting decisions. Capital budgeting is the firm’s decision to invest its current funds most efficiently in long-term activities in anticipation of an expected flow of future benefits over a series of years.

Long-term investment decisions, also known as capital expenditure decisions, involve substantial amounts of investment locked up for a considerable timespan, with uncertain returns and the potential for significant losses if reversed. They involve a largely irreversible commitment of resources with long-term implications, greatly impacting the firm’s future growth and profitability. Due to these characteristics – difficulty, uncertainty, risk, irreversibility, and complexity – proper care is required for investment project selection and evaluation.

Within the scope of financial management, investment decisions can be classified in various ways, including on the basis of situations or strategy. The sources distinguish between Strategic and Tactical investment decisions and planning.

Strategic Investment Decisions and Planning

Strategic planning is a fundamental part of strategic financial management. It identifies strategies for future activities and operations, defines goals, directions, and resource needs. A strategic plan states the long-range strategy for achieving organisational goals. This involves a 3 to 5 year plus time duration or longer. Long-range forecasts, generally 5 years or more, are included, covering markets, sales (including new products), price policies, production and capacity requirements, aggregate level of costs, resource needs, and financing requirements.

Strategic planning is primarily concerned with the long-range vision of the organisation, aiming to provide a sense of unity and commitment to specified purposes. While it forms the foundation on which short-term planning is based, it is not concerned with day-to-day operations. Managers involved in strategic planning should identify key variables, both internal (under management control) and external (normally non-controllable), that are believed to directly influence the achievement or non-achievement of organisational goals and objectives. Effective strategic planning requires managers to build plans and budgets that blend and harmonize external considerations and influences with the firm’s internal factors.

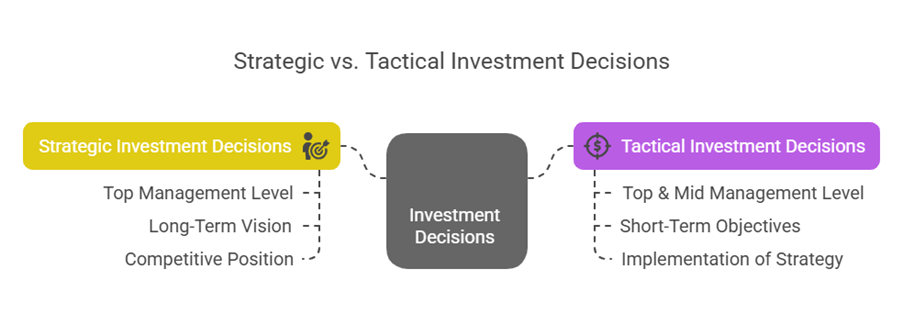

Strategic investment decisions are generally taken at the Top Management Level. Strategic financial management itself is described as a portfolio constituent of the corporate strategic plan that embraces the optimum investment and financing decisions required to attain overall specified objectives. Senior management typically decides strategy, which is a long-term course of action.

Examples of strategic investments can include investments in R&D activities, heavy expenditure on advertisement, initial investment in foreign markets to expand business in the future, or acquiring making rights. The purpose of such investments often involves defining the competitive position of the firm, hence being called strategic investments. These decisions are strategic choices made in long-term investment decisions.

Tactical Investment Decisions and Planning

Tactical planning is concerned with determining specific objectives and means by which strategic plans will be achieved. Tactical plans are considered intermediate plans, with a shorter time horizon compared to strategic plans. Some tactical plans, such as corporate policy statements, may exist for the long term and address repetitive situations.

Tactical investment decisions are generally taken at Top Management Level & Mid Management Level. Middle level management typically decides tactics. Tactical decisions are associated with statements of organisational plans, often short-term in nature, serving as the steps to implement the broader strategic vision.

Key Differences and Relationship

The sources highlight several parameters to distinguish between Strategic and Tactical Investment Decisions:

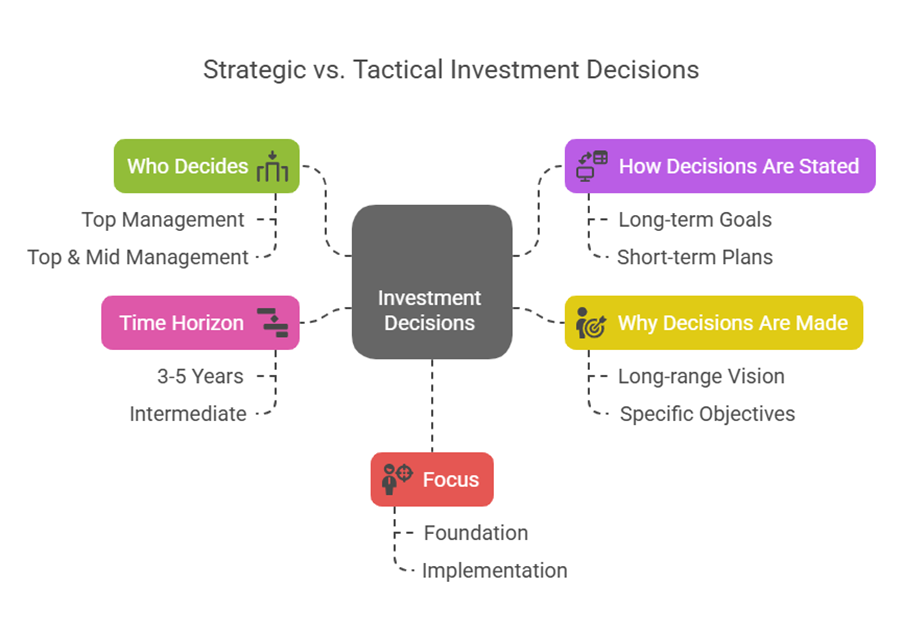

- Who decides: Strategic Investment Decisions are generally taken by Top Management, whereas Tactical Investment Decisions are generally taken by Top & Mid Management. Strategic planning is decided by Senior management, and tactical by middle level management.

- How decisions are stated: Strategic decisions are based on the Statement of organisation mission, goals and strategies (Long-term). Tactical decisions are based on the Statement of organisational plans (Short-term).

- Why decisions are made: The purpose of Strategic Investment Decisions (and planning) is to Establish a long-range vision of the organisation and provide a sense of unity and commitment to specified purpose. Tactical Planning is focused on determining the specific objectives and means required to achieve the strategic plans.

- Time Horizon: Strategic planning is long-term, involving durations typically of 3 to 5 years or longer, and long-range forecasts often exceeding 5 years. Tactical planning is intermediate, concerned with achieving strategic plans through specific objectives and means.

- Focus: Strategic planning is not concerned with day-to-day operations, serving as the foundation. Tactical planning focuses on the specific steps and means to implement the strategy.

In essence, strategic plans set the overarching, long-term direction and vision for the organisation, decided by top management. Tactical plans, decided by top and mid-management, define the specific, often shorter-term actions and objectives necessary to execute the strategic plans and achieve the long-range goals. Strategic planning provides the foundation upon which tactical planning is based.

Context: Long-Term Investment Decisions and Capital Budgeting

Both strategic and tactical investment decisions often fall under the umbrella of long-term investment decisions, commonly known as capital budgeting. Capital budgeting is the process of evaluating and selecting long-term investments that align with the goal of maximizing investor’s wealth.

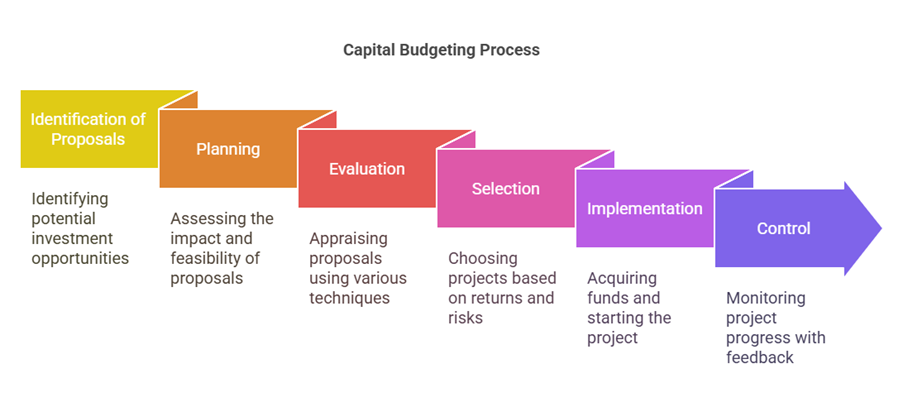

The process of capital budgeting involves several stages:

- Identification of various investment proposals. Proposals can originate from top management or lower ranks. The capital budgeting process begins with identifying potential investment opportunities.

- Planning: Assessing the potential effect of the opportunity on the firm’s fortunes and the management’s ability to exploit it. Promising opportunities advance as proposals.

- Evaluation: Determining a proposal’s investments, inflows, and outflows. This phase involves appraising the proposals using various investment appraisal techniques. This evaluation should consider marketing, technical, economic (social cost benefit), and ecological aspects, especially for long-term strategic projects. Key variables identified during strategic planning are relevant here.

- Selection: Choosing among projects based on returns, risks, and the cost of capital, aiming to maximize shareholders’ wealth. For mutually exclusive projects, a choice must be made where accepting one excludes others. This often involves ranking projects. In situations of limited funds (capital rationing), a combination of projects is selected to maximize total NPV.

- Implementation: Acquiring funds, purchasing assets, and starting the project.

- Control: Monitoring the project’s progress using feedback reports.

Investment decisions, particularly strategic ones, are crucial because they determine employment, economic activities, and growth at a national level. For a business entity, they aim to optimize fund utilization to maximize organisational wealth and shareholder wealth, generating revenue and ensuring long-term existence.

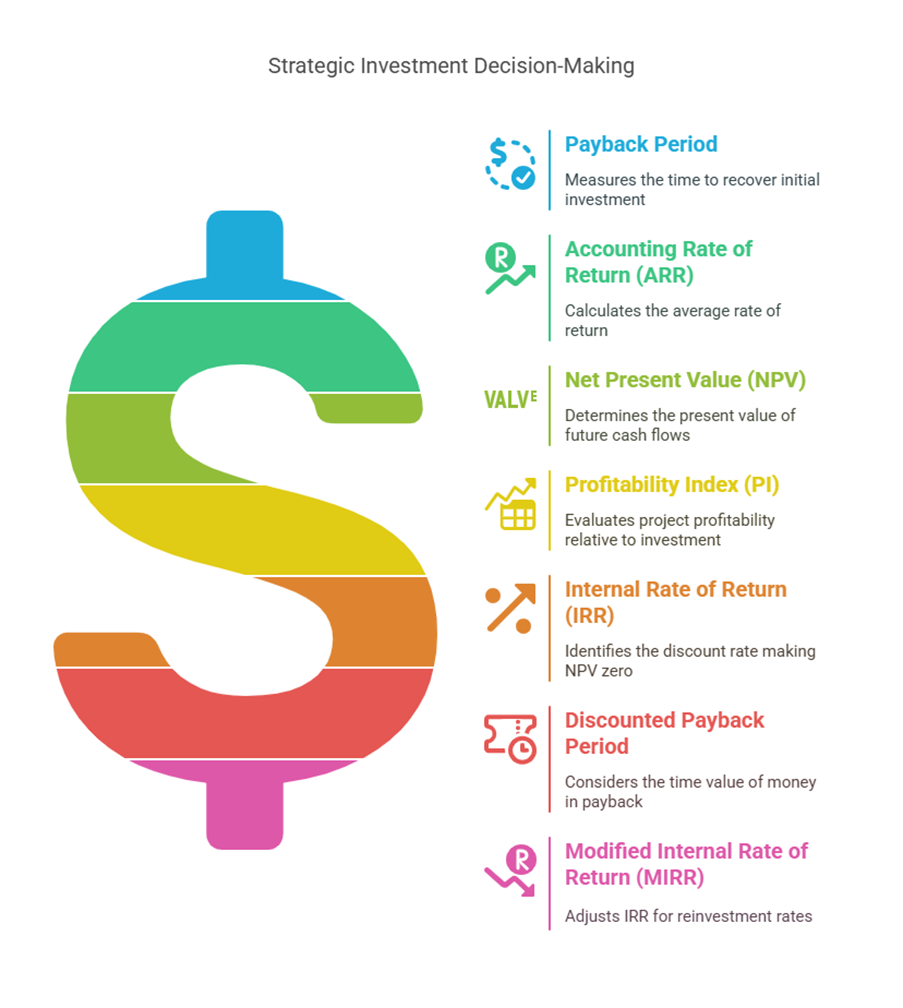

Various techniques are used to appraise investment proposals during the evaluation phase:

- Payback Period

- Accounting Rate of Return (ARR)

- Net Present Value (NPV)

- Profitability Index (PI) – Accepted if > 1, rejected if < 1. Projects ranked higher with higher PI.

- Internal Rate of Return (IRR)

- Discounted Payback Period

- Modified Internal Rate of Return (MIRR)

These techniques are used to evaluate cash flows associated with investment proposals. Estimating future cash flows is a crucial task, and the accuracy of cash flow estimates impacts the final decision. Relevant cash flows include incremental cash flows, opportunity costs, and tax shields (e.g., from depreciation). Sunk costs and committed costs are considered irrelevant.

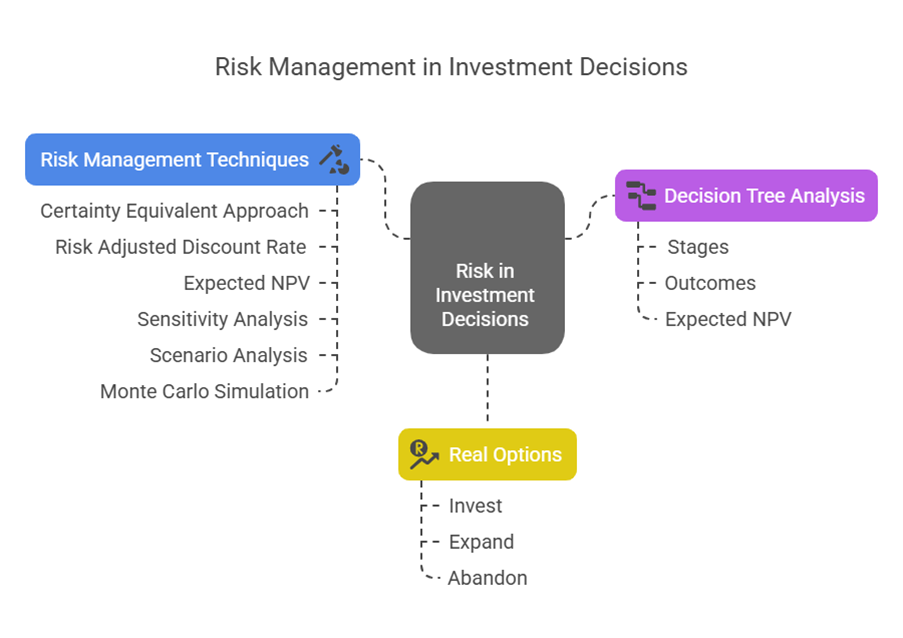

Risk in Investment Decisions

Investment projects, especially long-term strategic ones, are exposed to various degrees of risk. Risk arises from the uncertainty associated with future returns. Dealing with risk is an important aspect of investment decisions. Projects are evaluated based on their expected return and risk.

Techniques for dealing with risk in capital budgeting include:

- Certainty Equivalent Approach

- Risk Adjusted Discount Rate

- Expected NPV, Standard Deviation of NPV, and Use of Normal Distribution

- Sensitivity Analysis

- Scenario Analysis

- Monte Carlo Simulation

- Decision Tree Analysis

Decision tree analysis is a useful tool for analyzing investment opportunities involving a sequence of decisions over time, incorporating project flexibility and probabilities of outcomes. It involves defining stages, listing possible outcomes with probabilities and cash flow effects, and computing Expected NPV by working backward. Decision points (squares) represent management’s options, while chance nodes (circles) represent uncertain events with associated probabilities and monetary values.

Another aspect is ‘Options in Capital Budgeting’, also referred to as real options. These represent the flexibility to invest, expand, or abandon a project at a future date based on certain conditions. Examples mentioned as strategic investments like R&D or initial foreign market entry can be viewed as acquiring such real options.

Types of Investment Decisions and Strategic Relevance

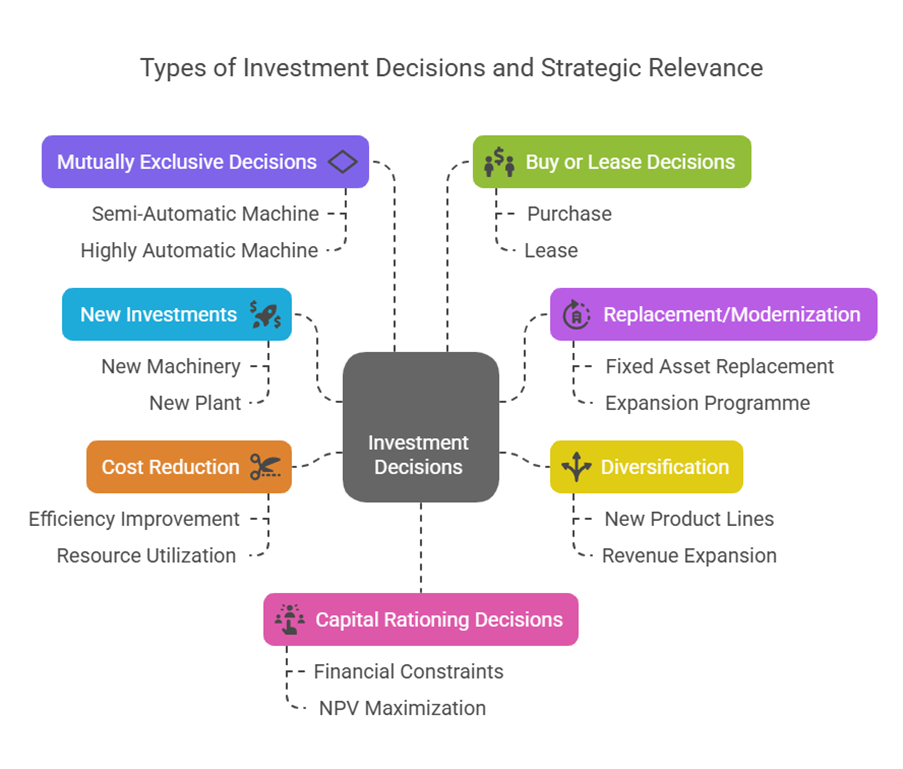

The sources list various types of capital investment decisions:

- New Investments: In a newly established or existing firm (e.g., purchasing new machinery, setting up a new plant).

- Investments for replacement or modernization or expansion programme. Expanding level of operation through increased capacity or a new plant can be a type of proposal. Replacing fixed assets is also a capital budgeting decision.

- Diversification: Deciding to diversify production into other lines, adding new lines. This typically requires large funds for long-term investment and is classified as a revenue expansion decision.

- Cost Reduction and Efficient Utilization of Resources: Proposals aimed at improving efficiency.

- Mutually Exclusive Decisions: Where accepting one proposal excludes others (e.g., choosing between a semi-automatic or highly automatic machine). Strategic choices might involve selecting between mutually exclusive large-scale projects.

- Buy or Lease Decisions: Deciding whether to purchase or lease an asset.

- Capital Rationing Decisions: Selecting projects under financial constraints, aiming to maximize total NPV from acceptable projects.

Many of these types, especially diversification, expansion, new product lines, or large-scale projects impacting the firm’s competitive position, are inherently strategic in nature.

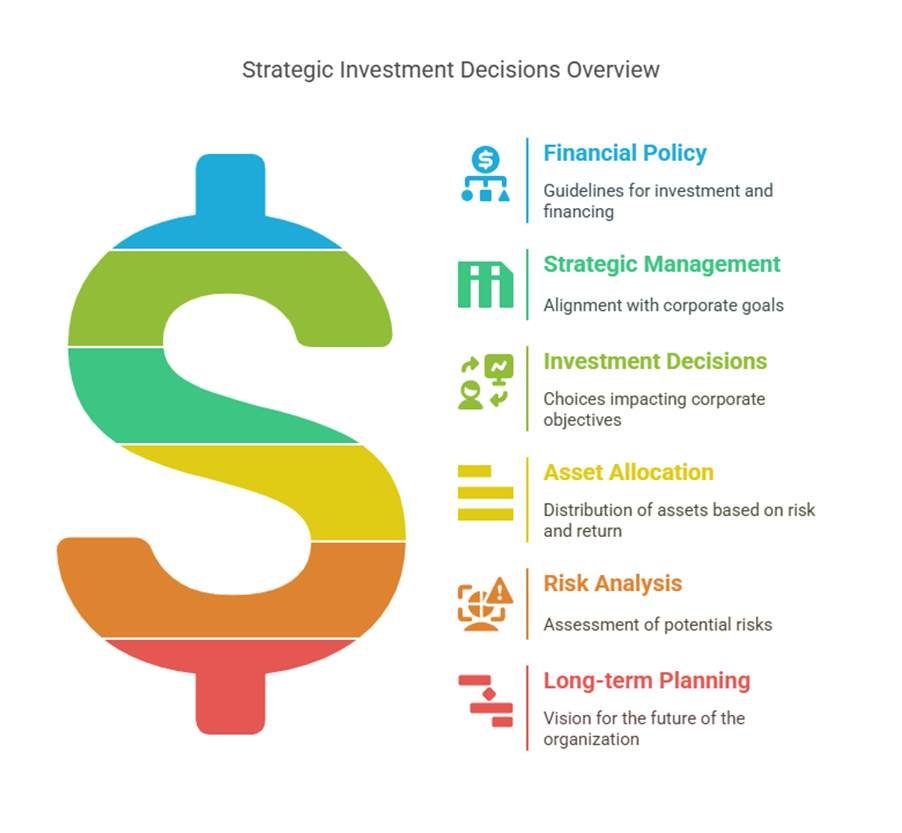

Interface of Financial Policy and Strategic Management

Strategic financial management is deeply integrated with the corporate strategic plan. It involves the optimal investment and financing decisions needed to achieve overall corporate objectives. Financial planners frame policies for regulating investments in fixed and current assets. They evaluate investment proposals, which may be grouped by type (new product, capacity increase, cost reduction), using capital budgeting exercises. Project evaluation and selection are key jobs under fund allocation, with the planner’s task being to make the best possible allocation under resource constraints.

Strategic investment decisions at the highest level might involve portfolio decisions, where investments are evaluated based on their contribution to the aggregate performance of the entire corporation rather than in isolation. Strategic asset allocation is described as a strategy under active portfolio management that involves determining long-term exposures to available asset classes based on risk, return, and co-variances, adjusted periodically to maintain target allocation within the investor’s objectives and constraints. This high-level decision aligns with the nature of strategic investment thinking.

In summary, Strategic Investment Decisions are long-term, high-level decisions taken by top management, setting the direction and vision for the future of the organisation. Tactical Investment Decisions are intermediate steps, taken by top and mid-management, defining specific plans and means to achieve those strategic goals. Both are crucial aspects of long-term investment planning (capital budgeting), involving rigorous evaluation, risk analysis, and alignment with overall corporate strategy to maximize wealth.