Introduction to Venture Capital Financing

Venture Capital (VC) financing is a new type of financial intermediary that emerged in India during the 1980s. It involves providing long-term financial assistance to projects established to introduce new products, inventions, ideas, and technology. Venture Capital finance is particularly suitable for risk-oriented businesses that require huge investment and are expected to yield results after a longer period, typically 5 to 7 years.

In a broad sense, Venture Capitalists (VCs) make investments to purchase equity or debt securities from inexperienced entrepreneurs who undertake highly risky ventures with the potential for future success. The term “Venture Capital” itself comprises “Venture,” a process with an uncertain outcome involving the risk of loss, and “Capital,” the resources needed to start an enterprise. The generic name “Venture Capital” was coined to denote the risk and adventure associated with such funds. Venture capital is defined as long-term funds in equity or semi-equity form to finance hi-tech projects involving high risk and yet having strong potential of high profitability. It is a form of equity financing specifically designed for funding high risk and high reward projects.

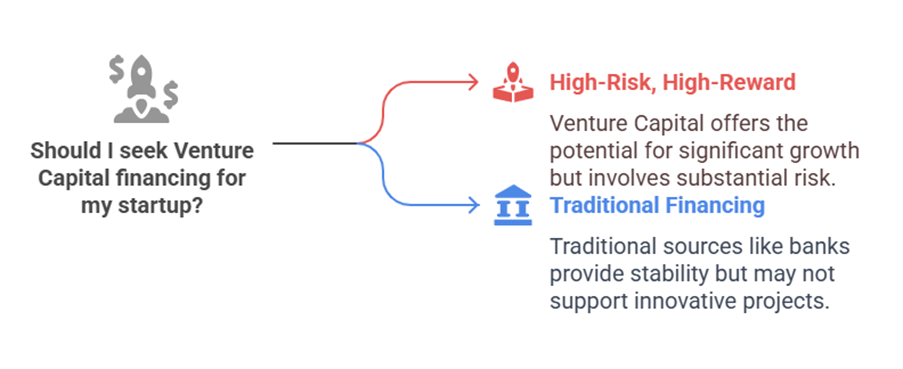

Venture Capital is an alternative investment fund (AIF). Venture capital funding differs from traditional sources of financing because VCs finance innovation and ideas that have the potential for high growth but come with inherent uncertainties. This makes it a high-risk, high-return investment. Traditionally, lenders like banks are not interested in startup businesses because they cannot rely on the security of assets or accurately forecast cash flows or repayment capacity.

Characteristics of Venture Capital Financing

Several key characteristics define Venture Capital financing:

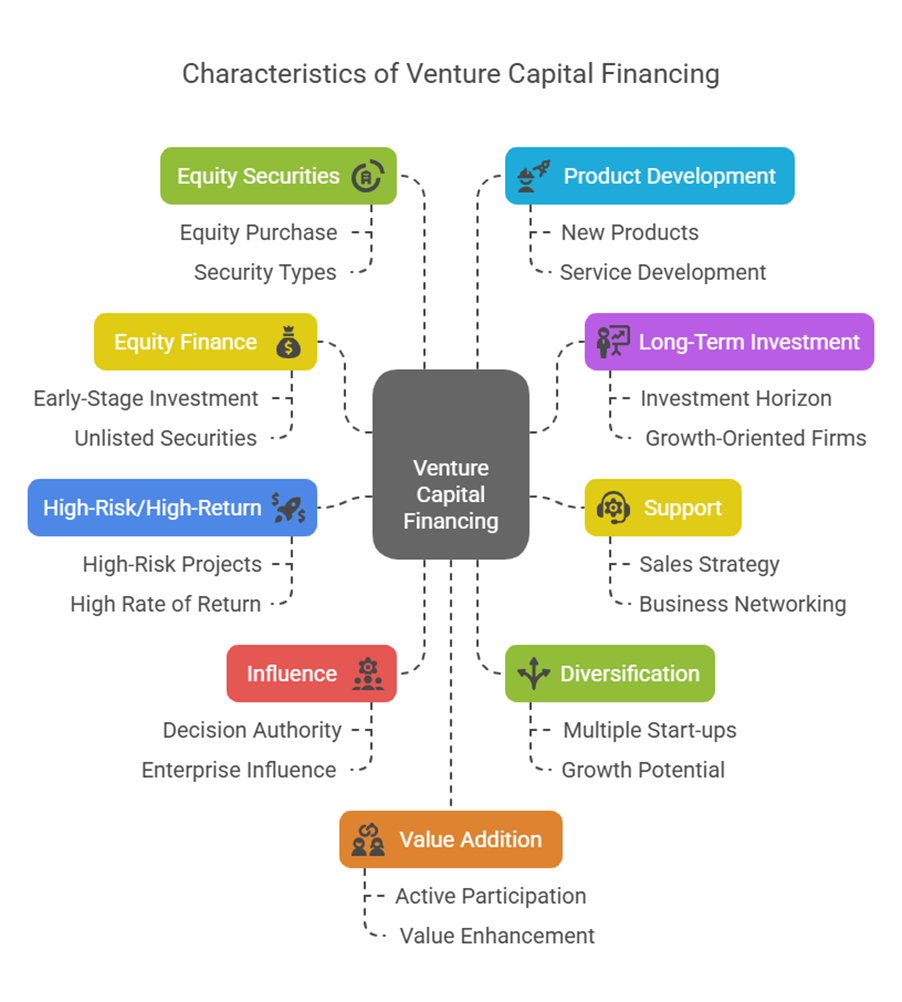

- It is primarily equity finance in new companies. The main focus is on early-stage investment, although it can also involve expansion-stage financing. VC funds invest primarily in unlisted securities of startups, emerging or early-stage venture capital undertakings.

- It can be viewed as a long-term investment in growth-oriented small/medium firms. The investment horizon is long, typically a minimum of 3 years and a maximum of 10 years.

- Besides providing funds, the investor also offers support in the form of sales strategy, business networking, and management expertise to help the entrepreneur grow. VCFs also bring knowledge and experts, help develop new products/services, and acquire the latest technologies to improve efficiency. They offer networking opportunities, with influential and wealthy investors promoting the company to achieve stellar growth.

- VC funds are given based on the company’s assets, size, and stage of product development. Since funded firms are usually start-ups or small, they are considered to have high-risk/high-return profiles. Venture capital investments are made in highly risky projects with the objective of earning a high rate of return. This high risk leads to Venture Capital firms potentially charging a 20% interest rate, which may increase to 25% per annum if the loan is not repaid on time.

- VCFs hold the authority to influence the decisions of the enterprises they invest in.

- To mitigate the risks of funding new projects, VCFs invest in a variety of young start-ups with the belief that at least one will achieve massive growth and provide a large pay-out.

- VCs purchase equity securities.

- They assist in the development of new products or services.

- They add value to the company through active participation.

- There is a lack of liquidity in the equity they receive, and they account for this by adding an illiquidity premium to the price and required return.

- The venture capitalist is a business partner, sharing both risks and rewards, and is rewarded with business success and capital gain.

- VCs are experienced in preparing companies for an Initial Public Offering (IPO) or facilitating a trade sale.

Working of Venture Capital Funds

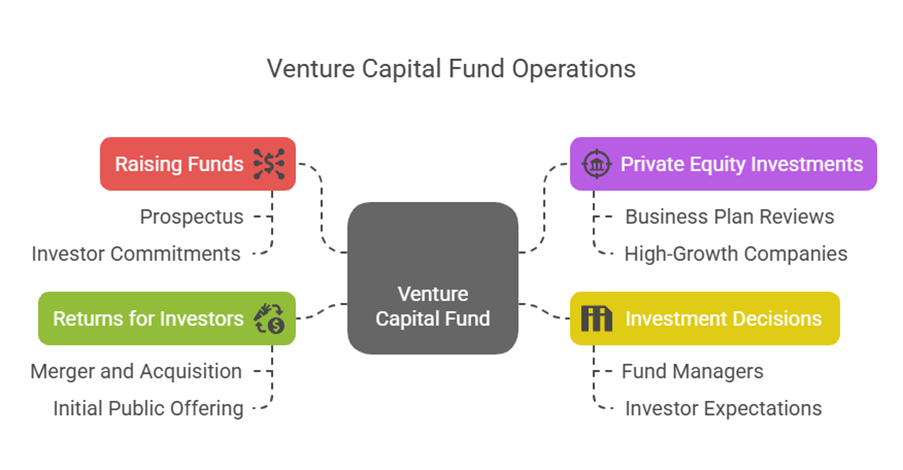

Like all funds, venture capital funds must first raise money before making investments. Potential investors receive a prospectus and commit money. The fund’s operators then call investors to finalize individual investment amounts. After raising funds, the venture capital fund seeks out private equity investments that can generate positive returns for its investors. This involves the fund manager(s) reviewing numerous business plans to find potentially high-growth companies. Investment decisions are made by the fund managers based on the prospectus and investor expectations. An annual management fee of around 2% is charged once an investment is made. Investors make returns when a portfolio company exits, either through a merger and acquisition or an IPO. The fund also keeps a percentage of the profits if the investment is profitable.

Modes/Methods of Venture Financing

Venture Capital finance can be provided through several methods:

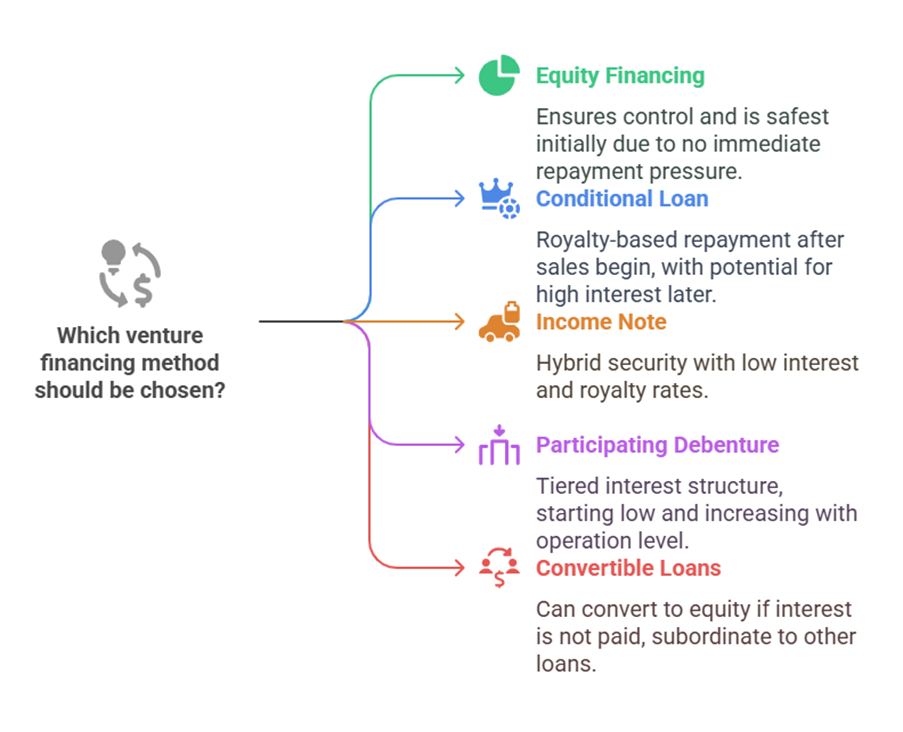

- Equity financing: This is the most common method. Venture capital finance is generally provided as equity share capital because undertakings often need funds for a longer period but may not generate returns in the initial stages. Venture capital firms’ equity contribution typically does not exceed 49% of the total equity capital, ensuring that effective control and ownership remain with the entrepreneur. Equity financing is considered the safest mode in the initial years due to uncertainty about cash inflows, unlike debt which requires periodical servicing.

- Conditional loan: This type of loan is repayable in the form of a royalty after the venture begins generating sales. No interest is paid initially. In India, VCs charge royalty ranging between 2% and 15%, with the rate depending on factors like gestation period, cash flow patterns, and risk. Some VCs offer the option of paying a high interest rate (potentially above 20%) instead of a royalty once the enterprise becomes commercially sound. A conditional loan usually involves either no interest or a nominal coupon payment, with a royalty on sales turnover. As sales pick up, the interest rate increases, and royalty amounts decrease. From a VC perspective, conditional loans are a potentially less preferable option than secured debt, as equity is an unsecured instrument.

- Income note: This is a hybrid security combining features of conventional and conditional loans. The entrepreneur pays both interest and royalty on sales, but at substantially low rates.

- Participating debenture: This security involves a tiered charge structure. In the start-up phase, no interest is charged. A low interest rate is charged up to a certain level of operation, after which a high interest rate is required.

- Convertible Loans: These loans are subordinate to other loans and may be converted into equity if interest payments are not made within the agreed time limit. Other financing methods mentioned include Partially Convertible Debentures, Cumulative Convertible Preference Shares, Deferred Shares, Convertible Loan Stock, Special Ordinary Shares, and Preferred Ordinary Shares.

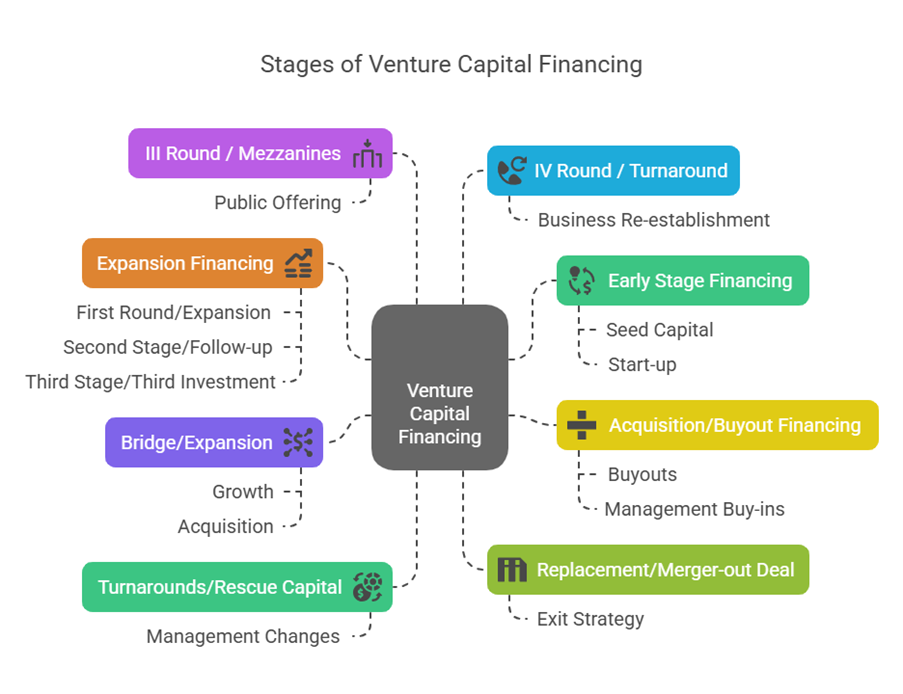

Stages of Venture Capital Financing

Venture Capital Funds are often classified based on their utilization at different stages of a business. The main types are:

- Early stage financing: This stage includes seed capital and start-up funding.

- Seed Capital: Low-level financing needed to prove a new idea, often for conceptualization/planning or research base. The Seed Capital Assistance scheme in India is designed for professionally or technically qualified entrepreneurs lacking financial resources. This assistance is interest-free but carries a service charge. IDBI provides Seed Capital assistance.

- Start-up: Funding for early-stage firms needing money for expenses related to marketing and product development, or commencement of business activity.

- Expansion financing: Funding for businesses expanding their productive assets or through acquisition. This can be Medium risk.

- First Round/Expansion: Financing for expansion in production/marketing or to meet demand.

- Second Stage/Follow-up: Financing for marginal progress.

- Third Stage/Third Investment: Financing for development/expansion.

- Acquisition/Buyout financing: Financing required when a management group wishes to acquire another company’s product or buy an ongoing venture.

- Buyouts: Includes Management Buyouts (funds for existing management/investors to acquire a product) and Management Buy-ins (funds for an outside group to buy an ongoing venture).

- Bridge/Expansion: Can refer to expanding business by growth or acquisition, or company planning to go public.

- Turnarounds/Rescue capital: Financing for distressed companies, which is risky and may lead to demands for management changes.

- Replacement/Merger-out deal: Refers to a planned exit.

- III round / Mezzanines: Last stage before a public offering.

- IV round / Turnaround: Re-establishment of business.

Angel Investors typically provide seed money. Formal debt from banks/NBFCs may be available once a startup shows market traction and revenue to finance interest payments. Venture Debt Funds invest in startups primarily in the form of debt, often alongside angel or VC rounds. For the scaling stage, VCs with larger ticket sizes and Private Equity/Investment firms may provide funding.

Venture Capital Institutions/Funds

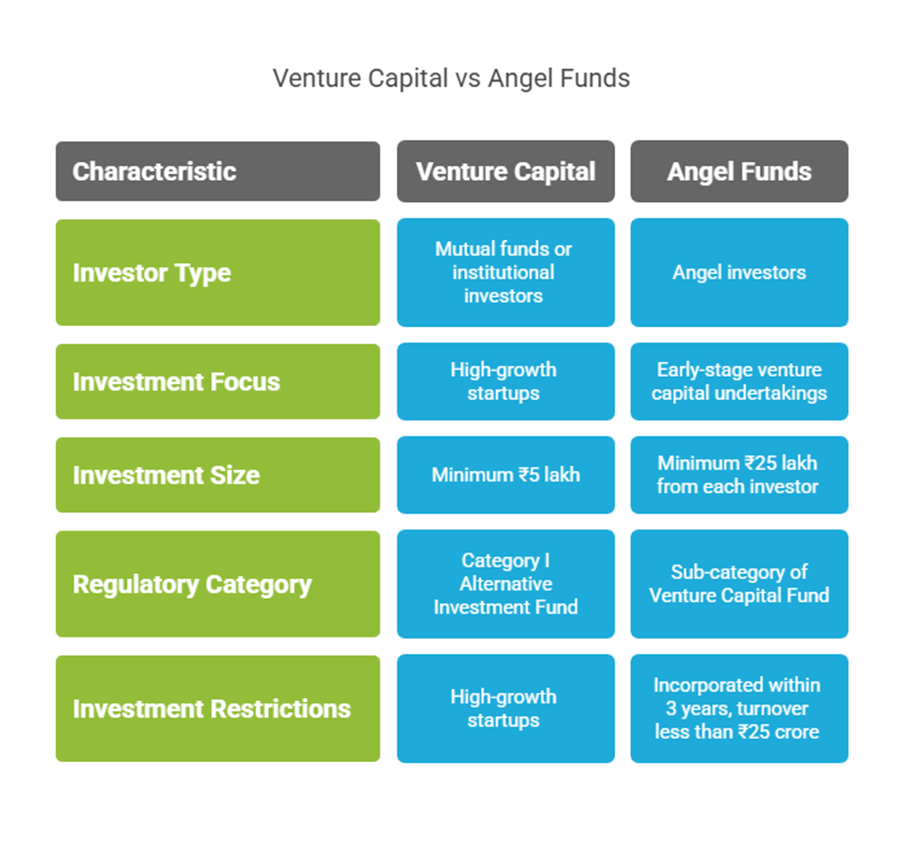

Venture Capital Institutions, or Funds, are a type of financial intermediary. The term Venture Capital fund is usually used to denote Mutual funds or Institutional investors. They provide equity finance or risk capital to little known, unregistered, highly risky, young and small private businesses, especially in technology-oriented and knowledge-intensive fields. VCs are professionally managed investment funds that invest exclusively in high growth startups. Each VC fund has an investment thesis regarding preferred sectors, stage of the startup, and funding amount. They take startup equity in return for investment and actively engage in mentoring investee startups.

Angel funds are a sub-category of Venture Capital Fund under Category I Alternative Investment Fund. Angel funds raise funds from angel investors and invest according to AIF Regulations. An angel fund accepts at least ₹25 lakh from an angel investor for a maximum of 3 years. An angel investor is an individual with net tangible assets of at least ₹2 crore (excluding principal residence value) and has early-stage investment experience, is a serial entrepreneur, or a senior management professional with at least ten years of experience. Angel funds raise funds through private placement. Angel funds invest only in venture capital undertakings that have been incorporated within the preceding three years, have a turnover less than ₹25 crore, and are not promoted by a large industrial group. They cannot invest more than 25% of their investable funds in one venture capital undertaking.

Minimum investment in a Venture Capital Fund from any investor (Indian, Foreign, NRI) is generally not less than ₹5 lakh if the fund is set up as a company or trust.

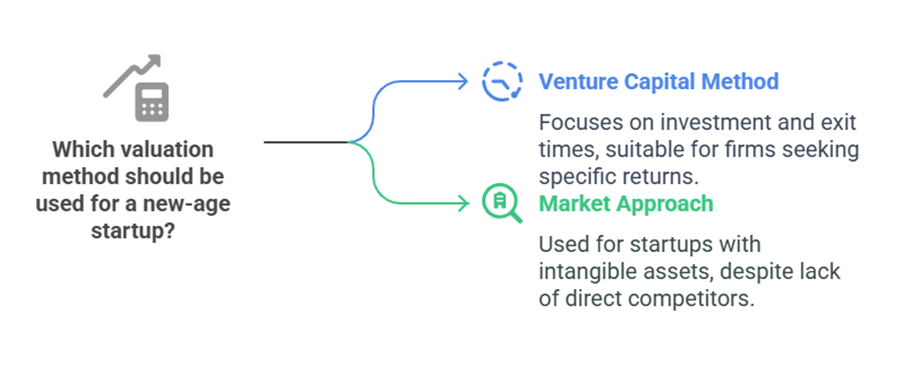

Valuation Methods

The sources mention that Venture Capital methods exist for valuing venture capital undertakings. These methods typically focus on the starting time of investment and the exit time. The Venture Capital Method is used by venture capital firms, who seek a return equal to a multiple of their initial investment or a specific internal rate of return based on the perceived risk. This method incorporates the relevant timeframe for discounting a future value attributable to the firm. The post-money value is calculated by discounting at the investor’s expected or required rate of return. Valuing new-age startups, especially those with significant intellectual property and intangible assets, presents challenges. Market approaches are sometimes used for valuing new-age startups, particularly in advanced funding rounds, despite the lack of directly comparable established competitors.

Regulation

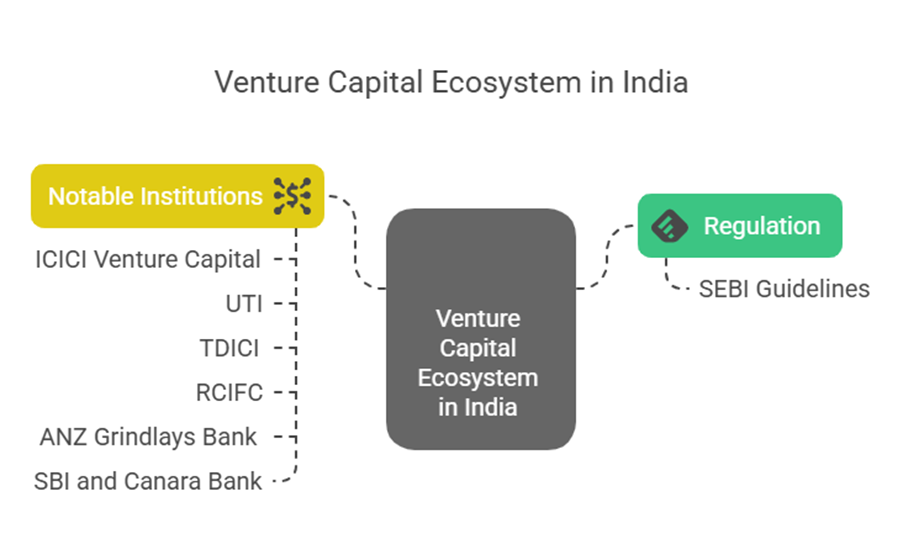

Venture Capital funds in India are regulated by the guidelines issued by the Securities and Exchange Board of India (SEBI).

Notable Venture Capital Institutions in India

The sources list several notable Venture Capital Financing institutions in India:

- ICICI Venture Capital: The first VC Financing in India, started in 1988 as a joint venture of ICICI and UTI.

- UTI: Launched the Venture Capital Unit Scheme (VECAUS-I) to raise finance in 1990.

- Technology Development and Information Company (TDICI): Another major VC financing institution in India.

- Risk Capital and Technology Finance Corporation Ltd. (RCIFC): Provides VC finance to technology-based industries.

- ANZ Grindlays Bank: Set up India’s first private sector Venture Capital fund.

- SBI and Canara Bank: Also involved in Venture Capital Finance, providing either equity capital or conditional loans.

Evolution of Venture Capital in India

Venture Capital began in India in the 1970s when a government committee addressed inadequate funding for entrepreneurs and start-ups. However, the first all-India VC funding started a decade later by IDBI, ICICI, and IFCI. Institutionalization in 1988 led to government guidelines that were initially restrictive, focusing narrowly on innovative technologies by first-generation entrepreneurs, making investment highly risky and unattractive.

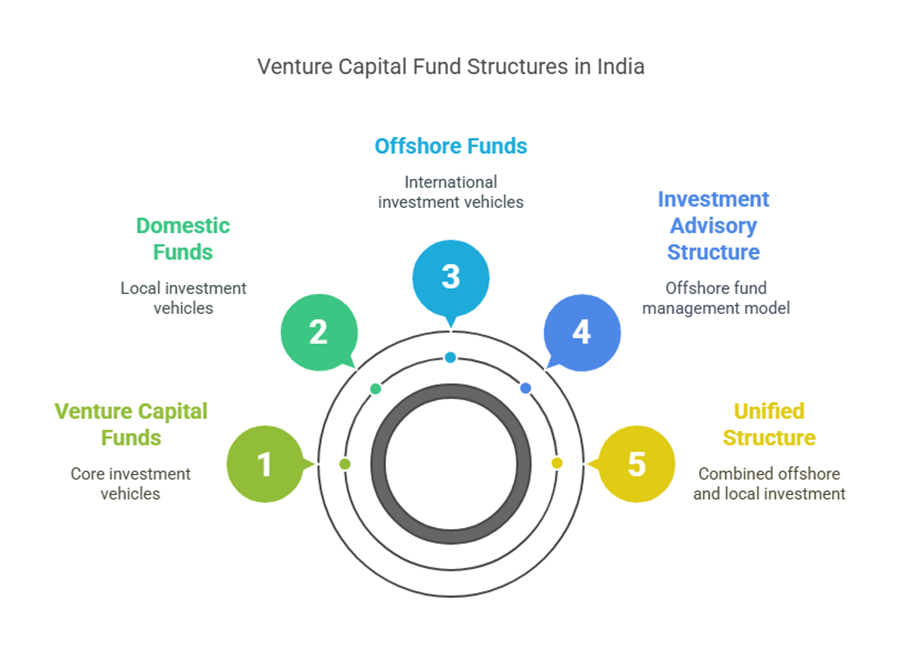

Structure of Venture Capital Funds in India

Three main fund structures exist: one for domestic funds and two for offshore ones.

- Domestic Funds: Usually structured as a domestic vehicle (trust or company, with trust prevailing for flexibility) for pooling funds and a separate investment adviser. India does not recognize a limited partnership.

- Offshore Funds: Can have a unified structure or an investment advisory structure. In the investment advisory structure, the fund is established offshore and managed by an offshore manager, with an Indian investment adviser carrying out due diligence and identifying deals. In a unified structure, overseas investors pool assets in an offshore vehicle that invests in a locally managed trust, while domestic investors contribute directly to the trust, which then makes local portfolio investments.

Venture Capital within the Financial System

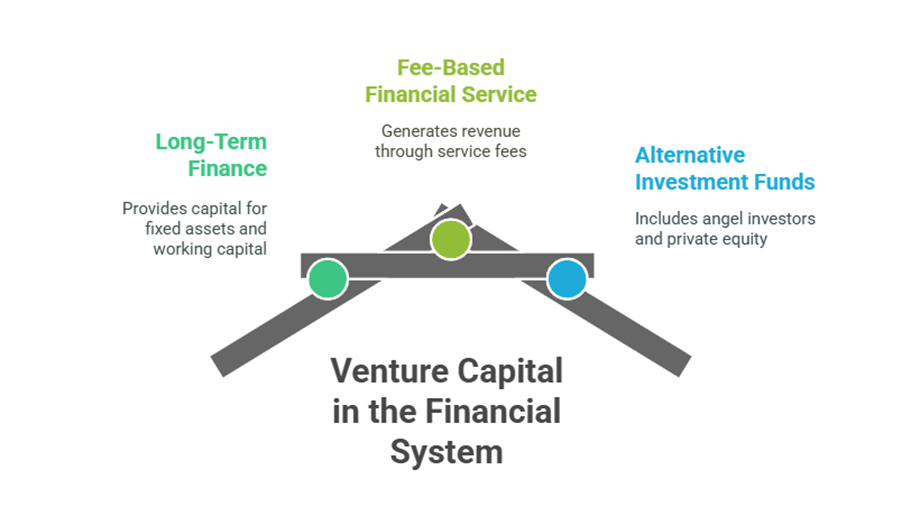

Venture Capital financing is considered an important long-term source of finance. Long-term sources are needed for capital expenditures in fixed assets and permanent working capital. It is also listed as one of the fee-based financial services.

Venture Capital funds are also included in discussions of Alternative Investment Funds (AIFs) alongside Angel Investors and Private Equity.

In summary, Venture Capital Institutions are crucial players in financing high-risk, high-growth ventures, providing not just capital but also expertise and networking to support entrepreneurial success. They are regulated in India and operate through various structures and financing methods tailored to the specific needs and stages of the businesses they invest in.