Working Capital is a crucial concept in financial management, representing the capital needed to meet the day-to-day transactions of a business concern. It is also described as the funds available for day-to-day operations of an enterprise. Unlike Fixed Capital, which is invested in long-term assets [previous conversation], working capital is required for short-term financial needs.

Working capital can be understood through different concepts, based on value and time.

Concepts of Working Capital

- On the basis of Value:

- Gross Working Capital: This refers to the firm’s aggregate of current assets or the total of all current assets of business. It is the firm’s investment in current assets. According to this concept, Gross working capital equals Total current assets. Gross working capital is considered more helpful in managing each individual current asset for day-to-day operations.

- Net Working Capital: This is defined as the excess of current assets over current liabilities. It represents the difference between current assets and current liabilities. Net Working Capital can also be defined as the part of the current assets which are financed with the long-term funds. If current assets exceed current liabilities, it is positive working capital. If current liabilities are in excess of current assets, it is negative working capital. Net working capital is considered more useful in the long run and when understanding the sources of funds.

- On the basis of Time:

- Permanent/Fixed Working Capital: There is always a minimum level of current assets which is continuously required by the enterprise to carry out normal business operation. This minimum level, such as required minimum stock or cash balance, is called permanent or fixed working capital because this amount is permanently blocked in current assets. This Rigid, fixed, regular or permanent working capital is indispensable for any business concern.

- Temporary/Variable Working Capital: This refers to working capital needs that fluctuate, varying seasonally or depending on other business fluctuations. This is also called seasonal, temporary or flexible working capital.

The permanent working capital should be financed from long-term sources, while temporary working capital should be financed from short term sources.

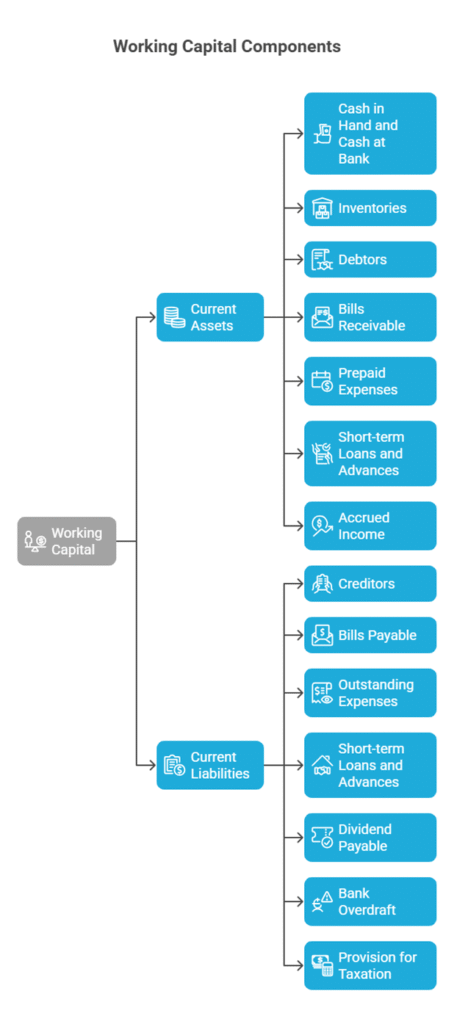

Components of Working Capital

Working capital consists of various current assets and current liabilities.

- Current Assets are assets expected to be realised, sold, or consumed within the normal operating cycle or within twelve months, whichever is longer. They are held primarily for trading in the ordinary course of business and can be converted into cash within an accounting period, generally a year. Common current assets mentioned include:

- Cash in Hand and Cash at Bank.

- Inventories (Stock): Raw materials, Work-in-process, and Finished goods.

- Debtors (Sundry Debtors).

- Bills Receivable.

- Prepaid Expenses.

- Short-term Loans and Advances.

- Accrued Income.

- Current Liabilities are obligations expected to be settled within the entity’s normal operating cycle or within twelve months. They are held primarily for trading. Common current liabilities mentioned include:

- Creditors (Sundry Creditors or Trade Payables).

- Bills Payable.

- Outstanding Expenses (Payables for overheads, Wages Payables, Liabilities for expenses).

- Short-term Loans and Advances.

- Dividend Payable.

- Bank Overdraft.

- Provision for Taxation.

Need and Significance of Working Capital

Working capital is needed for purposes such as purchasing raw materials, paying wages to workers, paying day-to-day expenses, and maintenance expenditure. Its primary objective is to ensure an organization maintains sufficient cash flows to meet its day-to-day operating expenses and its short-term obligations. Working capital is essential for the uninterrupted and smooth functioning of the day-to-day business.

Having adequate working capital is crucial. Both excessive as well as inadequate working capital positions are dangerous. A large amount of working capital means the company has idle funds, which are expensive due to their cost. Conversely, inadequate working capital puts the firm at risk of insolvency.

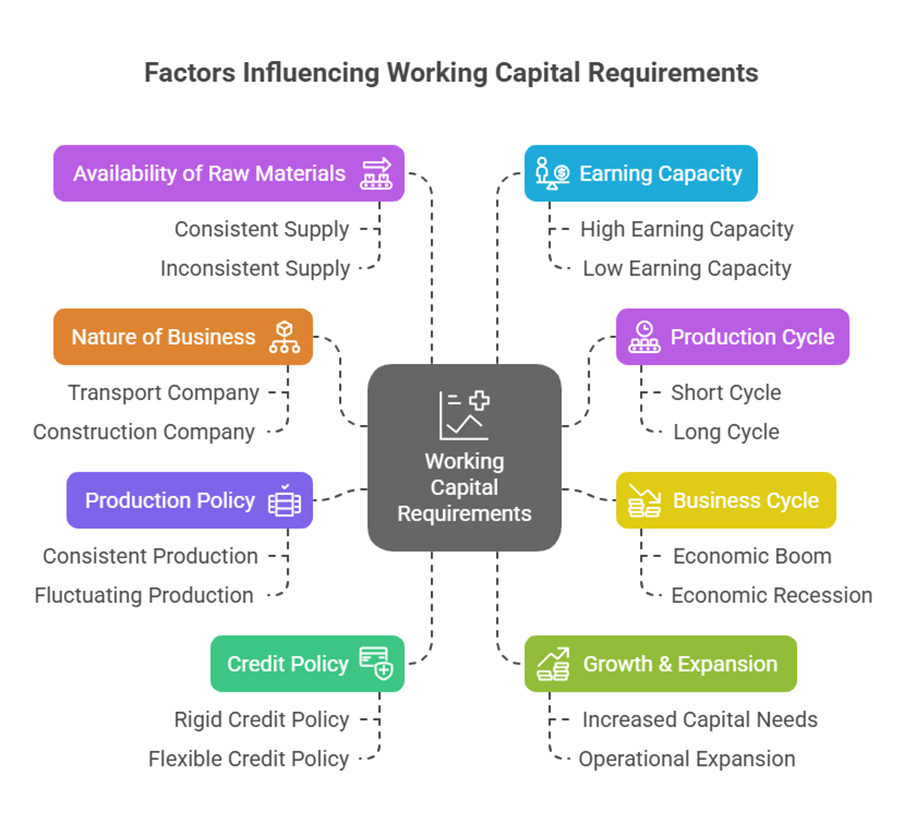

Determinants of Working Capital

Working capital requirements are influenced by several factors, including:

- Nature of business: Different types of businesses have different needs; for example, a transport company needs less working capital than a construction company.

- Production cycle: The length of time it takes to convert raw materials into finished goods.

- Business cycle: Economic fluctuations can affect sales and inventory needs.

- Production policy: Whether production is consistent or fluctuates.

- Credit policy: The terms offered to debtors and received from creditors. A rigid credit policy (cash sales) requires less working capital.

- Growth & expansion: Expanding businesses typically need more working capital.

- Availability of raw materials: Consistent supply reduces the need for large raw material stocks.

- Earning capacity: Higher earning capacity can generate more working capital from operations.

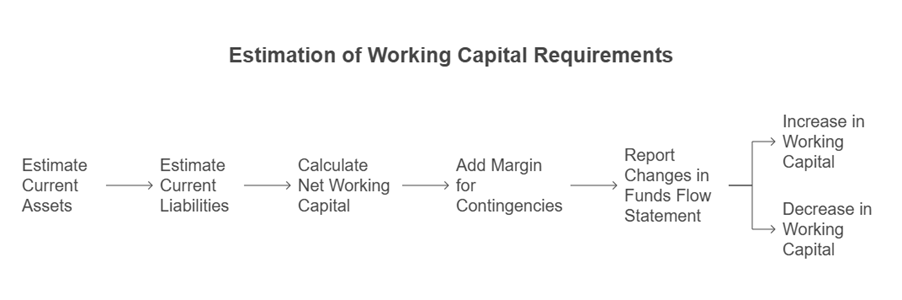

Estimation of Working Capital Requirements

Estimating working capital needs is a key part of financial planning. The process involves forecasting the amount required for each item of current assets and current liabilities. The finance manager first estimates the required current assets and then the required working capital for a particular period.

The sources provide numerous examples of calculating working capital requirements based on different components like stocks (raw materials, work-in-process, finished goods), debtors, creditors, cash, and prepaid/outstanding expenses, often expressed in terms of months, weeks, or days of consumption, sales, or credit period. The calculation often follows a format of Total Current Assets minus Total Current Liabilities to arrive at Net Working Capital, sometimes with an added margin for contingencies. Some estimations are done on a cash cost basis.

Changes in working capital are also calculated and reported in funds flow statements. An increase in working capital is considered an application of funds, while a decrease is a source.

Financing Working Capital

Working capital needs are met through various sources, primarily banks in India. While permanent working capital is ideally financed by long-term sources, temporary working capital can be financed by short-term sources. Long-term sources primarily support fixed assets but secondarily provide the margin money for working capital. Short-term sources of finance more or less exclusively support the current assets.

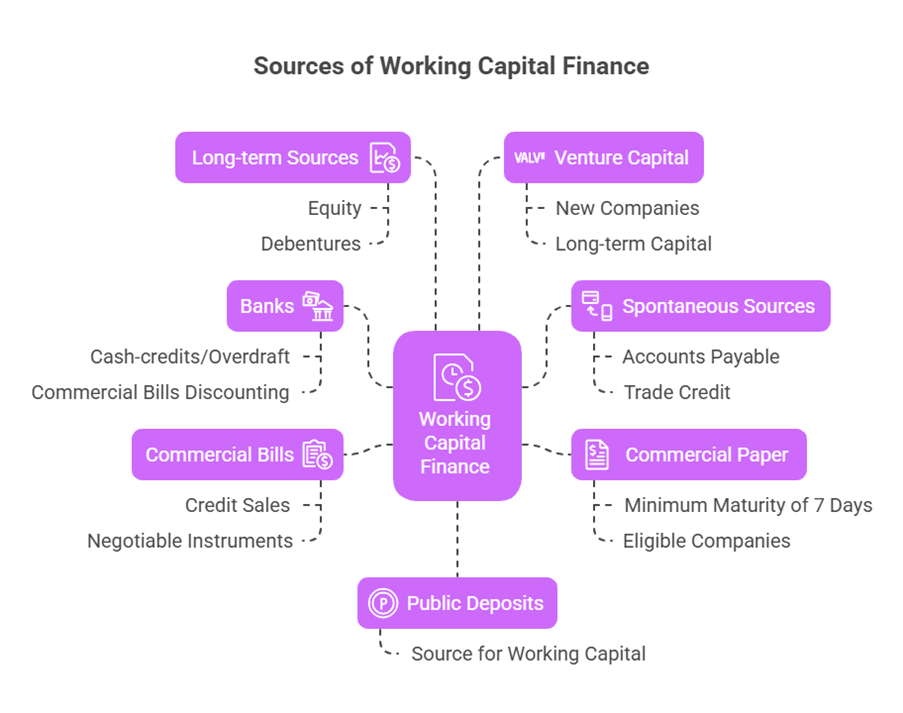

Sources of working capital finance mentioned include:

- Banks: Major suppliers of working capital credit. Banks assess requirements using various methods, moving away from the Maximum Permissible Bank Finance (MPBF) concept. Bank credit can be provided through cash-credits/overdraft and purchase/discounting of commercial bills.

- Spontaneous Sources: These arise automatically from business operations, such as accounts payable (trade credit). Trade credit is credit given by one firm to another, recorded as accounts payable by the buyer.

- Commercial Paper: An unsecured promissory note with a minimum maturity of 7 days, issued by eligible companies.

- Commercial Bills: Short-term, negotiable instruments arising from credit sales.

- Long-term Sources: While mainly for fixed assets, sources like equity, preference shares, debentures, and long-term loans also provide the margin for working capital [106, 123, previous conversation]. Term lending financial institutions also have working capital financing schemes.

- Venture Capital: Mentioned as a form of equity financing for new companies, providing long-term capital, but confusingly linked to financing temporary working capital like plant/building in one source [previous conversation].

- Public Deposits: Listed as a source for working capital [previous conversation].

Management of Working Capital

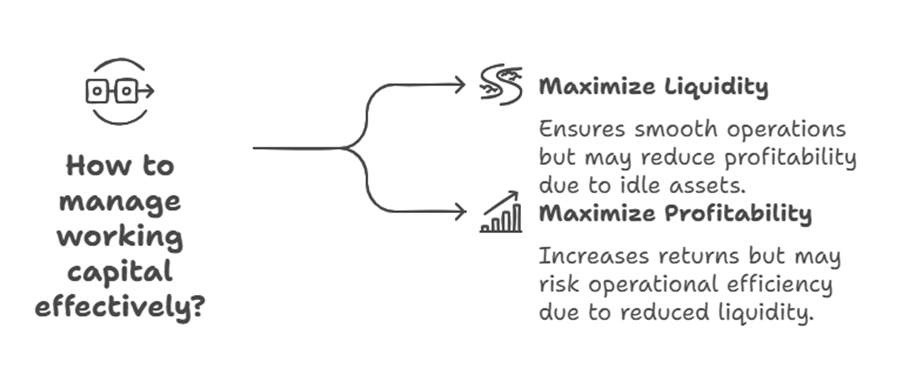

Working Capital Management is a process designed to ensure an organization operates efficiently by monitoring and utilizing its current assets and current liabilities to the best effect. It involves managing the balance between a firm’s short-term assets and liabilities. The scope includes maintaining adequate working capital (managing levels of current assets and liabilities) and financing it properly.

A key aspect of working capital management is the trade-off required between liquidity and profitability. While maintaining liquidity is important for smooth functioning, tying up funds unnecessarily in idle assets reduces liquidity and opportunity to earn better returns. The goal is to increase profitability without disturbing day-to-day functions.

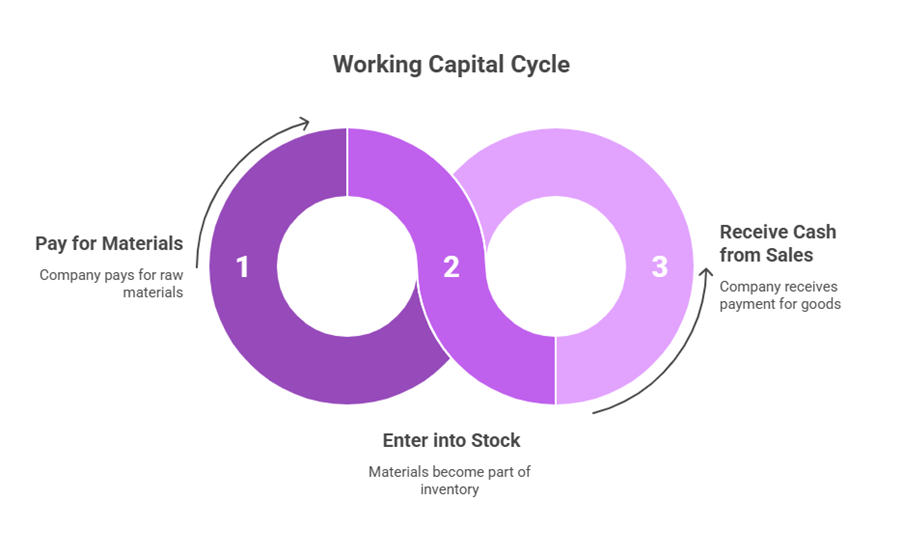

Working Capital Cycle

Also called the Operating Cycle or Business Cycle, the Working Capital Cycle indicates the length of time between a company’s paying for materials, entering into stock and receiving the cash from sales of finished goods. It is determined by adding the number of days required for each stage in the cycle.

In essence, Working Capital is the lifeblood for a business’s daily operations, requiring careful planning, estimation, financing, and management to ensure liquidity and support profitability.